Interviews

Three Years of CSRD Reporting: Lessons from an Early Mover, Ørsted

An expert interview with Merete Lerche Thinggaard, Senior Lead ESG Specialist at Ørsted, on three CSRD reporting cycles.

.png)

At Nossa Data, we are proud to disclose that our ESG reporting software is an accredited and acclaimed ESG software that ensures reporting requirements are met, serving various organisations globally, including PensionBee, Vodafone, and more. Nossa Data provides tools to improve their ESG and makes their reporting processes more efficient. Nossa Data is CDP Accredited, an EcoVadis Training Partner, and more to help both large listed companies and smaller companies subject to requirements (regardless of where you are on your journey) to be more able to drive business value and gain ROI, using just one platform. Nossa Data is a Friend of EFRAG - Sustainability and are proud of our support to business transparency; EFRAG is an independent body bringing standardisation to annual reporting.

Last year we reviewed 25 Netherlands ESRS/CSRD reports to see how companies approached the first wave of ESRS-aligned reporting. This year, because we’re early in the annual reporting cycle, fewer FY2025 reports (published in 2026) are available to access, so we’re starting with a smaller, sharper sample, where we are interested to understand early changes in information, standards, activities, impact, social data (employees, customers, reputation, et.c), and more, between FY25 and FY24, upon changes to interpretations of obligations.

In this article, we zoom in on the world and just analyse four Dutch companies reporting under CSRD for the second year in a row, comparing their FY2024 (published 2025) and FY2025 (published 2026) sustainability statements. We focus on what changes after the “first-time reporting” year, especially with the CSRD not being transposed into Dutch law. Largely we found that much of the early annual reporting practices in 2026 had companies still disclosing with transparency on the business risks, finance risks, and opportunities, to stakeholders and investors.

We looked at the following companies sites to assess their corporate sustainability reporting changes in the midst of the European Sustainability Reporting Standards changes in 2025:

First the first company we assess in corporate sustainability, TomTom’s material topics are the same 6 topics they were subject to by their materiality assessment, but with shifts in specifics and narratives. Largely it reads as the same, but with slightly stronger details, more elaboration on phased in requirements, and a better linkage between ESRS and EU Taxonomy reporting. As for an opening statement, the verbiage is close to identical, only highlighting the legal difference which did not seem to change their way of reporting too dramatically.

FY2024 Opener: “In the 2024 reporting year, the European Sustainability Reporting Standards (ESRS), which were introduced by the EU CSRD, became effective. In anticipation of the transposition of this directive into Dutch law, we have decided to voluntarily use this framework.”

FY2025 Opener: “In the 2024 reporting year, the European Sustainability Reporting Standards (ESRS), introduced by the EU CSRD, became effective. Although this directive has not been transposed into Dutch law, we continue to voluntarily use this framework to guide us in our reporting.”

To highlight some minor differences running through both reports' impact, see examples below…

Structure: In the FY25 ESRS sections, TomTom registered side-by-side “reported vs restated” comparatives more prominently than in the FY24, and the first-time narrative is more about establishing the ESRS baseline. FY25’s more explicit “restated” comparatives around KPIs (e.g., emissions and at least one social metric), with explanations tied to methodology refinements and their interpretation of the boundaries, highlighting potential maturity in ESRS structure and management of KPIs.

SBTi validation: In the FY24 report, TomTom reported that their net-zero commitment/targets were submitted to SBTi and they aimed to submit for validation over 2025. By their FY25 report, they stated that they successfully achieved SBTi validation.

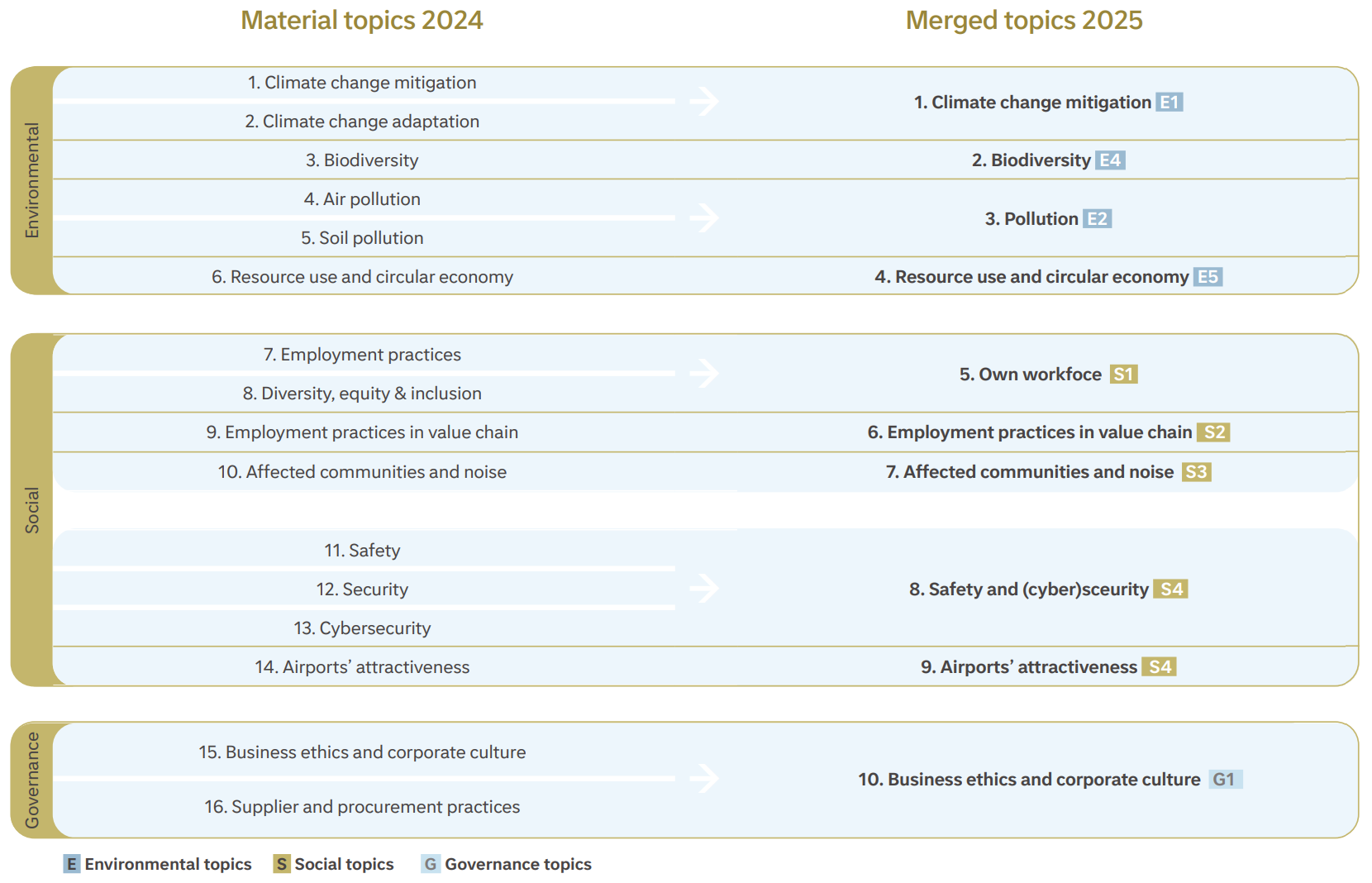

The general vibe shift was behind the intentionality of assessing materiality staying largely the same between both FYs. In fact, in FY24, Schiphol described 2024 as the year the DMA was updated with specific intention to align with the CSRD, including stronger human-rights scoring and expanded related external stakeholder engagement. Still in FY25, Schiphol is now communicating that the DMA only received a light revalidation and update of the 2024 DMA, given no major changes in activity.

Material topics: Mapping for the ESRS became more consistent in FY25. In FY24, terms were mapped out to ensure terminology from the materiality assessment maintained consistency with ESRS labels. See below for how the topics merged:

EU Taxonomy: More adjustments were made here than in the ESRS from what I can tell. No better stated than in the FY25 report, “ The Omnibus package communicated by the European Commission on 27 February changed the EU Taxonomy KPI tables and introduced a materiality threshold of 10%. RSG has elected [to] report the simplified tables under Additional environmental information, and left 1.4% of its CapEx KPI unassessed in line with the Omnibus package.”

Own workforce: Metrics for FTE definition become standardised in FY25. In FY24, FTE is defined differently across group entities (e.g., 36 hours for some locations, 40 for others). In FY25, the workforce metrics table now states simply, “An FTE consists of 36 working hours”, implying a more simplified baseline.

S1-13 performance review: FY25 introduces a methodology change (Amsterdam started tracking via GROW conversations), explicitly states this is a narrower group, and says the FY24 RSG total is therefore restated to 78%. Interesting signal that they may have set a precedent for themselves to maintain comparability of metrics.

From a first look, ESRS KPI signal got stronger and got more comparative, with comparative data from now, going back to 2022 for E1 / climate data. For Water (E3), they were able to report average water usage comparisons vs a 2018 baseline. Generally, FY25 embeds more in-line prior comparatives while explaining progress (e.g., renewable electricity 88% (2024: 84%), Scope 3 decrease 17% (2024: 14%) vs 2022 baseline). FY25 also gets more operational/value-chain specific in the narrative (e.g., packaging supplier roadmaps, contract requirements, Scope 3 split commentary). Other comments:

Explicit signposting: In FY25, the sustainability narrative explicitly points readers to “the disclosures required under CSRD” in the Sustainability Statements (pages 142–262).

That kind of “where the CSRD lives” navigation cue is useful for ESRS-readers doing traceability checks.

Circularity: FY25 discusses circularity with specific metrics and explicit YoY context: reusable packaging 39% (flat vs 2024) and recycled content 48% (2024: 44%), plus references to policy/regulatory developments (e.g., PPWR prep; DRS updates), whereas FY24 had similar data, but less signposted and less comparative data.

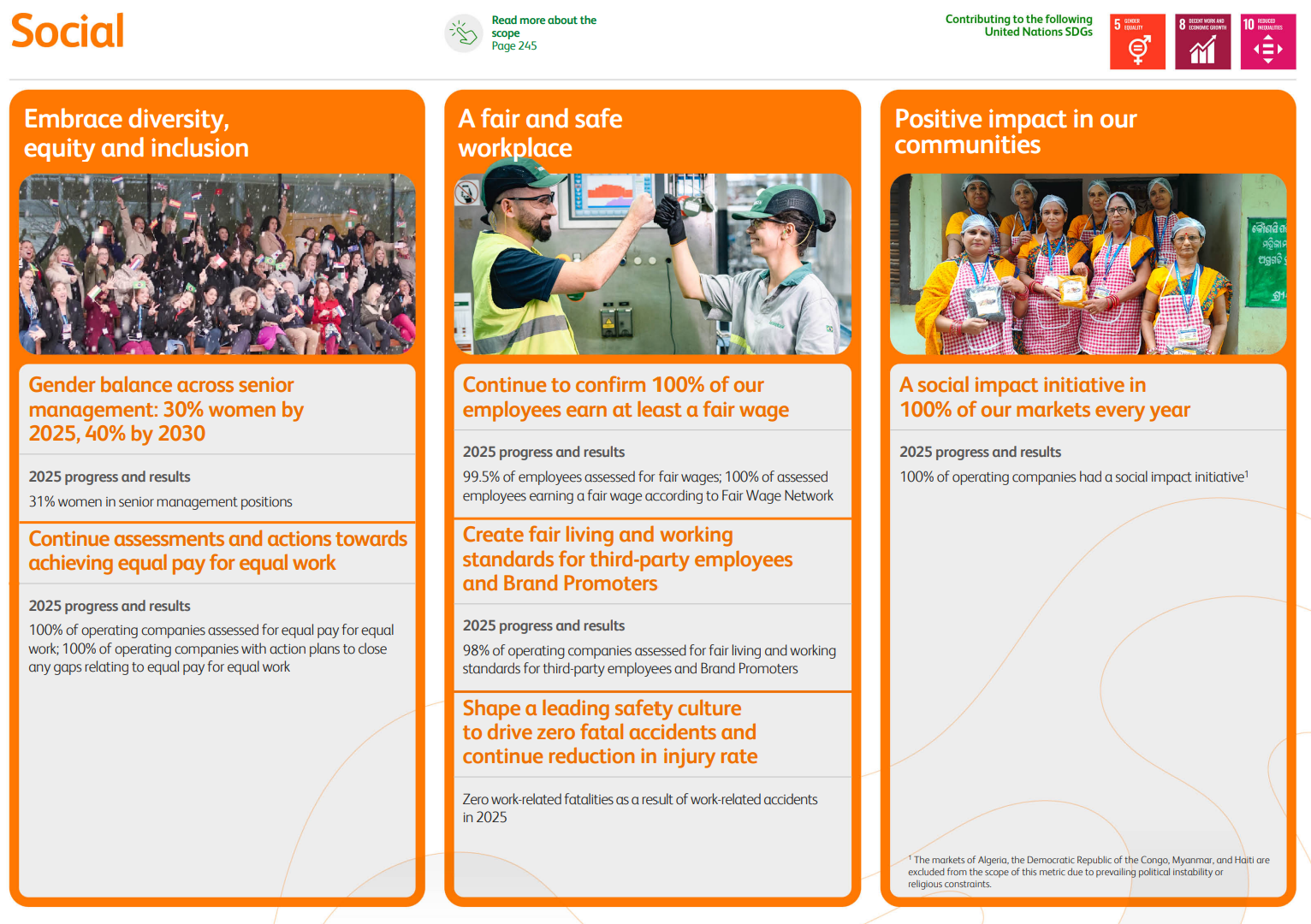

Social Data: Perhaps more my opinion on the reading of the rhetoric, but FY24 reads more like “targets met”; FY25 reads more like “tracked performance” that needs to be measured / managed. FY24 explicitly frames hitting the 30% women in senior management goal early and reiterates the 40% by 2030 ambition; it also quantifies progress on zero-alcohol options reaching 91% of beer & cider volumes in it’s product lineup.

The first difference spotted is in Double Materiality, but largely, much like the the previously mentioned reports, this ESRS disclosure comes across as a more thorough report with updates where relevant.

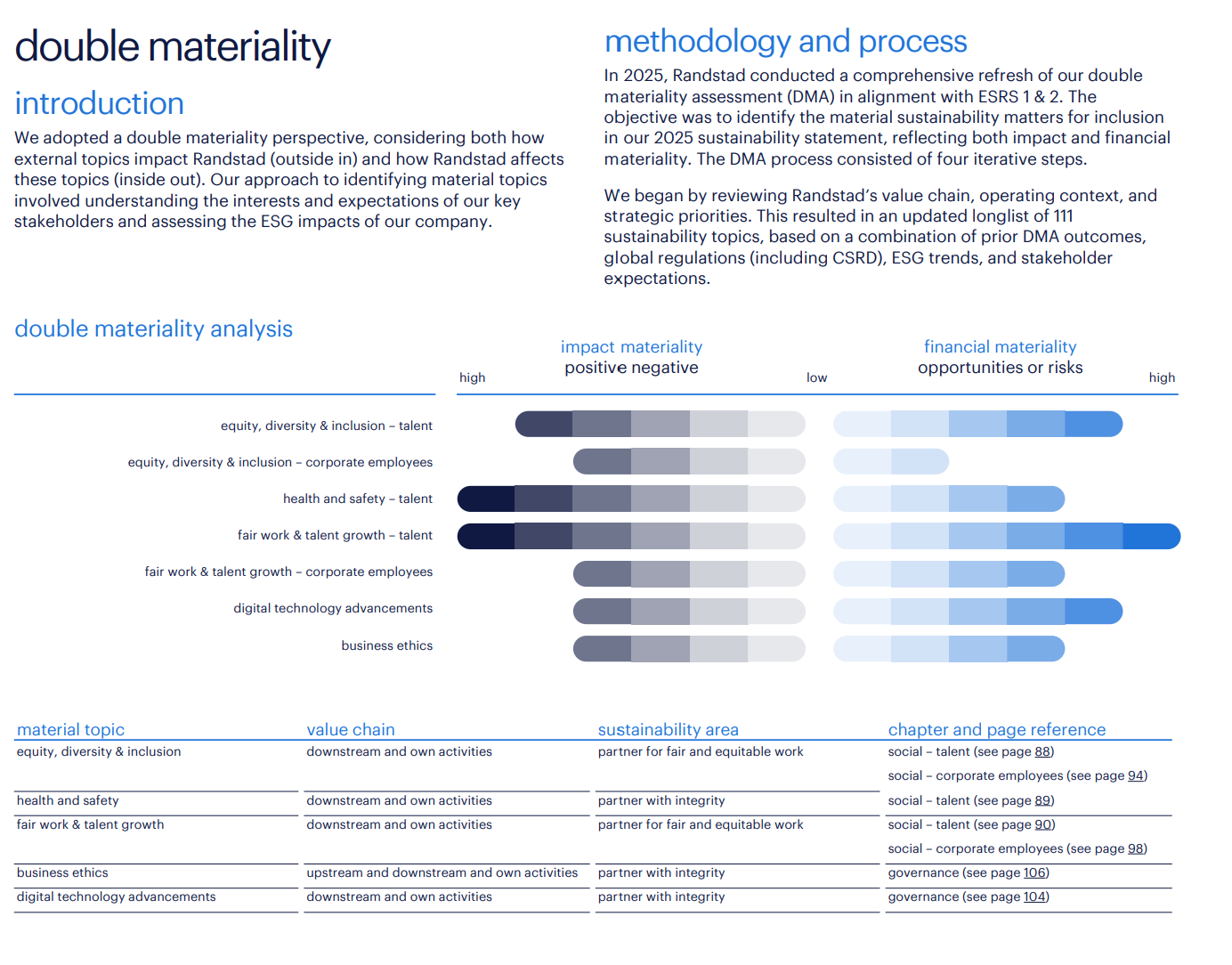

Double Materiality: The FY24 report describes a first-time ESRS-aligned approach, narrowing an initial longlist, with commentary on how topics changed vs the prior 2021 assessment, including more direct signposting of working conditions, refinements of human rights, and more. In FY25 reporting, they register results of their “comprehensive refresh” of the DMA in 2025, shortlisting / narrowing IROs; they also present a cleaner set of material topics (e.g., EDI (talent + corporate), health & safety (talent) and fair work & talent growth (talent + corporate).

Basis for reporting: FY24 frames ESRS reporting as voluntary and proactive, with Dutch CSRD transposition pending. By FY25, the “CSRD not yet transposed” framing is there still, but there is clear comparability between the reporting periods and the verbiage reads like they are evolving in a year-2 “operationalization” stance.

Environmental Materiality: For FY25, I can’t summarise it much better than they first paragraph of the environmental section… “Based on our 2025 double materiality assessment, we concluded that environmental topics are not material for Randstad. While the environment does not represent a material theme for our business, we recognize its wider importance and remain committed to responsible practices.” How would this impact actual reporting acitivities though?

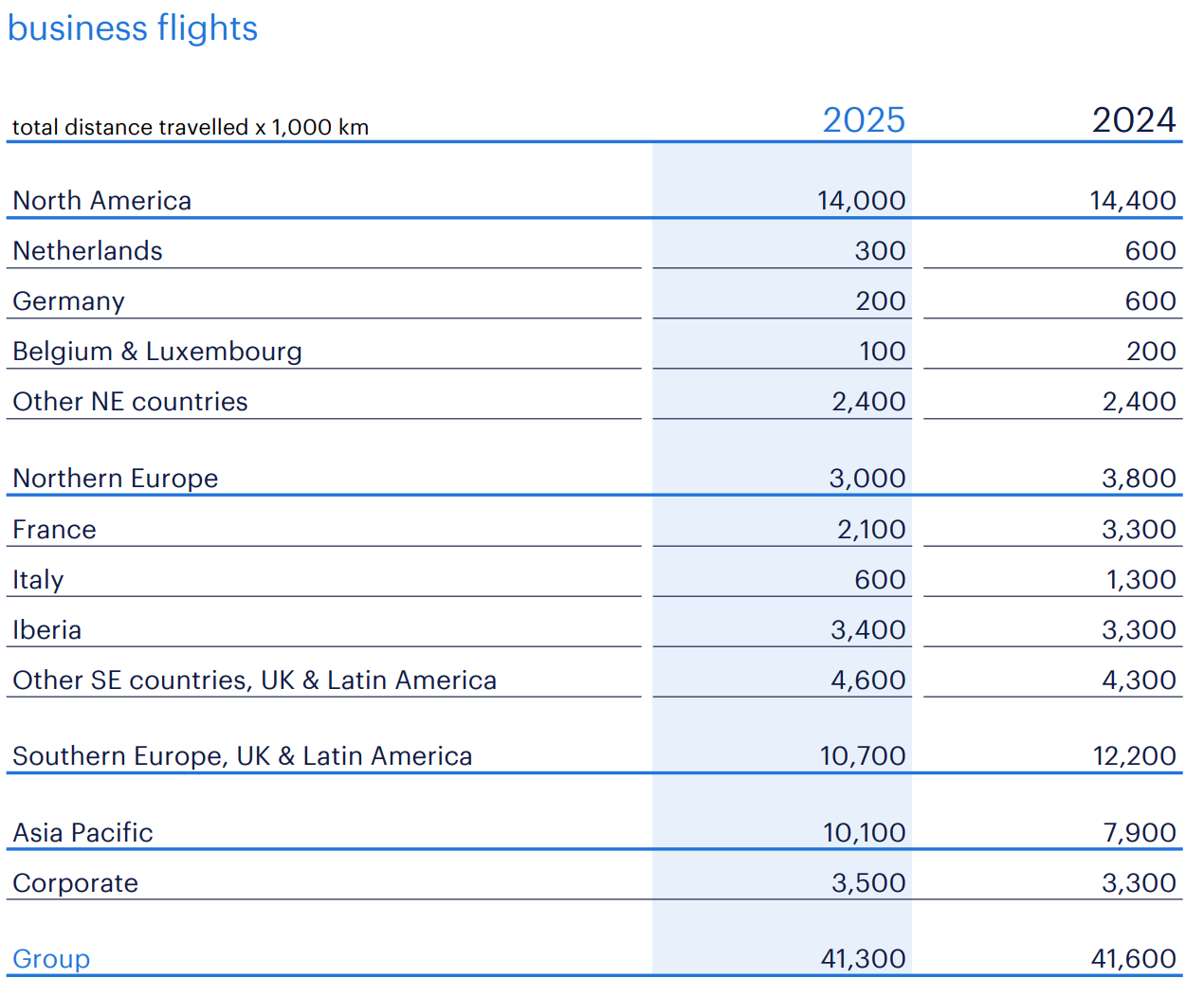

This is a shift between the rhetoric of FY24, highlighting the environmental material opportunity present. Despite this opening line, the report still has an extensive tracking of metrics and topics in the report, despite not deeming it material, meaning the people of Randstad still certainly register the impact / risks of reporting to their stakeholders / community here. This includes quantitative tracking of waste, energy, distance travelled (business flights, company cars, corresponding carbon footprint), water quantities, and a firm stance that they are still committed to SBTi and net zero goals, achieving validation on their targets in 2025. Despite the material topic shift in compliance, it does not seem to change much of the company's transparency and implemented practices to enable them to measure metrics / risks related to the environment. This is a potential win for the planet and impact reporting, as we learn that a company can change its environmental materiality, and still remain committed to the next steps in moving forward.

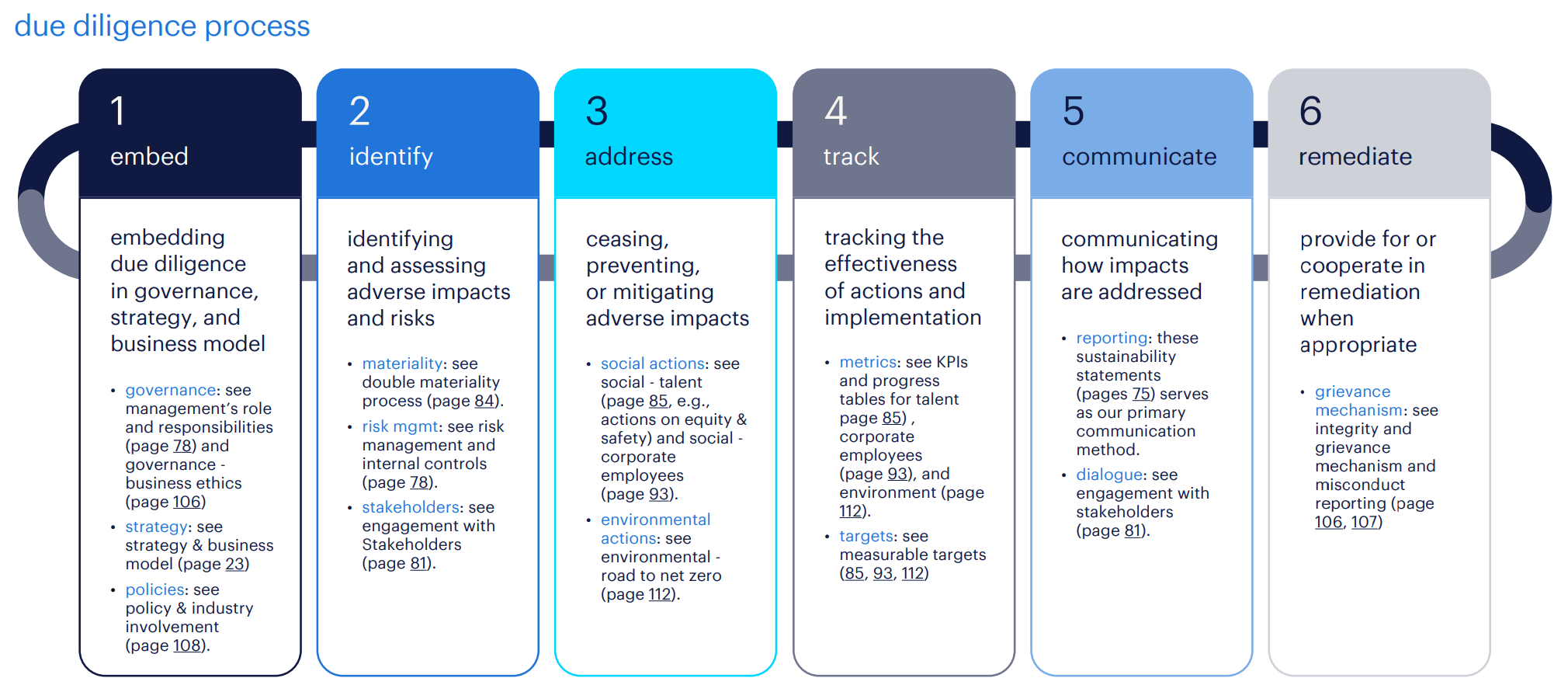

Due diligence: Controls and governance language got a bit sharper, adding more detail around the DMA process (documented scoring rationale, version control, periodic reassessments) and tighter integration language with enterprise risk.

As a business, Nossa Data is committed to understanding what people in the sustainable investor and corporate ESG community would like to see next in analysis on disclosures within corporate sustainability. We read through reports to understand disclosures, rules, accuracy, finance, employee metrics, implementation of standards, so you don't have to. We aim to stay relevant to what each organisation needs to know, so do not hesitate to get in touch if you would like to learn us to pay attention to, support, focus on, or scale insights a particular topic. Similarly, should you wish to collaborate on an article as a corporate ESG professional, please feel free to reach out if this is something we can support you with or provide an impact on.