Interviews

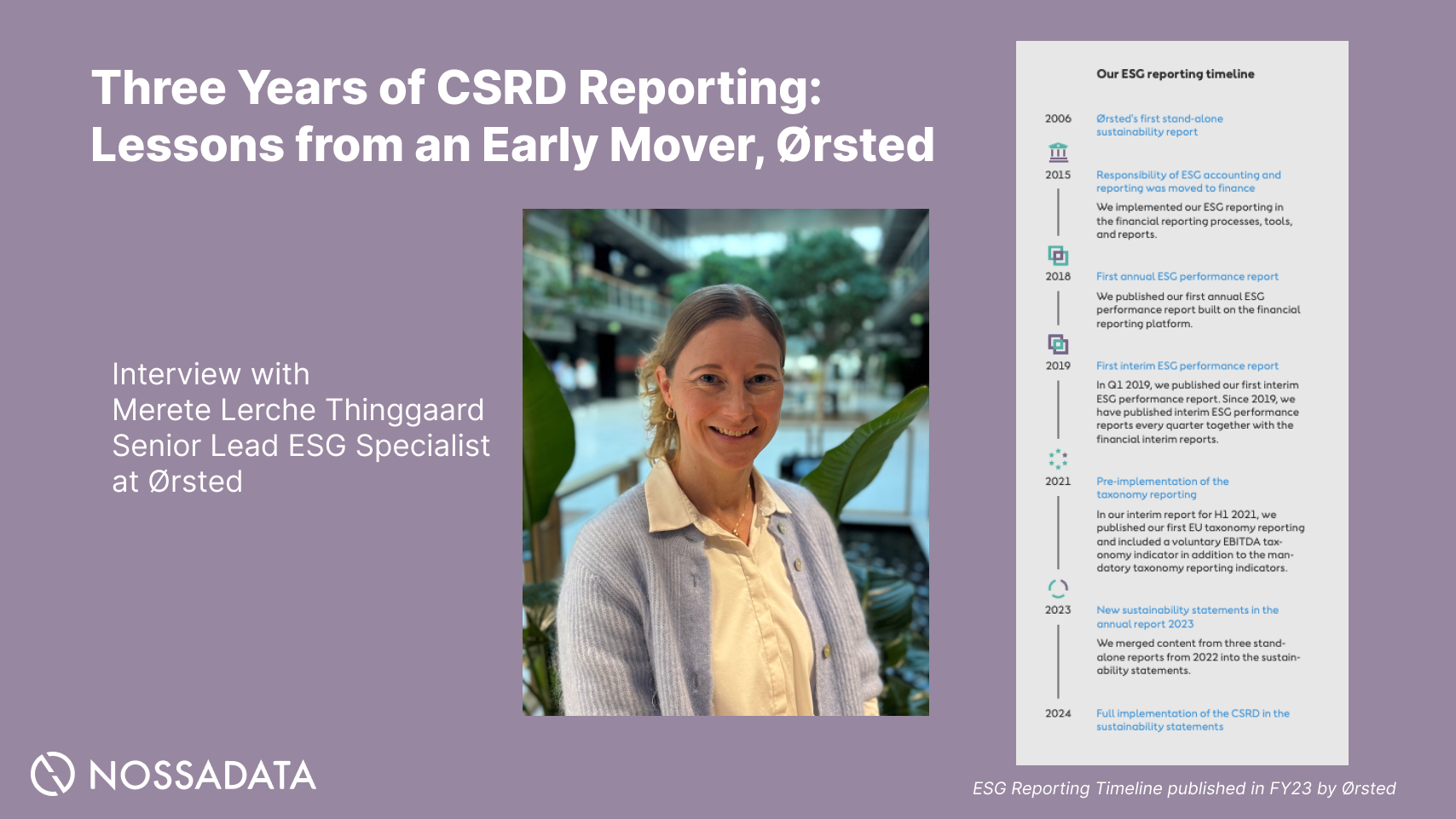

Three Years of CSRD Reporting: Lessons from an Early Mover, Ørsted

An expert interview with Merete Lerche Thinggaard, Senior Lead ESG Specialist at Ørsted, on three CSRD reporting cycles.

At Nossa Data, we are proud to disclose that our ESG reporting software is an accredited and acclaimed ESG software that ensures reporting requirements are met, serving various organisations globally, including PensionBee, Vodafone, and more. Nossa Data provides tools to improve their ESG and makes their reporting processes more efficient. Nossa Data is CDP Accredited, an EcoVadis Training Partner, and more to help both large listed companies and smaller companies subject to requirements (regardless of where you are on your journey) to be more able to drive business value and gain ROI, using just one platform. Nossa Data is a Friend of EFRAG - Sustainability and are proud of our support to business transparency; EFRAG is an independent body bringing standardisation to annual reporting.

CSRD: An Overview

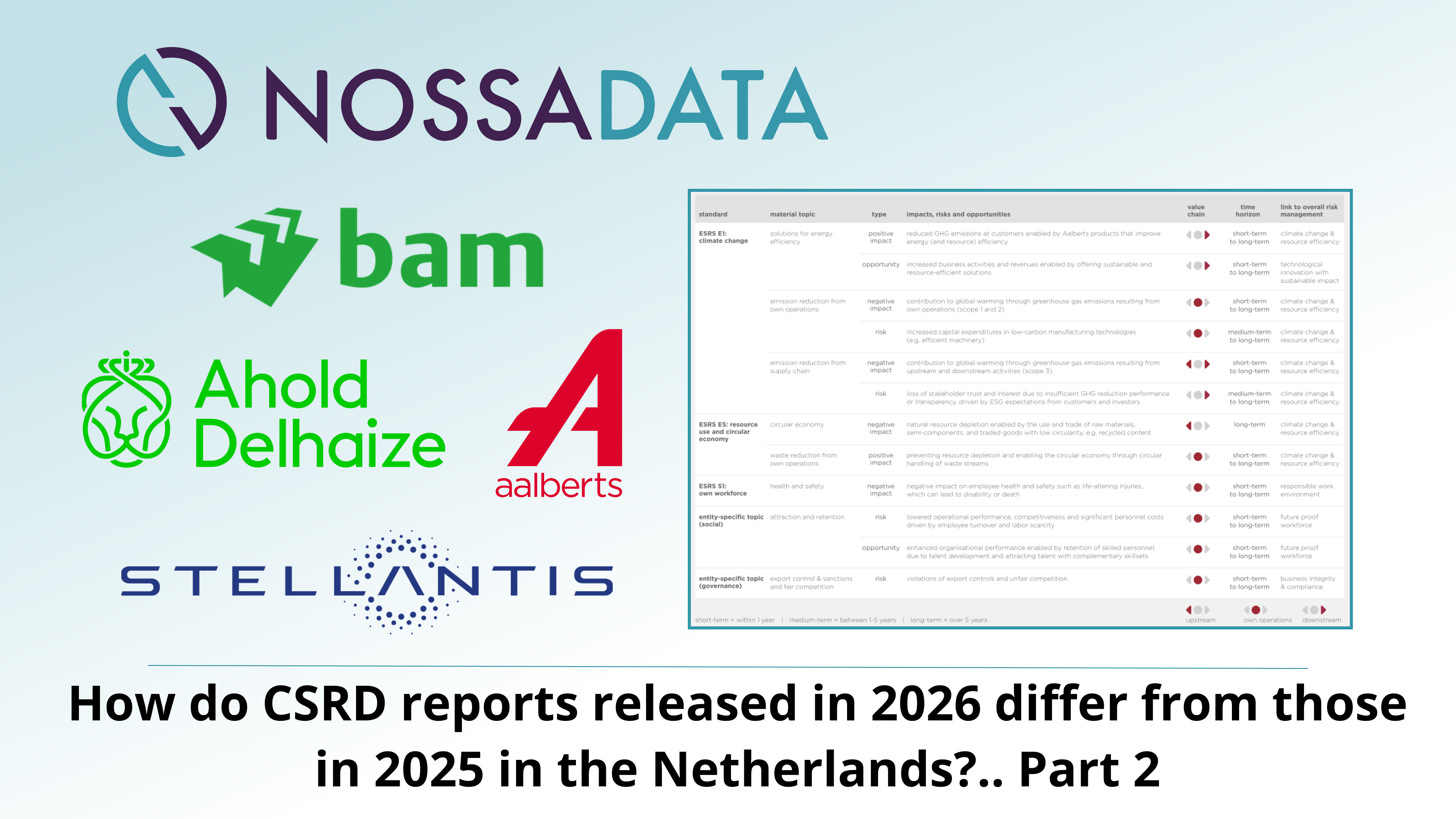

Last year we reviewed 25 Netherlands ESRS/CSRD reports to understand how companies approached the first wave of ESRS-aligned reporting. This year, because we’re early in the annual reporting cycle, fewer FY2025 reports (published in 2026) are available; so this is a smaller, sharper sample of five companies, focusing on what changes after the “first-time reporting” year. A couple weeks ago I analysed the differences for four companies in the Netherlands. Here, I’ve now taken a quick look at these companies:

Aalberts has clearly moved into “year-2 execution mode” in its public narrative; the 2025 annual report publication highlights continued work on sustainability initiatives and explicitly calls out Scope 1-3 reductions and “decarbonisation levers” alongside broader operating-model updates. What looks different based on what’s accessible right now?

To ensure the effectiveness and reliability of its sustainability disclosures under CSRD, Aalberts incorporates a robust evaluation process as part of its reporting framework, supporting transparency and continuous improvement.

Ahold Delhaize’s sustainability statements are presented as a self-contained package within the annual report ecosystem; with downloadable “Sustainability statements” sections for 2024, and a clearly partitioned ESG structure visible in the 2025 annual report PDF/print table-of-contents. Themes that stand out YoY:

Pragmatic read; Ahold’s year-2 story (from what we can access) looks like a shift from “getting the sustainability statements publishable” to “making them auditable, navigable, and repeatable”; especially around workforce/social datapoints and scope articulation.

Stellantis is one of the clearest “before/after” examples in this sample.

FY2024; E4 effectively treated as non-material (omitted);

FY2025; E4 becomes a visible, structured ESRS block;

Pragmatic read; this is exactly what “second-year reporting” often looks like; materiality and topic boundaries are recalibrated, and a topic that was previously handled as “out of scope” becomes a structured disclosure block once the organisation has baseline processes to support it.

For BAM, we have strong visibility into FY2025 because the company publishes the sustainability statement as its own PDF section.

FY2025; explicit DMA maintenance + change log;

FY2024; stakeholder/double materiality framing is present, but less delta-focused in what we could access;

Pragmatic read; BAM’s year-2 shift is a move toward traceability of materiality maintenance; not just “we did a DMA,” but “here’s what dropped out, here’s what came in, and here’s who validated it.”

A common undercurrent in second-year reports is the pragmatic use of relief mechanisms. Relief mechanisms, such as those available under streamlined energy and carbon reporting frameworks, help companies manage environmental disclosure requirements more efficiently. The European Commission’s “quick fix” amendments were designed to reduce burden for first-wave companies (e.g., extending the ability to omit certain anticipated financial effects for FY2025 and FY2026), and major accounting firms summarised the effect as “breathing space” while simplification continues.

We’ll keep tracking how year-2 CSRD reports evolve as more FY2025 annual reports publish through the spring; especially how companies (1) maintain DMA credibility, (2) handle comparatives and restatements, and (3) decide what to treat as material vs “not material / phased-in” without losing stakeholder trust.

As sustainability standards continue to evolve, companies will need to adapt their reporting practices to maintain compliance and transparency.

The CSRD primarily targets EU companies, but also has implications for UK companies and non-EU entities with significant EU operations. The evolving ESG reporting requirements under the CSRD and ESRS frameworks are driving changes in how companies approach sustainability and regulatory disclosures. The CSRD was published in the official journal of the European Union, establishing its legal force and formalizing the new standards. Some companies in the sample also include voluntary disclosures in their reports, going beyond mandatory requirements to enhance transparency and stakeholder trust.

Regulatory bodies are driving the transformation in sustainability reporting at breakneck speed, setting the pace and direction for how financial institutions, investment firms, and large companies approach their ESG disclosures. As of 2024-2025, the regulatory reporting landscape is evolving rapidly, with organizations increasingly required to align with more detailed reporting requirements—ensuring that sustainability information isn't just an add-on, but becomes a core part of their annual financial report and business strategy.

The Corporate Sustainability Reporting Directive (CSRD) serves as a prime example of this shift. By updating and expanding the reporting requirements for companies subject to EU law, the CSRD ensures that both public interest entities and large companies operating in the European Union must disclose information on environmental matters, human rights, and other sustainability risks. The European Sustainability Reporting Standards (ESRS), developed by the European Financial Reporting Advisory Group (EFRAG), provide the detailed framework for these disclosures, adopting a double materiality perspective. This means companies must report not only on how sustainability issues impact their financial performance, but also on how their operations affect people and the environment—a comprehensive approach that's becoming the global standard.

Regulatory bodies such as the Prudential Regulation Authority (PRA) in the UK and the European Banking Authority (EBA) play a pivotal role in translating these high-level directives into actionable regulatory reporting requirements. For example, the PRA has introduced clear guidelines for UK registered companies and PRA-designated investment firms to manage and disclose climate related financial risks, integrating these considerations into risk management and strategic decision making. Similarly, the EBA's technical standards on Pillar 3 disclosures require credit institutions and investment firms to report on ESG risks, using standardized reporting templates to ensure consistency and comparability across the financial industry.

Oversight and supervision represent key functions of these regulatory bodies moving forward. The Financial Stability Board (FSB) and the European Commission monitor the implementation of sustainability reporting standards, ensuring that companies comply with the latest delegated acts and regulatory requirements. This supervision helps safeguard financial stability by making climate related risks and other sustainability risks more transparent, enabling asset managers, asset owners, and investors to make better-informed investment decisions based on decision-useful information.

Beyond enforcement, regulatory bodies provide practical support to help companies navigate the complex reporting landscape effectively. The EBA, for instance, offers detailed reporting templates and guidance for disclosing ESG risks, while the PRA issues regular updates and best practice recommendations for managing climate related financial disclosures. These resources prove essential for companies aiming to meet the expectations of the CSRD, ESRS, and other sustainability reporting standards, especially as the requirements become more granular and audit-ready across different jurisdictions.

Ultimately, the influence of regulatory bodies extends well beyond compliance requirements. By setting clear reporting standards and fostering a culture of transparency and accountability, they drive the integration of sustainability into corporate reporting and risk management frameworks. This approach not only supports investor protection and financial stability, but also encourages companies to embed sustainability into their core business strategy—ensuring that the financial system becomes resilient, responsible, and aligned with the long-term interests of society and the environment in an evolving regulatory landscape.