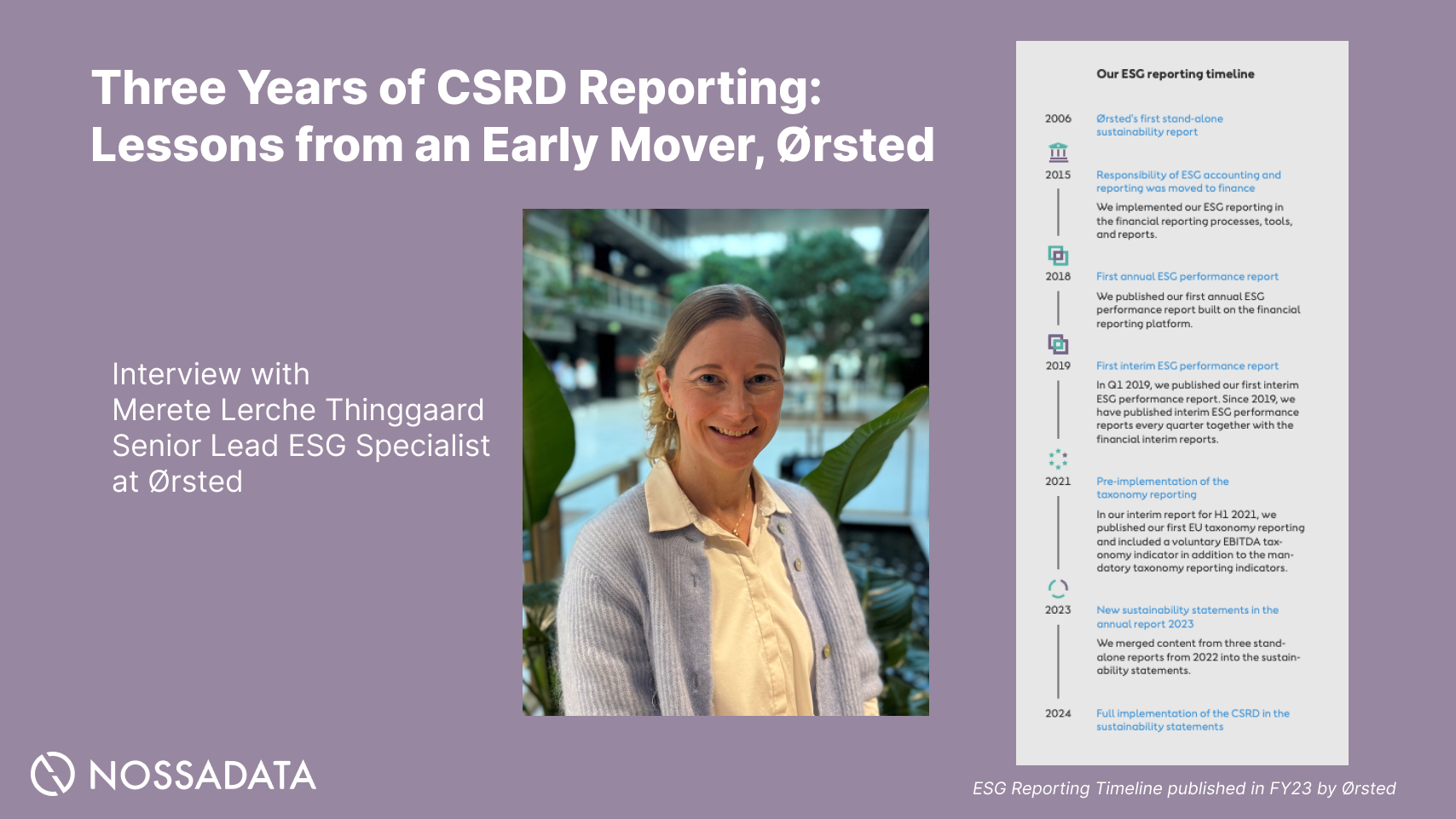

Interviews

Three Years of CSRD Reporting: Lessons from an Early Mover, Ørsted

An expert interview with Merete Lerche Thinggaard, Senior Lead ESG Specialist at Ørsted, on three CSRD reporting cycles.

The patchwork of sustainability reporting finally has a solution. Since January 2024, companies worldwide are navigating a new era of standardised sustainability disclosure requirements under the International Sustainability Standards Board (ISSB) framework. This is the biggest change in corporate sustainability reporting since environmental reporting itself.

This guide covers ISSB regulation from the foundation standards to country by country implementation, practical compliance steps and the role of these regulations in how businesses communicate their sustainability performance to capital markets.

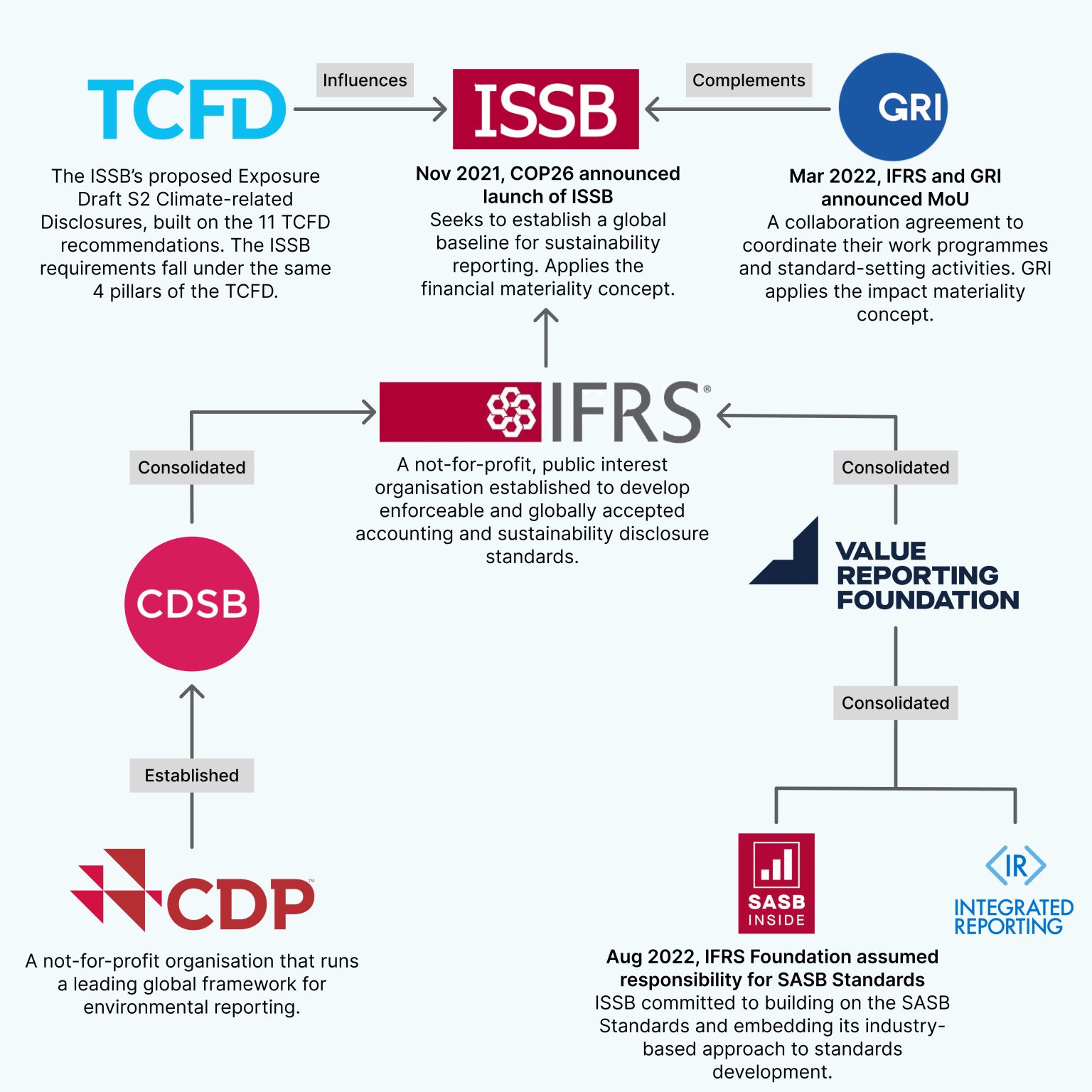

The International Sustainability Standards Board (ISSB) was set up at COP26 under the IFRS Foundation to create global baseline sustainability standards to address the fragmentation in sustainability reporting. This had direct support from G7, G20, IOSCO and the financial stability board, showing unprecedented international agreement on the need for standardised sustainability related financial information.

IFRS S1 and IFRS S2 became effective January 1, 2024 and set the foundation for sustainability disclosures globally. These IFRS sustainability disclosure standards require companies to disclose sustainability related risks and opportunities that may impact their prospects over short, medium and long term, including complying with the requirements of IFRS S1.

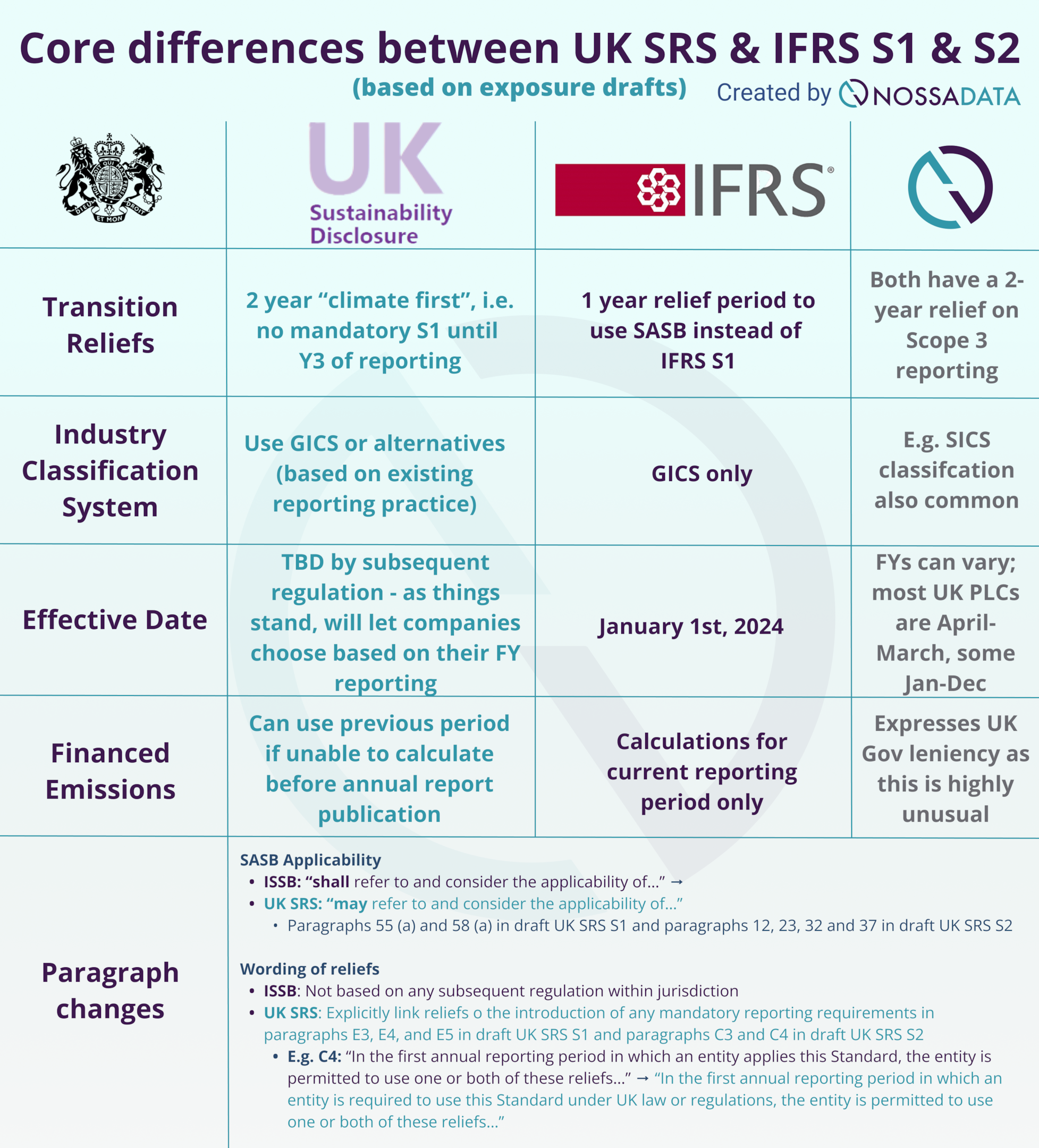

The UK Government is developing UK sustainability reporting standards (UK SRS) based on IFRS S1 and S2 with the Technical Advisory Committee recommending endorsement in December 2024. The expected effective date for UK implementation is no earlier than January 1, 2026 but voluntary adoption can start sooner.

The sustainability standards board ISSB designed these standards to work alongside existing financial reporting frameworks, requiring disclosure of sustainability related risks through four core pillars: governance processes, strategy, risk management and metrics and targets. Companies must provide disclosures that are decision-useful for primary users of general purpose financial reports.

Implementation includes transitional reliefs for comparative information and Scope 3 greenhouse gas emissions reporting and coordination mechanisms to avoid duplication with existing climate related financial disclosures requirements like TCFD.

The International Sustainability Standards Board is an independent global standard-setting body under the IFRS Foundation governance, working alongside the International Accounting Standards Board (IASB) to create comprehensive corporate reporting standards. The ISSB’s mission is to develop sustainability disclosure standards that provide comparable, decision-useful information for capital markets and other primary users of corporate reports.

This international body came out of the consolidation of several existing sustainability frameworks including the Sustainability Accounting Standards Board (SASB), Climate Disclosure Standards Board (CDSB) and the Value Reporting Foundation (VRF). The merging of these previously separate initiatives eliminated the confusion and duplication that existed in the pre-2021 sustainability reporting landscape.

The ISSB framework provides a global baseline, so jurisdictions can adopt these standards as minimum requirements and add local requirements on top. This ensures comparability across international markets while allowing for regional regulatory needs and priorities.

The sustainability standards framework is based on the principle that sustainability related financial information should meet the same quality standards as financial statements. Companies must apply the same rigorous approach to identifying sustainability related risks and managing sustainability related risks as they do to financial risk management processes.

Support for the ISSB regulation goes beyond regulatory bodies to include major institutional investors, multinational corporations and professional accounting organisations. This broad backing reflects the recognition that standardised sustainability disclosures are essential for efficient capital allocation and risk assessment in modern markets.

IFRS S1 sets out the general requirements for disclosure of sustainability related financial information, creating a framework for reporting all material sustainability factors that could impact a company’s prospects. The standard requires entities to disclose sustainability related risks and opportunities through four interconnected areas: governance, strategy, risk management and metrics and targets.

The governance requirements under IFRS S1 require entities to disclose how their governance processes and controls monitor sustainability related risks and the role of management in assessing and managing those risks. Companies must explain how governance bodies oversee sustainability matters and integrate them into strategic decision-making processes.

Strategy disclosures require entities to explain how sustainability related risks and opportunities impact their business models, strategy and financial planning processes. This includes describing the entity’s strategy for managing sustainability related risks and how current and anticipated regulatory, market and technological changes might impact future performance.

IFRS S2 builds on the general requirements and adds climate related disclosures that are based on the task force on Climate-related Financial Disclosures framework. The standard uses the greenhouse gas protocol for emissions measurement and requires disclosure of Scope 1, Scope 2 and where material, Scope 3 greenhouse gas emissions.

Climate related targets under IFRS S2 must include specific metrics, timelines and progress indicators. Companies must disclose their climate related changes in strategy, including transition risks and physical risks, and scenario analysis that demonstrates resilience under different climate scenarios.Both standards have industry specific disclosures, referencing industry based SASB standards for sector specific metrics and disclosure requirements. This ensures companies provide relevant and comparable information while addressing the unique sustainability challenges and opportunities within their industries.

The January 1, 2024 effective date for annual reporting periods means companies must integrate these requirements into their existing financial reporting cycles and provide sustainability related disclosures alongside their financial statements.

The UK’s approach to ISSB regulation is one of the most advanced national implementation processes globally. The UK Government consultation on the UK SRS runs until September 17, 2025, with the Secretary of State for Business and Trade making final endorsement decisions following technical review.

The expected UK SRS effective date is no earlier than January 1, 2026, giving entities plenty of time to prepare for mandatory sustainability related financial disclosures. However, voluntary use is expected to start earlier, particularly for entities already subject to existing climate related financial disclosures requirements.

The UK framework is GAAP-agnostic, meaning UK sustainability reporting standards will be compatible with both IFRS and UK GAAP reporting entities. This flexibility ensures broad applicability while maintaining consistency with the global baseline set by the ISSB.

The Technical Advisory Committee plays a key role in the UK’s ISSB regulation implementation, providing technical assessment and endorsement recommendations for IFRS sustainability disclosure standards. The TAC’s December 2024 recommendation to endorse IFRS S1 and S2 with only minor UK-specific amendments shows the strength of the global baseline approach.

The TAC has diverse professional membership supported by the financial reporting council, including experts in accounting, sustainability, assurance and legal matters. This multi-disciplinary approach ensures comprehensive evaluation of technical requirements and practical implementation considerations.

The public call for evidence process maintains transparency through published papers, meeting recordings and detailed documentation on the FRC website. This openness allows stakeholders to understand the reasoning behind endorsement decisions and provides confidence in the technical rigour of the process.

The Policy and Implementation Committee coordinates UK SRS implementation across government departments, ensuring alignment with the UK sustainability disclosure policy and preventing regulatory duplication. The PIC reviews interactions between new sustainability requirements and existing departmental responsibilities.

Information sharing between UK regulators and government bodies ensures consistent interpretation and application of sustainability disclosure standards across different sectors and regulatory frameworks. This coordination is important for entities subject to multiple regulatory requirements.

The committee’s approach includes private meetings with public summary minutes, so transparency while allowing for open discussion of implementation challenges and coordination issues between different regulatory bodies.

The ISSB framework has carefully designed transitional relief to support implementation while maintaining the integrity of sustainability disclosures. The one year delay on comparative information requirements recognises that many companies will be reporting sustainability for the first time.

Relief for Scope 3 greenhouse gas emissions reporting acknowledges the complexity and resource required to measure value chain emissions. These reliefs give companies time to develop robust measurement and verification systems while ensuring material Scope 3 emissions are disclosed.

The Technical Advisory Committee is actively collecting feedback on the sufficiency of transitional relief to ensure implementation support evolves based on practical experience. This responsive approach helps identify additional support needs while maintaining confidence in sustainability disclosures.

Support for companies building sustainability reporting capabilities goes beyond regulatory relief to include guidance materials, training programs and best practice sharing initiatives. These resources help companies develop the systems and expertise for ongoing compliance.

IFRS S2 alignment with existing climate related financial disclosures is a big advantage for companies already reporting under TCFD. The integration means companies can leverage existing processes and data to meet ISSB requirements without starting from scratch.

Extension beyond TCFD recommendations within the IFRS framework provides more clarity and specificity while maintaining the architecture many companies have already implemented. This reduces implementation cost and complexity.

The Policy and Implementation Committee’s analysis of overlaps with existing UK legislation helps prevent duplication and ensures a smooth transition from current requirements to enhanced sustainability disclosure standards. This coordination is important to maintain regulatory efficiency and reduce compliance burden.

Companies already applying TCFD requirements have a head start as they have developed many of the governance processes, risk management systems and metrics required for IFRS S2. However, there is still work to be done to gap analysis and system upgrades.

The upcoming consultation on mandatory assurance for sustainability disclosures recognises the importance of reliable verified information for capital market decision making. Draft regulations for triennial Audit and Assurance Policy Statements provide the framework for consistent assurance standards.

ISAE 5000 standard for sustainability assurance published in November 2024 provides the technical framework for independent verification of sustainability related financial information. This standard sets the foundation for consistent assurance practices across different jurisdictions and sectors.

ICAEW, government and the Financial Reporting Council (FRC) are working together on assurance frameworks to ensure sustainability disclosures are of the same quality as financial statements. This coordination is key to maintaining market confidence in sustainability information.

Data collection processes and organisational education requirements go beyond technical compliance to include the systems, controls and expertise needed for ongoing sustainability reporting. Companies must invest in these foundation elements to be sustainable compliant.

Gap analysis for current governance and sustainability strategy compliance is the foundation for implementation planning. Companies must assess their current processes against IFRS S1 and S2 to identify what needs to be developed or enhanced.

Sustainability roadmaps with clear milestones and responsibilities will ensure implementation is coordinated across different parts of the organisation. These roadmaps must cover technical requirements, system development, staff training and integration with existing reporting processes.

Resource planning and allocation for sustainability reporting preparation requires significant investment in technology, people and training. Companies must budget for initial implementation costs and ongoing operational costs to be compliant.

Establishing data collection systems is one of the biggest challenges of implementation, particularly for Scope 3 emissions and other value chain information. Companies must develop robust measurement, verification and reporting systems that can withstand external assurance.

Coordination with financial statement preparation and reporting cycles will ensure sustainability disclosures integrate with existing reporting processes. This integration is key to maintaining narrative consistency and operational efficiency.

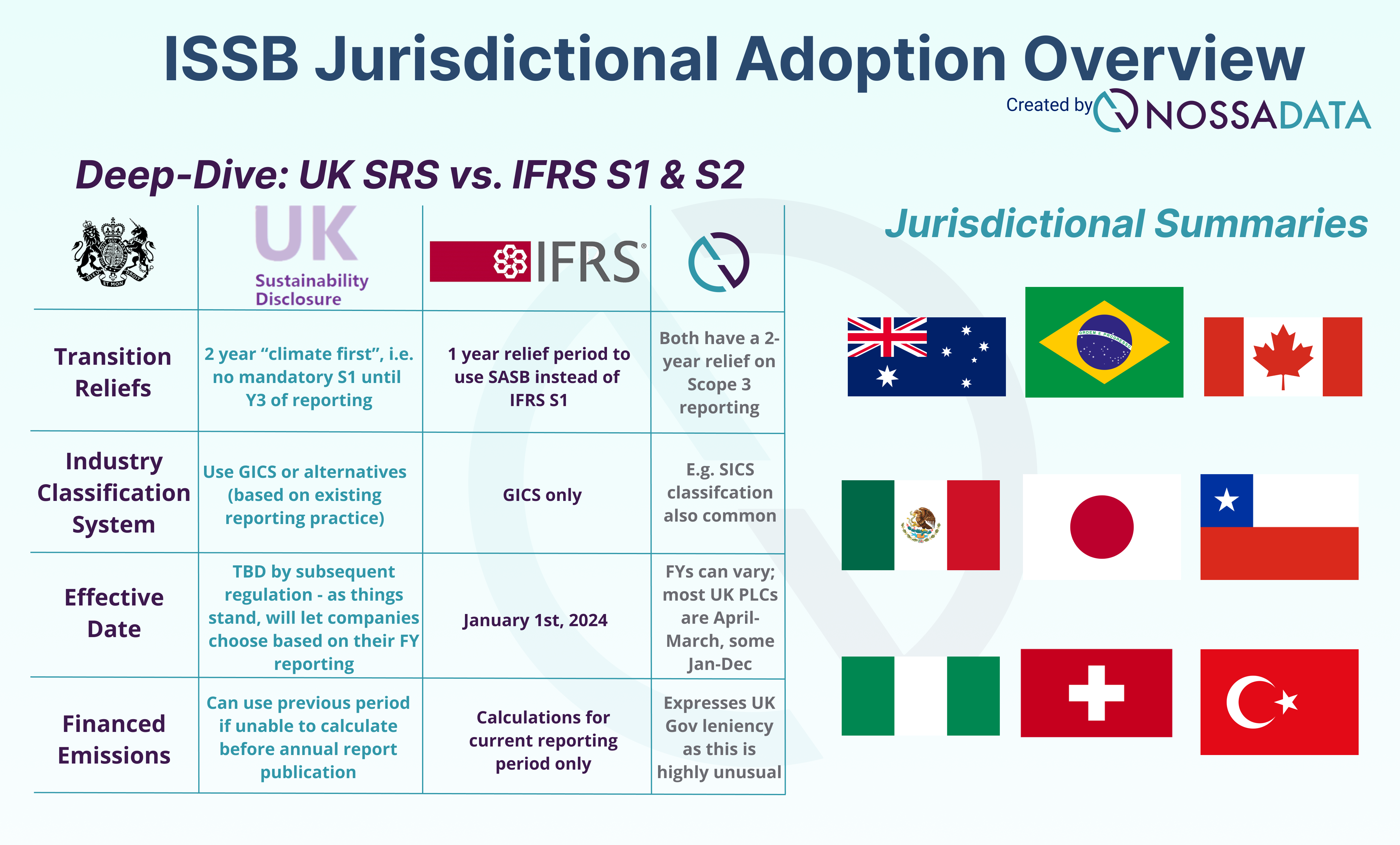

The IFRS Foundation has provided a breakdown of jurisdictional profiles and adoption across 35 jurisdictions (so far) that are using IFRS S1 and IFRS S2 in their existing or incoming ESG reporting regulation. We have summarised 9 of these below to show the scope and approach of major economies in their respective regions.

Australia’s approach to ISSB adoption shows the balance between global alignment and local regulatory needs. The Australian Accounting Standards Board is consulting on adopting ISSB regulation, with implementation expected to start in 2025 for large listed entities and financial institutions.

The Australian framework is substantially aligned with the global baseline but has transitional provisions for entities that don’t have existing sustainability reporting infrastructure. The phased approach prioritises publically accountable entities and large private companies, giving smaller entities more time to develop the necessary systems and processes.

Key features of Australia’s implementation include coordination with existing climate related financial disclosures and integration with the Australian Securities and Investments Commission’s regulatory framework. The approach allows entities already reporting under TCFD to use existing processes to meet ISSB standards.

The Australian consultation process specifically looks at the interaction between ISSB standards and local environmental regulations to ensure sustainability disclosures don’t duplicate existing requirements. This coordination prevents unnecessary burden while maintaining the global baseline.

Brazil’s convergence with ISSB regulation shows the country’s commitment to sustainable finance and environmental transparency. The Comitê de Pronunciamentos Contábeis (CPC) is leading the national adoption process, consulting with stakeholders on material implementation issues and sector specific applications.

The Brazilian approach integrates with existing sustainability initiatives, including the country’s environmental disclosure requirements for listed companies. This coordination allows Brazilian entities to build on current practices while meeting global standards for sustainability related financial information.

Implementation in Brazil will consider the capacity of different sectors to develop robust sustainability reporting systems. The phased approach will allow for industry specific guidance and support, particularly for sectors with limited experience in comprehensive sustainability disclosures.

The Canadian Sustainability Standards Board (CSSB) is working closely with the ISSB to achieve substantial alignment with global standards while addressing unique aspects of the Canadian market. Canada’s approach will coordinate between federal and provincial regulators to ensure consistent implementation across jurisdictions.

Canadian implementation will focus on publicly accountable entities first, with provisions for extending requirements to other entity types based on market development and stakeholder needs. The framework will include specific guidance for entities operating in multiple jurisdictions, addressing potential conflicts between different regulatory requirements.

The consultation in Canada will look at the relationship between ISSB standards and existing climate related disclosures to ensure a smooth transition for entities already reporting under federal climate disclosure requirements.

Chile’s roadmap for ISSB regulation shows the country’s commitment to sustainable capital markets. The Superintendency of Securities and Insurance will coordinate implementation for public companies and large financial institutions, prioritising integrated reporting approaches that link sustainability and financial information.

The Chilean framework will provide capacity building and technical support for preparers, recognising that many entities will need additional resources to implement comprehensive sustainability related disclosures. This support will include guidance materials, training programs and transition periods for complex disclosure requirements.

The Sustainability Standards Board of Japan is developing Japanese Sustainability Standards that reference IFRS S1 and IFRS S2 as the foundational framework while incorporating local market characteristics and legal requirements. Japan’s approach balances global comparability with domestic regulatory coordination.

Japanese implementation includes specific provisions for coordination with existing environmental reporting requirements and integration with Japan’s corporate governance framework. The phased approach allows entities to begin with voluntary adoption while building toward broader mandatory requirements.

The framework addresses the unique needs of Japanese multinational corporations that operate across multiple regulatory jurisdictions, providing guidance for entities that must comply with various international sustainability reporting requirements.

Mexico’s approach to ISSB regulation adoption involves the Mexican Council for Financial Reporting Standards reviewing IFRS S1 and S2 for formal endorsement within the country’s existing regulatory framework. The implementation strategy focuses initially on regulated sectors and publicly traded companies.

The Mexican framework emphasizes coordination with existing environmental and social disclosure requirements, ensuring that entities can build upon current practices while meeting enhanced global standards. This approach minimizes duplication while strengthening the overall quality of sustainability related financial information.

Nigeria’s Financial Reporting Council is advancing toward phased ISSB adoption for public interest entities, with particular attention to capacity building and implementation support. The approach recognizes the need for substantial infrastructure development to support comprehensive sustainability reporting.

The Nigerian framework includes provisions for technical assistance and guidance for preparers, acknowledging that many entities will require significant support to implement robust sustainability disclosure systems. This support extends to training programs, template materials and phased implementation timelines.

Switzerland’s integration of ISSB regulation involves amendments to the Swiss Code of Obligations for public companies, with particular relevance for entities listed on multiple international exchanges. The approach emphasizes coordination with EU regulatory requirements while maintaining alignment with global standards.

Swiss implementation includes specific provisions for entities subject to multiple regulatory jurisdictions, providing guidance for companies that must navigate overlapping sustainability disclosure requirements across different markets.

The Public Oversight, Accounting, and Auditing Standards Authority in Türkiye is converging Turkish sustainability standards with the ISSB regime for public companies. The approach begins with voluntary adoption and includes plans for broader mandatory implementation based on market development.

Türkiye’s framework emphasizes the development of local expertise and technical capacity to support effective implementation of sustainability related disclosures. This includes coordination with professional bodies and educational institutions to build necessary skills and knowledge.

When do ISSB standards become mandatory in the UK? When do I have to report under UK SRS?

First reporting is expected to be for the financial year starting 1 January 2026, so reports would be filed in 2027. However the Secretary of State for Business and Trade will make the final decision after the consultation process and Technical Advisory Committee recommendations.

What transitional reliefs are available for first time adopters?

Transitional reliefs include relief from providing comparative information in the first year of adoption and phased implementation of Scope 3 greenhouse gas emissions reporting. This helps entities manage the complexity of first time implementation while ensuring material information is disclosed.

How do ISSB standards interact with TCFD?

IFRS S2 fully incorporates and extends TCFD recommendations, so entities already reporting under TCFD can use existing processes to meet the new requirements. It eliminates duplication and strengthens the comprehensiveness and comparability of climate related disclosures.

What assurance is required for sustainability disclosures?

While ISSB standards do not require assurance, there is strong regulatory pressure for mandatory external assurance, particularly in the UK. ISAE 5000 is the technical standard for sustainability assurance and is expected to become mandatory for many entities.

Who should I contact for guidance on UK SRS?

FRC provides official guidance on UK sustainability disclosure policy, supported by the Technical Advisory Committee and government consultation processes. You can also find resources through professional bodies like ICAEW and industry associations.

What is the difference between IFRS S1 and IFRS S2?

IFRS S1 sets out general requirements for disclosure of all material sustainability related financial information, while IFRS S2 sets out specific requirements for climate related disclosures. S1 covers governance, strategy, risk management and metrics across all sustainability topics, while S2 focuses on climate related risks and opportunities, including greenhouse gas emissions and climate targets.

How does the UK endorsement process work for ISSB?

The UK endorsement process involves technical review by the FRC and Technical Advisory Committee, public consultation and final endorsement decision by the Secretary of State for Business and Trade. All documentation and analysis supporting the endorsement decisions are publicly available.

What support is available to help me prepare?

Implementation support includes step by step guidance materials, best practice workshops, regulatory Q&A sessions, template resources through government bodies and professional organisations. You can also access training programs and technical assistance to build your capabilities.

AI will help reduce the disclosure burden for preparing and disclosing on ISSB regulation, with SaaS tools like Nossa Data’s ESG Reporting Tool helping companies to centralise & align their data across 30+ frameworks & custom reporting templates.

The change represented by ISSB regulation goes far beyond compliance to fundamentally change how businesses understand, manage and communicate their sustainability performance. As companies worldwide adopt these standards, the transparency and comparability will drive better capital allocation, improved risk management and greater stakeholder trust.

Companies that approach ISSB implementation strategically, investing in robust systems and processes and using transitional reliefs wisely will not only meet the requirements but get ahead in the increasingly sustainability focused markets. Time to get ready as the global move to standardised sustainability reporting is one of the biggest changes in corporate disclosure in decades.