.png)

Interviews

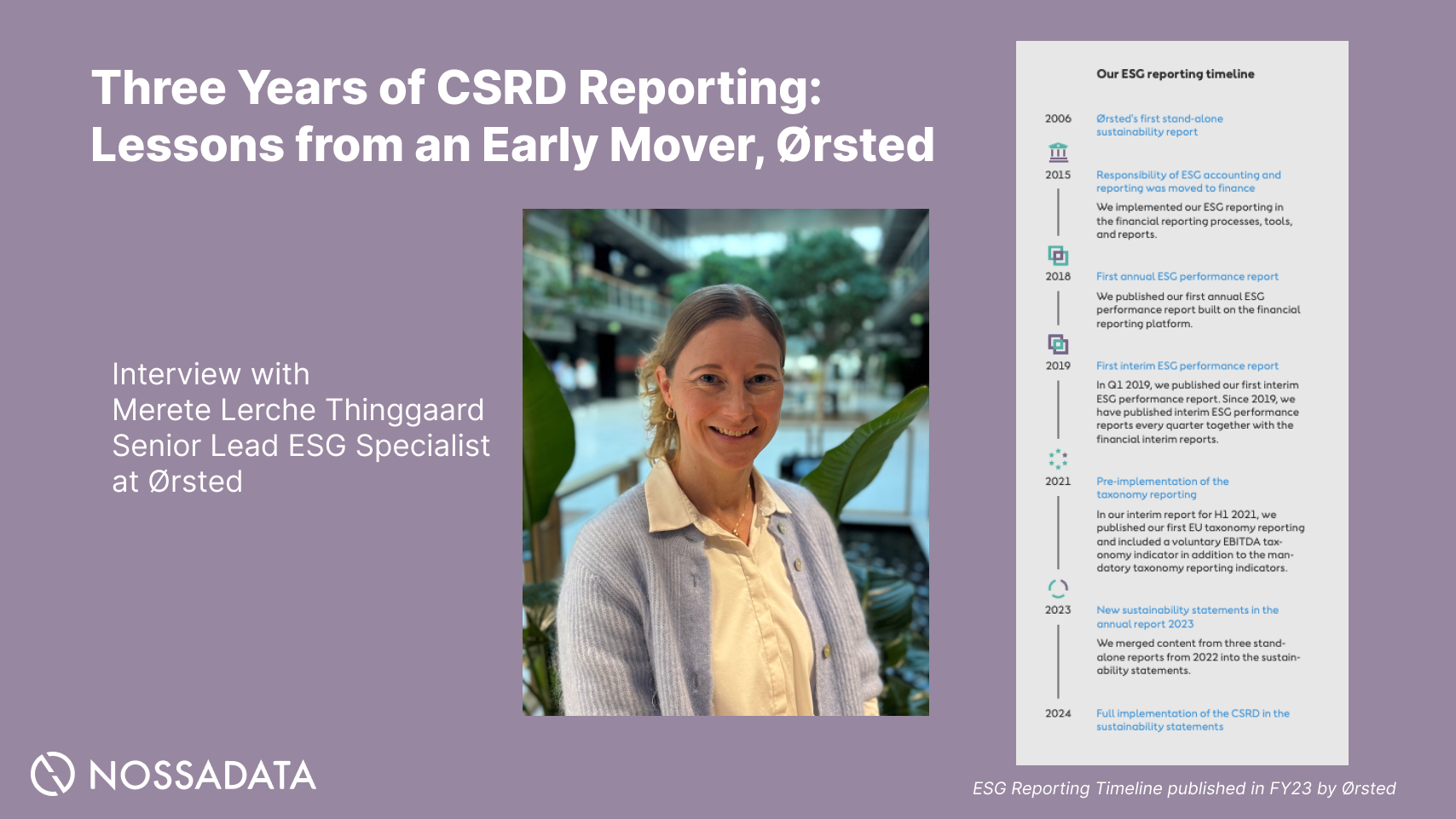

Three Years of CSRD Reporting: Lessons from an Early Mover, Ørsted

An expert interview with Merete Lerche Thinggaard, Senior Lead ESG Specialist at Ørsted, on three CSRD reporting cycles.

The Corporate Sustainability Reporting Directive (CSRD) came into force in 2023 and is a big deal for corporate transparency across the EU. It requires companies in scope to report on their environmental and social impact, with this information to be assured. But because the CSRD is a directive, each EU member state has to transpose it into national law—a process that had to be done by 6 July 2024. For related initiatives, check out the Corporate Sustainability Due Diligence Directive (CSDDD) explainer by CDP.

The European Parliament was key in passing the CSRD. Despite the deadline, 17 countries didn’t fully transpose the CSRD on time and the European Commission has started infringement procedures. This means while the CSRD sets a baseline, its real world application varies from country to country—and in some cases is still in flux.

Importantly the CSRD is not a maximum harmonisation directive, so countries can go beyond the requirements when transposing it—this is called “goldplating.” These national divergences can create complexity for companies operating across multiple jurisdictions within different EU member states.

Here’s a look at three countries to see how the CSRD is being transposed in practice:

The Corporate Sustainability Reporting Directive (CSRD) is a big deal in the world of sustainability reporting, to increase transparency and accountability of companies operating in the European Union. By requiring large and listed companies to disclose comprehensive information on their environmental, social and governance (ESG) performance, the CSRD will promote sustainable practices and investments. This directive is part of a broader effort to put sustainability at the heart of business strategy, to drive growth, protect reputation, and unlock profit and purpose. As companies navigate the complexities of CSRD compliance, they also need to consider the broader implications of sustainability reporting on their financial performance, competitive advantage and relationships with stakeholders including investors, consumers and other stakeholders.The CSRD builds on the foundations of the Non-Financial Reporting Directive (NFRD) and expands the scope and depth of sustainability reporting requirements. With the European Commission’s proposal for significant changes as part of an Omnibus package, the regulatory landscape for corporate sustainability reporting is changing. The CSRD’s introduction of European Sustainability Reporting Standards (ESRS) provides a common framework for companies to report on their sustainability performance, so the information disclosed is comparable and credible. This is big for companies worldwide as it sets a new benchmark for transparency and accountability in sustainability reporting, not just for EU companies but also for non-EU companies operating in the EU market.

The CSRD applies to almost 50,000 EU companies, a big increase from the NFRD. To fall under the CSRD’s scope, companies must meet specific criteria, including a total balance sheet value, net turnover or number of employees. SMEs will also be subject to the CSRD but with a phased implementation. Non-EU companies with operations in the EU will have to comply with the CSRD if they meet the thresholds, so there is a level playing field for sustainability reporting requirements. The directive applies to listed companies and non-listed companies that meet the criteria, so it covers a wide range of companies operating in the EU.

The CSRD requires companies to disclose a lot of sustainability related information, including quantitative measures and qualitative narratives. The European Sustainability Reporting Standards (ESRS) provide the framework for this disclosure, covering topics such as environmental impact, social responsibility and governance practices. Companies must do a double materiality assessment to identify the most significant sustainability issues for their business and report on those. The CSRD also introduces the concept of “limited assurance” for sustainability information, to increase the credibility and reliability of the data. Companies will also have to publish their sustainability reports in a standard digital format, so the information is accessible and comparable.

Implementing the CSRD will be a challenge for companies, gathering and reporting complex sustainability data, ensuring compliance with ESRS and managing the costs and resources. But the CSRD also presents opportunities for companies to deepen their understanding of sustainability risks and opportunities, unlock value through integrated reporting and enhance their reputation and competitiveness. By embracing the CSRD’s requirements companies can show their commitment to transparency, accountability and sustainability and contribute to a more environmentally friendly and socially responsible business environment. As the EU evolves its sustainability reporting landscape companies must stay vigilant and proactive in their compliance efforts and use the CSRD as a catalyst for long term growth, innovation and success.

Managing sustainability information is key to CSRD compliance. This delay creates an unlevel playing field between companies across the EU.

Belgium has kept its approach very close to the directive’s core framework. The information disclosed must be relevant and useful for stakeholders, in line with relevant legislation and standards.

Ireland’s early transposition and selective goldplating is a cautious but forward looking approach to CSRD. Ireland’s transposition requires companies to include sustainability reporting in their annual reports and hence full transparency.

And Ireland’s approach adds to the credibility of the information reported by requiring additional assurance.