Interviews

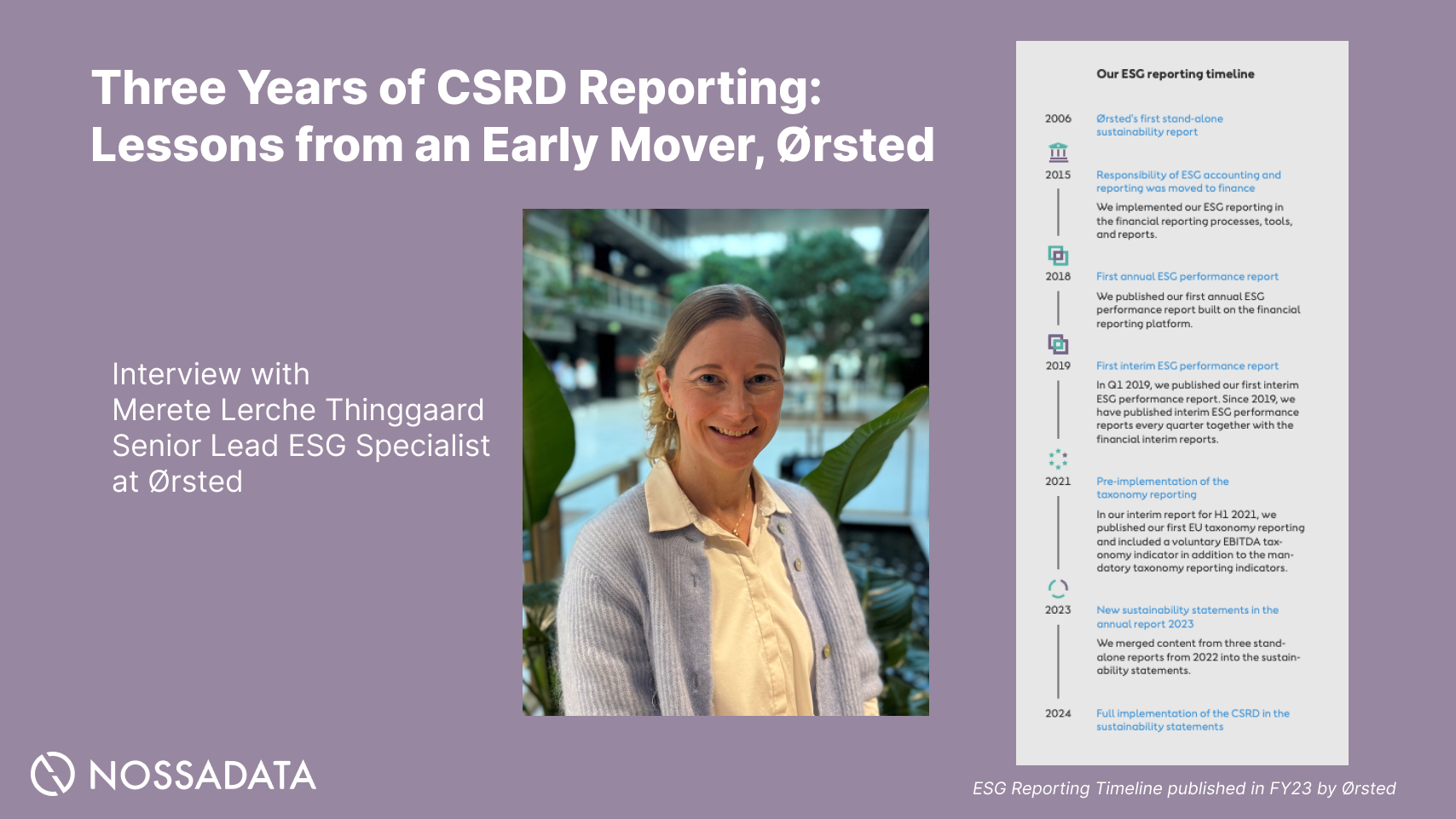

Three Years of CSRD Reporting: Lessons from an Early Mover, Ørsted

An expert interview with Merete Lerche Thinggaard, Senior Lead ESG Specialist at Ørsted, on three CSRD reporting cycles.

.png)

At Nossa Data, we’re proud to share that our ESG reporting platform is both recognised and trusted by organisations worldwide, including companies like PensionBee, Vodafone, and others. ESG data is essential for delivering accurate and thorough sustainability reports. Strong internal controls are key to reducing risks and boosting transparency, which is why Nossa Data offers tools that help organisations strengthen their ESG practices and streamline reporting for frameworks such as CDP, IFRS, EcoVadis.

As we move deeper into 2025, the ESG regulatory landscape continues to evolve rapidly, presenting both opportunities and challenges for businesses and investors alike. Sustainable Fitch’s latest ESG Regulation and Reporting Standards Tracker, updated at the end of April, offers a valuable snapshot of where global ESG standards are headed. The quarterly update highlights regulatory changes, new proposals, and key milestones set to unfold over the coming year.

The CSRD officially came into force on January 5, 2023, following its final approval by the European Council in late November 2022. The annual report has become a crucial element in sustainability reporting, integrating sustainability-related risks alongside traditional business risks. This trend underscores the growing importance of sustainability in broader discussions about risk and value creation, making it highly relevant to investors and decision-makers.

Here are the most noteworthy ESG regulatory trends and timelines to keep on your radar.

1. Europe Tightens ESG Frameworks

The European Union remains at the forefront of ESG regulation. Several important updates are coming out of Brussels:

2. The UK Moves Toward Sustainable Disclosure Standards

Across the Channel, the UK is preparing to release its Sustainable Disclosure Standards (SDS) for consultation in Q2 2025. Modeled in part on international initiatives like the ISSB standards, the SDS is expected to provide clarity and comparability in corporate sustainability reporting, helping investors better assess ESG risks and opportunities.

3. Taxonomies on the Rise: Canada, Australia, Brazil

Several countries are making strides in developing sustainable finance taxonomies:

These developments mark a clear global shift toward greater ESG harmonization, although local variations in priorities and definitions will persist.

4. UAE Sets a Precedent for Emissions Disclosure

In a landmark move, the United Arab Emirates will mandate GHG emissions disclosures for applicable companies starting May 30, 2025. This requirement signals a growing trend in the Middle East toward formalizing ESG expectations, particularly around climate-related risks and transparency.

Final Thoughts

The 2025 ESG regulatory agenda is shaping up to be one of the most dynamic in recent years. With multiple jurisdictions rolling out or refining sustainability frameworks, companies must remain agile and proactive in their ESG strategies.

For stakeholders, staying informed isn’t just about compliance, it’s about leveraging these changes to drive long-term value and resilience. As always, we’ll continue to monitor and share updates on these emerging trends, helping you navigate the evolving ESG ecosystem with clarity and confidence.

The EU has introduced the Corporate Sustainability Reporting Directive (CSRD) to enhance transparency and accountability among companies regarding their environmental, social, and governance (ESG) practices. The CSRD applies to companies based outside the EU if they have a presence in the EU. This directive is part of a broader effort to promote sustainable finance and encourage companies to adopt more responsible business approaches. The CSRD builds upon the Non-Financial Reporting Directive (NFRD) and introduces more detailed reporting requirements for large companies. By mandating the disclosure of sustainability information, the EU directive aims to support investors, consumers, and other stakeholders in making informed decisions.

The CSRD is a significant development in the field of sustainability reporting, requiring companies to provide detailed information about their sustainability performance, risks, and opportunities. The level of financial penalties for non-compliance can be tied to a company's total annual turnover. The directive applies to all large companies, including those with a net turnover of €40 million, which are required to comply with the CSRD. Companies subject to the CSRD must publish regular reports on their ESG activities, which will be made available to the public. The CSRD requires companies to conduct a double materiality assessment, considering both the impact of their activities on the environment and society (impact materiality) and the financial materiality of sustainability matters. This assessment will help companies identify the most relevant sustainability topics to report on.

The CSRD casts a wide net, impacting nearly 50,000 EU companies, including large companies, small and medium enterprises (SMEs), and even micro enterprises. This directive mandates that companies disclose comprehensive sustainability information within their management reports, integrating both financial and sustainability data. The scope of the CSRD is intricately linked to the double materiality assessment, which evaluates both the impact materiality (the effect of the company’s activities on the environment and society) and financial materiality (the financial implications of sustainability matters). Companies subject to the CSRD must report on their sustainability performance, covering a range of environmental and social issues, and disclose detailed information on their policies, initiatives, and targets. By promoting corporate sustainability and simplifying sustainability regulation, the CSRD aims to provide a standardized framework for sustainability reporting, ensuring that all stakeholders, including investors and consumers, can make informed decisions based on reliable and comparable data.

Double materiality assessment is a key element of the CSRD, enabling companies to determine the reporting scope and identify the most critical sustainability topics. The assessment involves evaluating the impact of a company’s activities on the environment and society, as well as the financial implications of sustainability matters. In this context, the significance of climate change is paramount, as businesses must disclose both the risks they face due to climate change and the impacts they cause to it. By considering both impact and financial materiality, companies can provide a more comprehensive picture of their sustainability performance. The CSRD disclosure requirements include reporting on policies, initiatives, and targets related to sustainability, as well as progress towards these targets. Companies must also disclose information on their entire value chain, including social and environmental issues.

The European Commission has provided guidance on the implementation of the CSRD, emphasizing the importance of transparency and consistency in sustainability reporting. The European Parliament has played a crucial role in the timeline and implementation of the CSRD, including confirming delays and passing the CSRD text through decisive votes. The Commission has also proposed significant changes to the reporting requirements, including the introduction of European Union (EU) sustainability reporting standards. These standards will provide a common framework for companies to report on their sustainability performance, ensuring comparability and consistency across the EU. The Commission’s guidance also highlights the need for companies to embed sustainability knowledge in their organization and to consider the interests of all stakeholders, including affected communities. The CSRD is being incorporated into national law across the EU, with each member state enforcing the new regulations, which may lead to varied compliance requirements and stricter standards in some countries.

Under the CSRD, companies are required to obtain limited assurance from an independent auditor, with the possibility of transitioning to reasonable assurance over time. This assurance process is crucial for evaluating the accuracy and reliability of the sustainability data disclosed by companies. Auditors will assess the company’s reporting process, scrutinizing the collection and analysis of sustainability data, and provide an opinion on the fairness and accuracy of the reported information. Additionally, the CSRD mandates that companies disclose information in alignment with the Task Force on Climate-related Financial Disclosures (TCFD) requirements and the EU Taxonomy. The assurance and audit process will play a pivotal role in ensuring the credibility and transparency of sustainability reporting, thereby enhancing stakeholder trust and confidence in the disclosed information.

The CSRD officially entered into force on January 5, 2023, setting a clear timeline for companies to follow. By January 1, 2025, companies must submit their first CSRD-compliant report, covering the 2024 financial year. The implementation timeline is phased, starting with large companies, followed by small and medium enterprises (SMEs), and finally micro enterprises. This phased approach allows companies of different sizes to gradually adapt to the new requirements. The European Commission has proposed significant changes to the Non-Financial Reporting Directive (NFRD), which will be replaced by the CSRD. Companies must start preparing for the CSRD by gathering sustainability data, developing a robust reporting process, and ensuring compliance with the EU Sustainability Reporting Standards. This preparation is essential for meeting the new reporting obligations and avoiding potential enforcement actions.

The CSRD presents a dual-edged sword of challenges and opportunities for companies. On the challenge side, companies must navigate more detailed reporting requirements, conduct a thorough double materiality assessment, and secure limited assurance from an independent auditor. These requirements demand significant effort and resources. However, the CSRD also opens up numerous opportunities. Companies can leverage the directive to enhance their sustainability performance, increase transparency, and attract sustainable investments. By identifying and managing sustainability risks, companies can improve their reputation and brand value. Moreover, the CSRD facilitates informed decisions by investors, consumers, and other stakeholders, promoting a more sustainable and responsible business model. Embracing the CSRD can ultimately lead to long-term value creation and resilience in an increasingly sustainability-focused market.

In 2025, companies will be required to submit their first CSRD-compliant reports, covering the 2024 financial year. This will mark a significant milestone in the implementation of the CSRD, as companies will need to demonstrate their ability to provide detailed and accurate sustainability information. The complexities of CSRD reporting and the importance of integrating sustainability into business strategies cannot be overstated. The European Commission is expected to continue providing guidance and support to companies, and the EU sustainability reporting standards will be finalized. Additionally, the Commission will monitor the progress of companies in implementing the CSRD and will take enforcement action against those that fail to comply. As the CSRD continues to evolve, companies must remain vigilant and adapt to the changing regulatory landscape, ensuring that they are well-prepared to meet the challenges of the new CSRD requirements and the opportunities presented by this directive.