Interviews

Three Years of CSRD Reporting: Lessons from an Early Mover, Ørsted

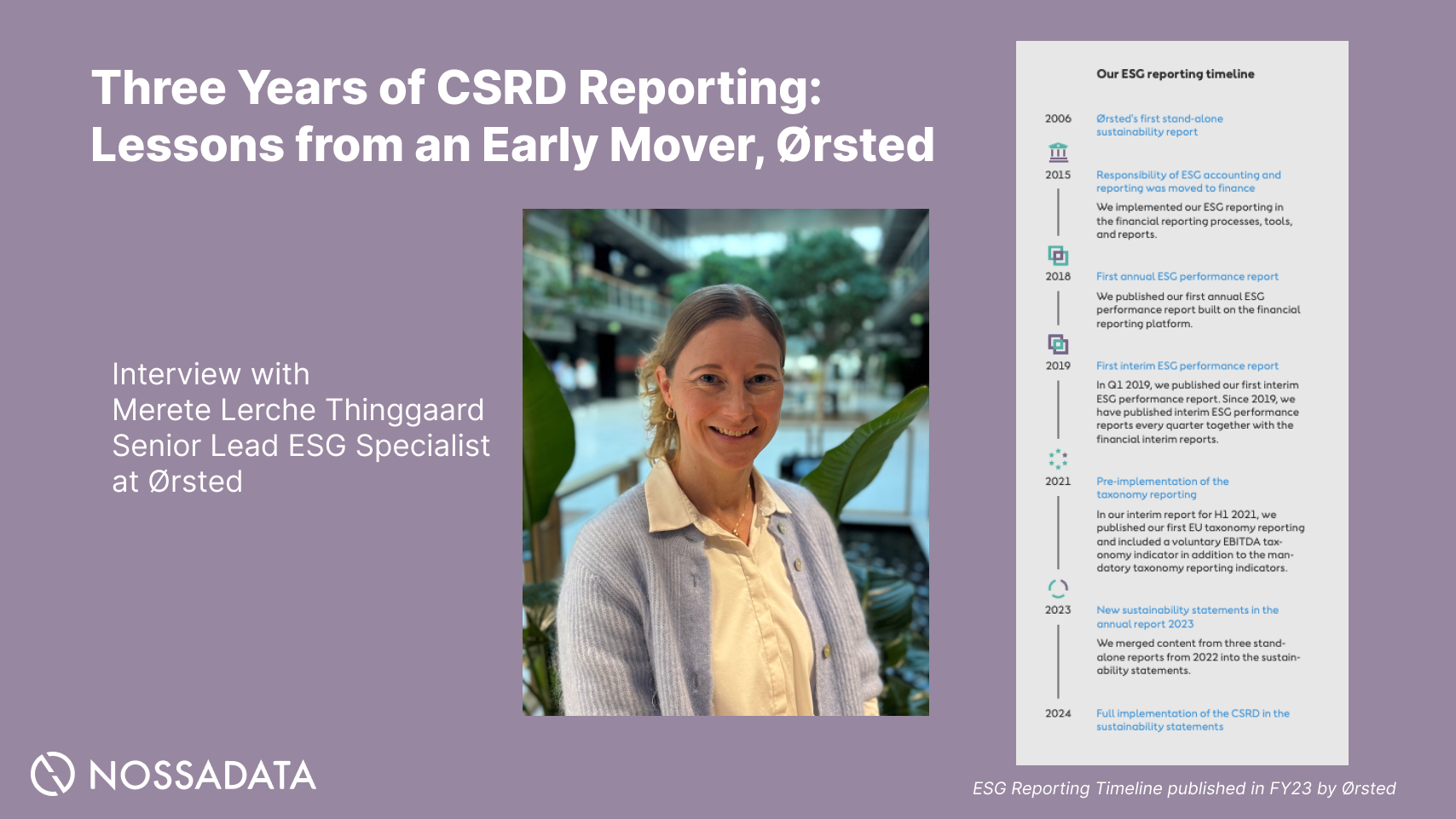

An expert interview with Merete Lerche Thinggaard, Senior Lead ESG Specialist at Ørsted, on three CSRD reporting cycles.

The Corporate Sustainability Reporting Directive (CSRD) was adopted by the EU Commission in July 2023, replacing the Non-Financial Reporting Directive (NFRD). The CSRD increases the scope of the NFRD and introduces mandatory third-party assurance for sustainability reporting. It aims to standardise sustainability metrics, mandate corporate sustainability disclosures and increase transparency.

Companies that fall under scope of the CSRD will have to report to the European Sustainability Reporting Standards (ESRS). The standards were developed by the European Financial Reporting Advisory Group (EFRAG), an independent body tasked with advising the European Commission. These standards are built around EU policies, while taking into account and contributing to international standardisation initiatives.

1. Large EU companies with:

2. Parent companies incorporated in an EU member state, where the group of companies collectively meet the large company criteria

3. Non-EU incorporated companies:

4. Captive insurance and reinsurance undertakings

5. Small and non complex institutions, provided they also qualify as large companies or SMEs

The CSRD is the first mandatory ESG standard that requires assurance on sustainability information. The incoming regulations will guarantee that investors and other interested parties can readily access the data necessary for evaluating the influence of companies on both society and the environment. Additionally, investors will have the means to gauge financial risks and opportunities linked to climate change and other sustainability matters.

Prior to responding to the ESRS, companies are required to complete a Double Materiality Assessment. This means that a reporting entity must consider both environmental impact materiality and financial materiality when identifying the material topics to be disclosed under the ESRS. The CSRD report must be included in a company’s management report rather than in a separate sustainability report. The first companies will have to apply the new rules for the first time in the 2024 financial year, for reports published in 2025.

Nossa Data can assist companies to prepare a gap analysis for the upcoming regulation to ensure all material topics relating to the entity are being disclosed. Clients can disclose to the ESRS using the Nossa Data platform. In addition, clients have in platform access to a simplified guidance on overarching, sub and application requirements on a question by question basis.

Start your CSRD Journey with Nossa Data

Sources: