Interviews

Three Years of CSRD Reporting: Lessons from an Early Mover, Ørsted

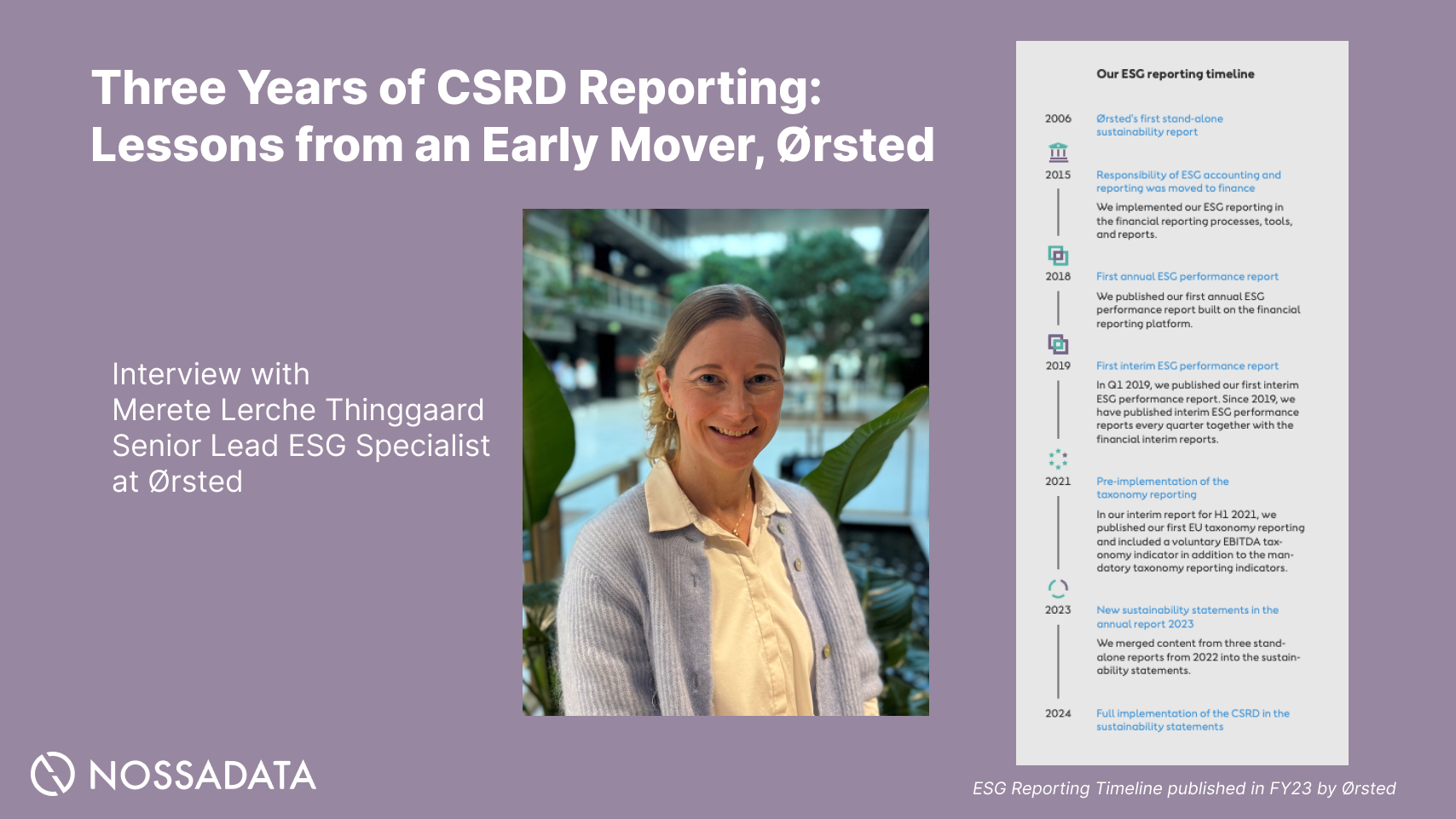

An expert interview with Merete Lerche Thinggaard, Senior Lead ESG Specialist at Ørsted, on three CSRD reporting cycles.

.png)

2025 was a turning point for environmental social and governance reporting among listed corporates. It was a year of regulatory recalibration. The world shifted firmly towards the International Sustainability Standards Board (ISSB) framework as the emerging baseline for investor-focused disclosures. At the same time, ESG ratings, benchmarks and data quality came under the microscope for sheer volume.

This shift in the ESG landscape meant practical implementation, governance enhancements and alignment across frameworks. Companies with ESG strategies and structured data models emerged as early leaders as the disclosure calendars from platforms like CDP, CSA and EcoVadis tightened up.

Below we provide a rundown of the key ESG frameworks and developments that shaped 2025, what they meant in practice for corporate sustainability and what ESG teams should keep an eye on for 2026.

2025 was the year ESG moved from theory to tracked, enforceable practice. Despite political headwinds in some jurisdictions and quarterly outflows from sustainable funds, the structural shift towards integrated sustainability disclosures continued.

Here are some of the numbers that mattered:

Several jurisdictions announced or advanced ISSB-aligned rules in 2025. Hong Kong began phasing in IFRS S2-aligned climate disclosures from 1 January 2025. The UK consulted on UK Sustainability Disclosure Standards (UK SRS). Türkiye took its first steps towards regulated reporting with TSRS standards. And the UAE’s Federal Climate Law entered into force in May 2025, as the global momentum behind climate commitments gathered pace.

Despite political flux—including US executive orders promoting fossil fuels and rolling back Inflation Reduction Act incentives—asset owner sustainability uptake (73%) and California’s persistence on climate laws showed that ESG considerations are here to stay in stakeholder expectations and financial markets.

2025 was the year ESG regulation went from expansion to consolidation. Policymakers across the EU, UK, US and Middle East adjusted timelines and datapoints but kept the core ESG objectives and enforcement intact. The message was clear: simplify but not retreat.

Below we break down the major regulatory developments by jurisdiction.

The CliffsNotes version: 2025 was the first real CSRD reporting year for Wave 1 entities (large public interest entities), while the Omnibus proposals reset the timelines for others. Quality of governance and ESG data—not quantity—was what mattered most.

2025: The Highlights

The EU’s “Omnibus simplification package” was first adopted by the EU Council on 14 April 2025, following European Parliament approval on 3 April. This package proposed:

The final vote on passing the EU Omnibus took place and passed in the EU Parliament on December 16th 2025.

Early 2025 CSRD reports from large EU-listed companies showed practical approaches to double materiality assessments. Impact-Risk-Opportunity (IRO) counts typically ranged from the low 20s to low 50s. These reports showed increased transparency on carbon emissions, energy efficiency, water, waste management, biodiversity, diversity, labour practices and community metrics. Science based targets and net zero commitments were common, although application of double materiality varied.

What to watch:

2025 was the first year ISSB moved from conceptual frameworks to phased-in mandatory or quasi-mandatory use in capital markets. ISSB is now the standard around which all other reporting frameworks are building.

2025 Milestones:

Early adopters in 2025 set the bar high for consistent, investor-grade climate metrics. Many regulators signalled future assurance requirements for ISSB-aligned reporting that would match financial reporting rigor.

What to Watch in 2026:

US climate disclosure rules adopted by the SEC in 2024 faced legal challenges throughout 2025 and created uncertainty for multinational issuers. But California’s climate laws moved forward despite court actions.

California remained the US standard-setter despite legal challenges. Scope 3 greenhouse gas emissions and climate risk disclosures were top of the agenda.

The California Air Resources Board (CARB) advanced draft regulations in 2025 on:

A court injunction delayed SB 261 implementation but preparatory enforcement notices and guidance still encouraged large businesses operating in California to prepare for climate risk reporting. Proposed rulemaking was delayed to Q1 2026 board meeting but SB 253’s 2026 reporting on prior-year GHG emissions remained unchanged.

Financial implications for multinationals: Companies with over USD 1 billion revenue operating in California must now model how these state rules intersect with SEC, ISSB and ESRS frameworks—especially around Scope 3 data and global supply chains.

California’s rules support the state’s 2045 carbon neutrality goal and 100% clean electricity targets which exceed federal baselines.

What to Watch:

The UK and selected Middle East jurisdictions used 2025 to refine stewardship, supply-chain and climate rules that impact global ESG strategies.

UK Modern Slavery Act Updates:

2025 saw a major overhaul of the UK “Transparency in Supply Chains” guidance under the modern slavery act. Key changes included:

UK Stewardship Code:

The updated UK Stewardship Code in 2025 reinforced long-term sustainable value creation but shifted focus towards narrative, outcomes-focused reporting instead of checklist-style ESG disclosures.

UAE Federal Climate Law:

The UAE’s Federal Climate Law entered into force on 30 May 2025, mandating:

These developments underscore how listed corporates must enhance supply chain due diligence, human rights oversight, and climate governance across global operations to remain competitive and protect consumers.

Contact Nossa Data for support with managing ESG Regulatory compliance & preparations

Beyond hard law, 2025 was shaped by updates to mainstream voluntary (and semi-mandatory) frameworks underpinning climate, nature, and impact reporting. While some frameworks like TCFD and SASB are being folded into ISSB, they still influence regulatory design and stakeholder expectations.

TCFD principles remained foundational in 2025, even as ISSB began to subsume its recommendations into IFRS S2.

2025 Highlights:

The UK Financial Conduct Authority (FCA) published its 2025 climate disclosure review findings. The review critiqued inconsistencies in listed issuers’ and asset managers’ TCFD-aligned disclosures, particularly around:

Regulators in multiple jurisdictions used 2025 to move from “comply or explain” to more prescriptive expectations for climate metrics, governance factors, and risk management.

What to Watch:

2025 saw rapid uptake of the Taskforce on Nature-related Financial Disclosures (TNFD) by investors and early-adopter corporates, particularly in high-impact sectors like the energy sector and agriculture.

2025 Milestones:

Investors rapidly adopted metrics on dependencies, and heightened awareness around environmental impact from extreme weather events pushed nature onto corporate agendas.

What to Watch:

GRI remained the primary framework for impact-focused sustainability disclosures in 2025, especially for stakeholders beyond investors. It continues to anchor corporate transparency around renewable energy, labour practices, and community engagement.

2025 Developments:

Revised GRI Climate and Energy topic standards were published, updating requirements on:

These revisions were designed to improve interoperability with ESRS climate and energy datapoints, making it easier for companies to map disclosures across frameworks.

What to Watch:

For more information on GRI, TNFD, and ESRS updates, check out our blog post here.

SASB standards remained the primary reference for sector-specific ESG metrics in 2025, even as they moved under the ISSB umbrella.

2025 Updates:

Exposure drafts proposing amendments to SASB standards were released to better align with IFRS S1/S2. Updates addressed:

Listed corporates in 2025 increasingly used SASB metrics to benchmark esg performance against peers for investors and ratings providers.

What to Watch:

Contact Nossa Data for support with streamlining and aligning your annual reporting disclosures & processes

2025 marked a turning point where ESG ratings and benchmarks shifted from unregulated market tools to activities under direct or indirect regulatory oversight. Listed corporates increasingly had to manage ratings governance: who they respond to, how they validate data, and where they reference ratings in annual reports and prospectuses.

Policymakers in 2025, particularly in the EU and UK, advanced frameworks to regulate ESG ratings providers, moving them closer to being treated as regulated financial services.

2025 Developments:

What Corporates Need to Know:

For an overview of the top ESG rating agencies assessing listed companies, see this guide.

CDP sharpened its role as a de facto climate data standard in 2025, with more investors using CDP outputs to supplement regulatory disclosures.

2025 Recap:

CDP scores and the A-List publication had noticeable reputational impact for listed corporates, influencing investor perception and, in some markets, banking relationships related to sustainability reporting.

What to Watch:

The S&P Global Corporate Sustainability Assessment (CSA) remained a critical benchmark in 2025, especially for inclusion in major sustainability indices.

2025 Recap:

What to Watch:

EcoVadis’ influence expanded in 2025 from a procurement tool into a broader ESG performance signal used by customers, lenders, private sector investors, and private equity.

2025 Recap:

What to Watch:

2025 saw growing use of thematic ESG datasets to contextualise companies’ own disclosures, especially on workforce and access to justice topics.

2025 Updates:

What to Watch:

Contact Nossa Data for end-to-end disclosure integration with ESG benchmark platforms, assessing scoring gaps, & ensuring AI-readiness of your ESG data

2025 rewarded companies that had already invested in centralised ESG data models, clear governance structures, and cross-functional reporting calendars.

Leaders

Laggards

ESG systems outperformed spreadsheets. Companies that had sorted their data models were already ahead—able to enhance resilience, reduce compliance burdens, and respond to investor and regulatory requirements with confidence.

2025 did not roll back ESG—it clarified, delayed selectively, and raised expectations on quality and assurance.

Key Takeaways for 2026:

The sectors which invested in structured, centralisable ESG data are positioned to enhance transparency, meet evolving regulatory requirements, and drive value creation—regardless of which framework takes precedence in any given jurisdiction.

For companies still relying on patchwork approaches, 2026 will require a shift toward unified ESG data platforms that can handle reporting, regulation, and ratings all at the same time. That’s exactly what solutions like Nossa Data are built to solve.

Do companies still need to report against multiple frameworks after 2025?

Yes, they do. 2025 showed that overlap between ESRS, ISSB, GRI, TNFD, and ratings platforms like CDP and EcoVadis is unavoidable. The key advantage comes from structuring ESG data once and being able to map it across all the different frameworks. Rather than duplicating effort, companies that build a single, centralised data layer can respond to sustainability reporting requirements across jurisdictions without starting from scratch each time. This is the approach that platforms like Nossa Data enable—helping companies manage ESG initiatives, voluntary ESG disclosures, and mandatory requirements from a unified foundation.

How do the new EU/UK “Rate the Raters” regulations affect corporates directly?

In effect, ESG ratings are now treated as regulated financial information in key markets. Post-2025, companies need a clear grip on how they select, reference, and explain their ratings. This means establishing governance around which ratings providers you engage, understanding investor rights to challenge methodologies, and ensuring any ratings referenced in annual reports or prospectuses can be substantiated. Companies will also need to manage how changes in ratings are communicated, especially where ESG performance influences sustainable finance relationships or index inclusion.

How should smaller or non-EU listed companies prepare if they are not yet in CSRD scope?

Even if not directly subject to the corporate sustainability reporting directive, smaller companies should begin preparing now. Practical steps include conducting early materiality assessments aligned with double materiality principles, upgrading data systems to capture ESG metrics systematically, and mapping current disclosures to ISSB requirements. Many such companies will face indirect pressure through global supply chains—large customers subject to CSRD or EU taxonomy requirements may request enhanced ESG data from suppliers. Early preparation also positions companies to respond to investor expectations and potential future regulatory requirements in their home jurisdictions.

How can companies manage ESG litigation and greenwashing risk after 2025?

The heightened regulatory scrutiny of 2025 brought increased litigation risk around climate targets, AI use in ESG claims, and supply chain diligence. To manage this, companies should establish robust internal controls around ESG data quality and disclosure sign-off. Seeking independent assurance for key sustainability disclosures—particularly around climate commitments and net zero targets—adds credibility and reduces exposure. Transparency is essential: avoid overclaiming on ESG factors or making forward-looking statements without clear evidence and methodologies. Companies should also monitor developments around industrial strategy and European competitiveness initiatives, which may influence enforcement priorities.

What was the biggest operational lesson of 2025?

Calendars matter. Companies that succeeded in 2025 had integrated ESG data management systems that could meet overlapping deadlines for CSRD, CDP, CSA, EcoVadis, and national filings without version-control chaos or data quality issues. The lesson is clear: shift away from patchwork reporting toward a single, structured ESG data layer that can handle reporting, regulation, and ratings simultaneously. That operational shift—supported by economic growth in ESG technology—is now a competitive differentiator for listed corporates navigating climate change, global warming pressures, and energy transition demands.