Interviews

Three Years of CSRD Reporting: Lessons from an Early Mover, Ørsted

An expert interview with Merete Lerche Thinggaard, Senior Lead ESG Specialist at Ørsted, on three CSRD reporting cycles.

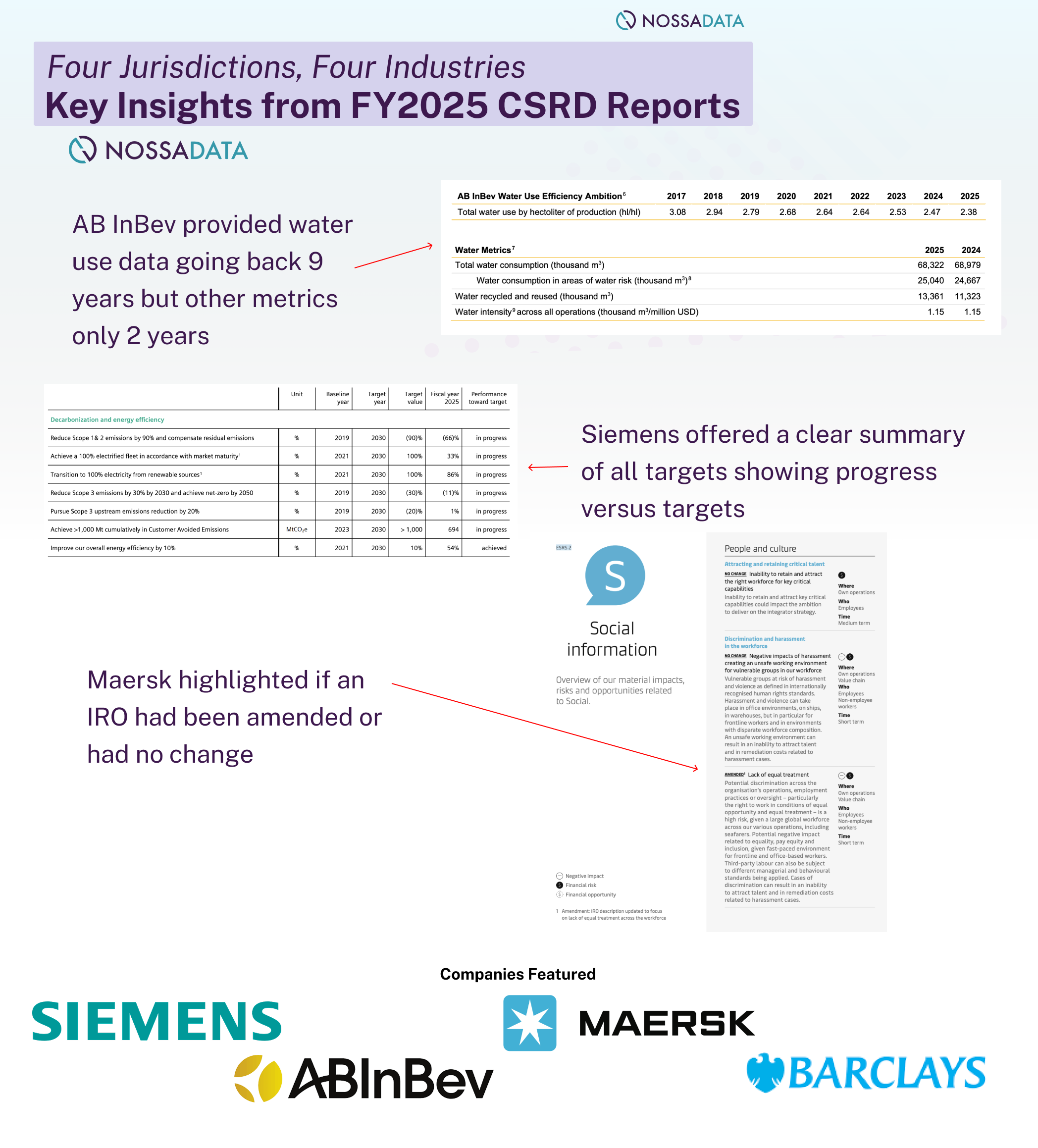

For this week’s article, I reviewed FY2025 CSRD reports from four companies operating across different jurisdictions and industries: AB InBev, Siemens, Barclays Bank Plc, and Maersk. Three of these companies are publishing their second CSRD-aligned reports, while Siemens’ report represents its first CSRD-aligned disclosure due to its September financial year-end.

Several observations stood out.

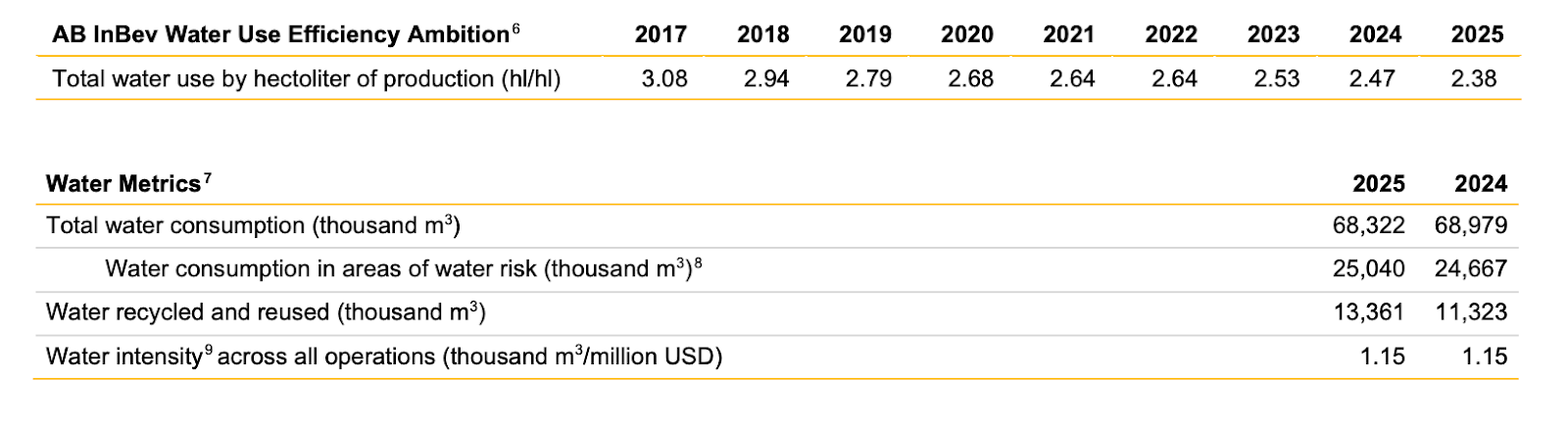

Different approaches to historical data disclosure. Even within the same report, companies vary significantly in how they present historical data. For most metrics, disclosures are limited to FY2024 and FY2025—reflecting the CSRD reporting timeline. However, in certain areas, companies provide much longer trend data. For example, AB InBev includes nine years of data on water use, while presenting only two years of data for workforce-related metrics.

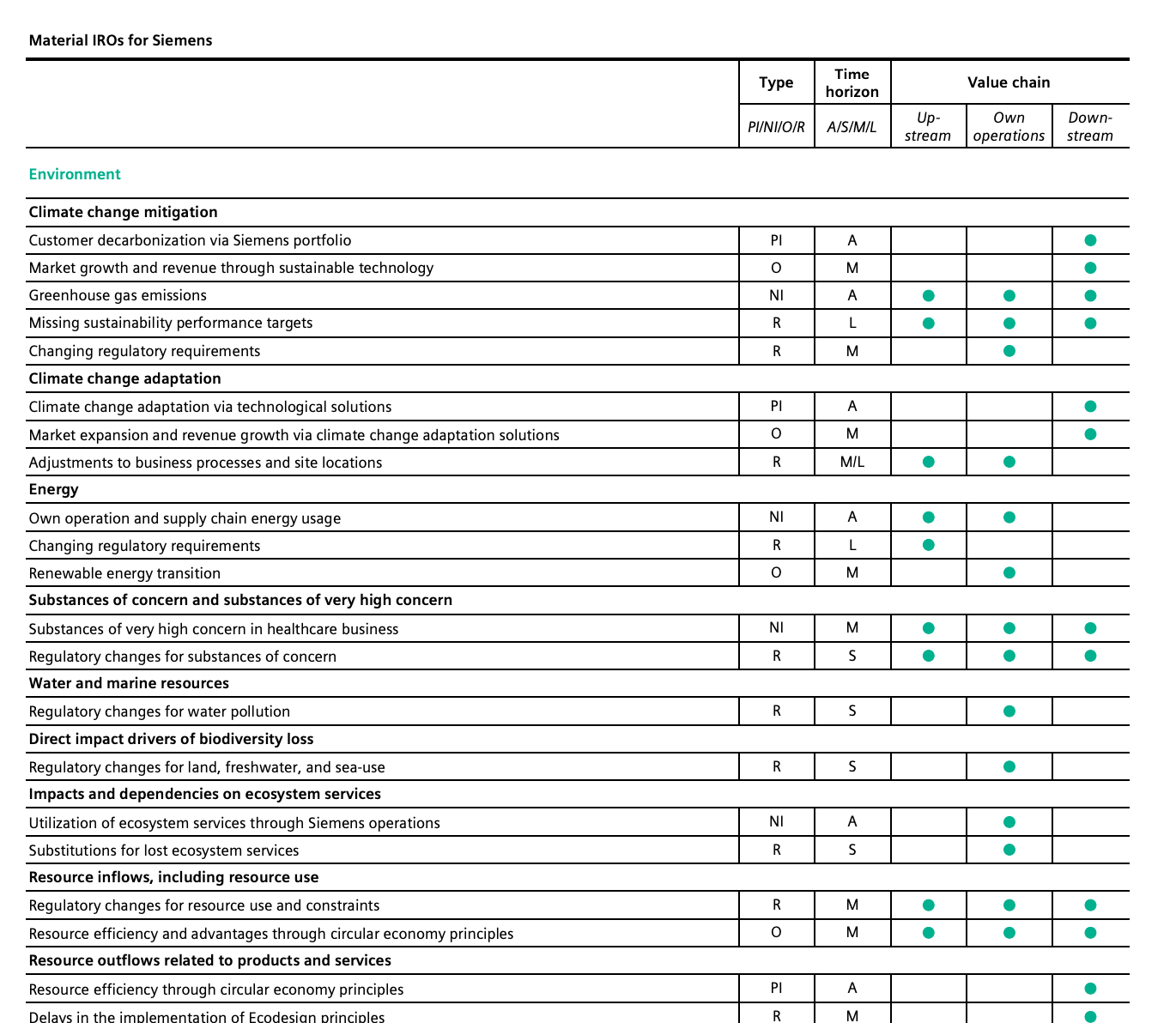

Clear mapping of material topics to IROs. Many—but not all—companies begin each material topic section with a table outlining the relevant Impacts, Risks, and Opportunities (IROs). This practice greatly enhances usability, allowing readers to quickly understand how identified IROs connect to each material topic.

Use of EFRAG datapoint IDs in metric disclosures. Similar to trends observed in earlier analyses, Maersk continues to reference EFRAG datapoint IDs alongside its metric disclosures. It will be interesting to see how companies adapt, if following the Omnibus developments, EFRAG releases an updated datapoint file—particularly how first-wave reporters respond to potential changes of data point IDs.

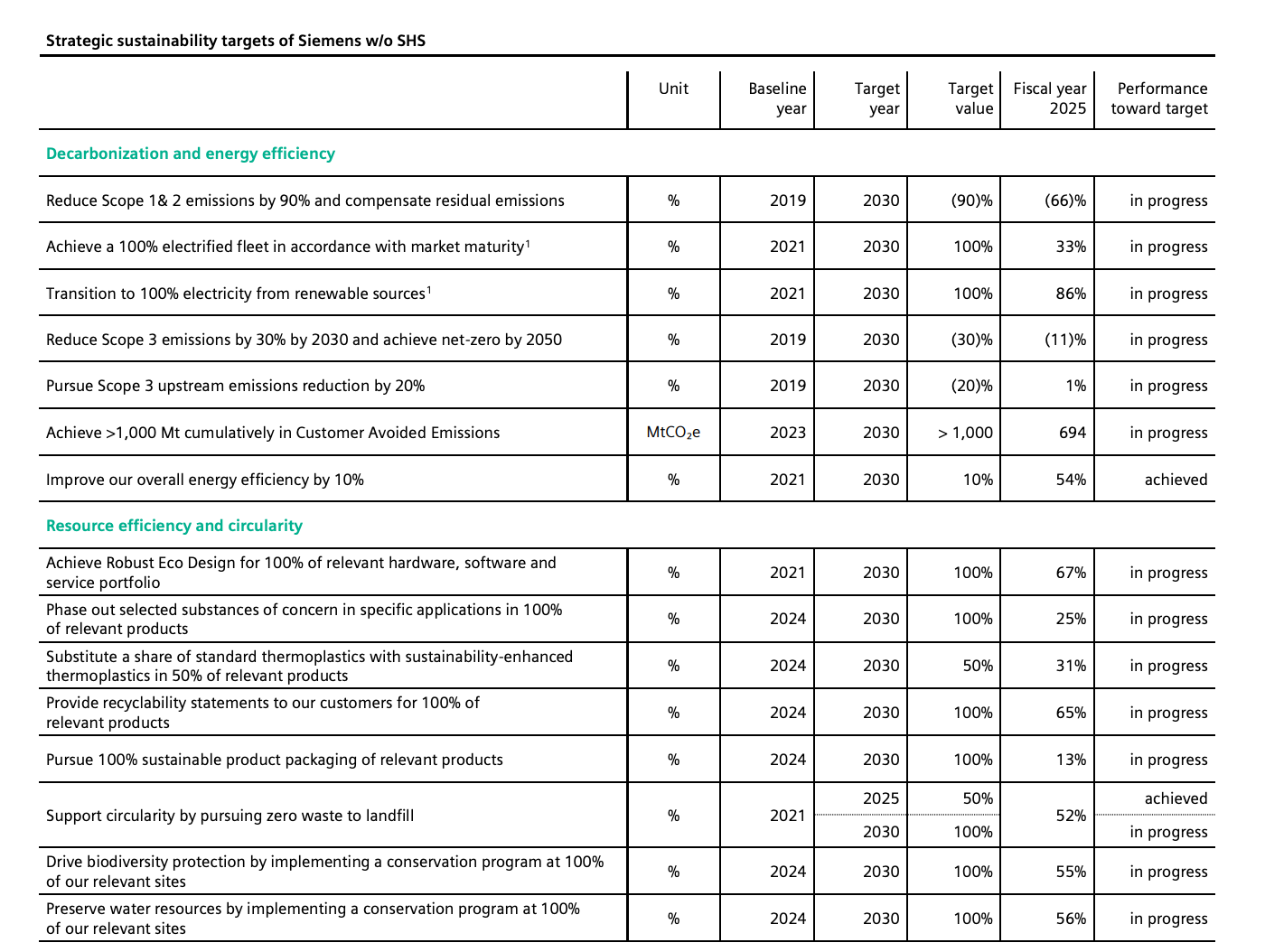

Concise and transparent target reporting. Siemens stands out for publishing a clear summary table of its sustainability targets, including the target year and performance against each goal. This format makes it easy for readers to assess progress at a glance and represents a strong example of user-friendly disclosure.

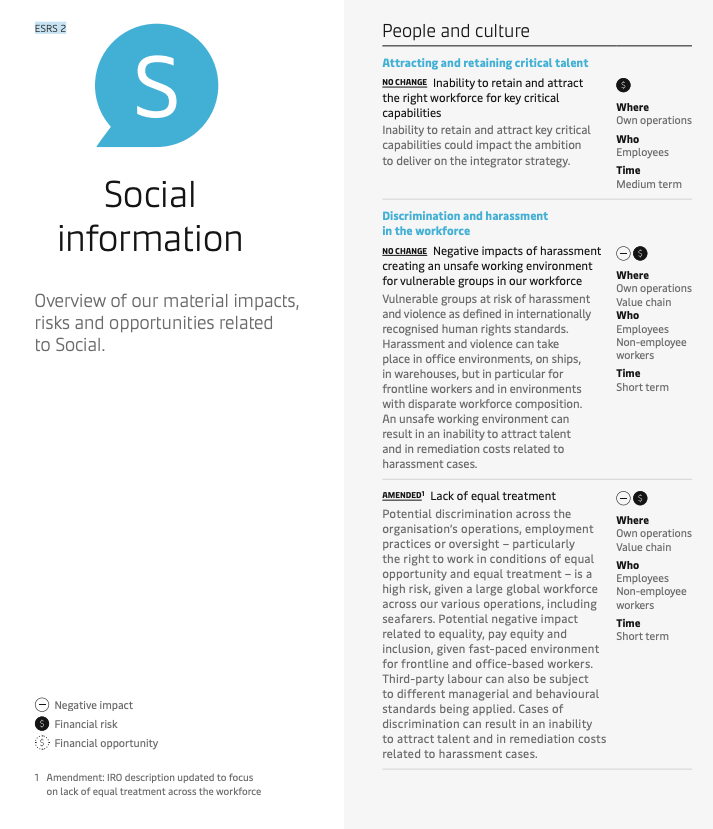

Highlighting if an IRO / Material Topic was amended: Maersk had a very clear communication in their FY2025 report about when IROs had been amended from the previous year. This helpful noted "No Change" or "Amended" next to each listed IRO so the reader was left in no doubt about any changes. They even specified an amended reason.

In the remainder of this article, I will explore these observations in more detail through specific disclosure examples from each of the four reports. By comparing how AB InBev, Siemens, Barclays Bank Plc, and Maersk approach key CSRD requirements—I aim to highlight practical reporting choices that may shape emerging best practices. These examples provide useful insight into how early wave one reporters are interpreting the ESRS framework in practice, and where we may begin to see greater consistency—or continued divergence—in future reporting cycles.

Would you like Nossa Data, an ESG software company and advisory firm, to analyse your CSRD Report? We are completing a series of analysis over the coming weeks. Get in touch at solutions@nossadata.com and we can look at your latest publication.

AbInBev found 11 material topics. See this analysis here.

One difference we noticed in AB InBev versus other CSRD reports assessed is for one of their material topics, Water - for some metrics they provide data prior to CSRD. See the below screenshot where “Total water use by hectoliter of production (hl/hl)” but other water metrics begin when CSRD begins.

A key difference in their disclosure versus some others we reviewed from Denmark (article here) is their report overall seemed to follow less of the CSRD structure than we have seen from other companies (in terms of formatting choices). For example, when discussing “Climate” data is presented in a narrative approach with data tables. Meanwhile other reports we have assessed would organise this by discussing their IROs, Policies, Actions and Metrics.

Due to Siemen’s September 30th year end, this was their first aligned CSRD Report. A number of best practice techniques were shown.

For one, they offered a summary table of all of their targets with Base year, Target Year, Target Value and Performance versus target. See the screenshot below.

They also offer an extensive list of all of their material IROs.

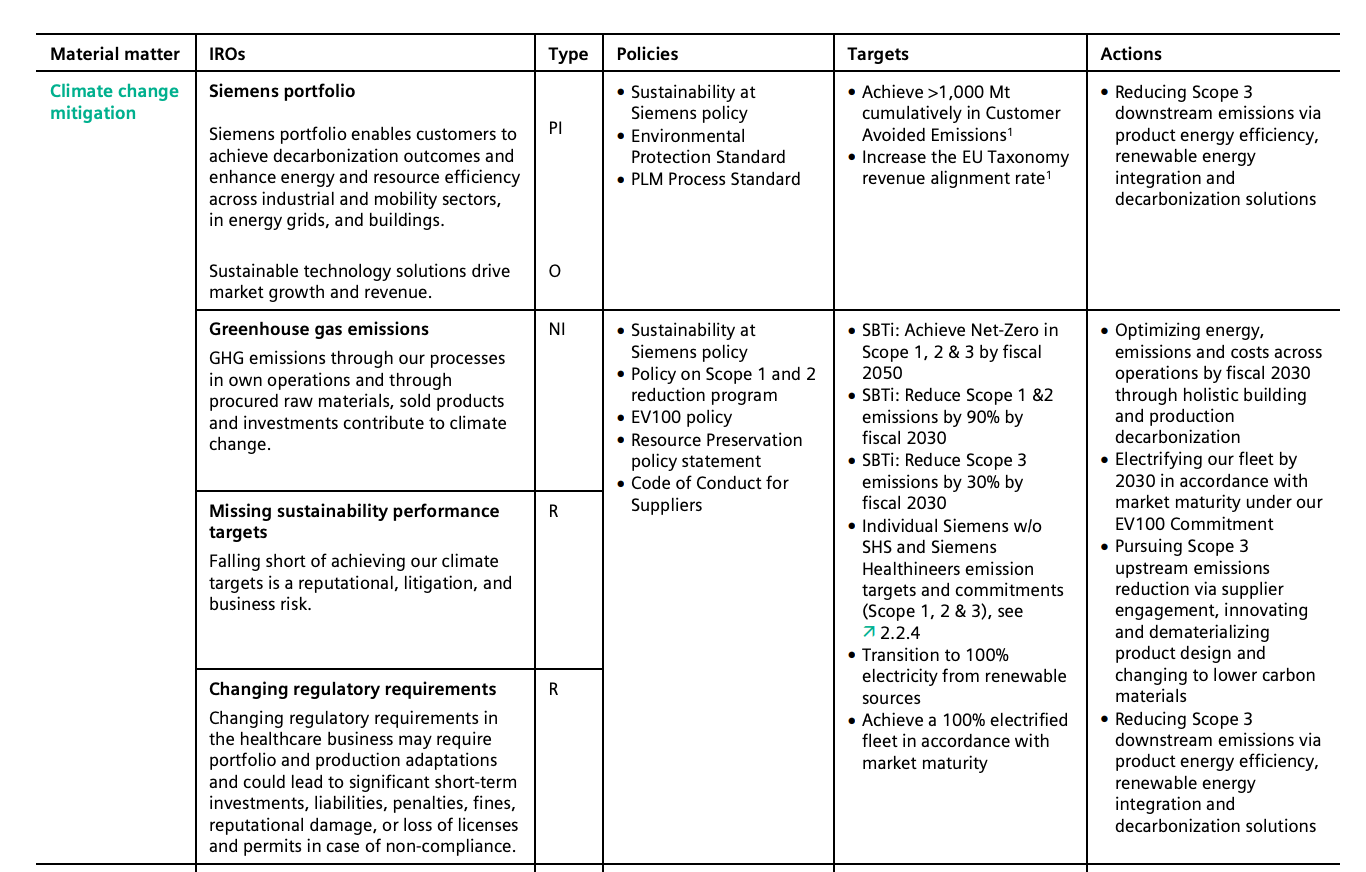

Later, when Siemens does their topic level disclosure, IROs are summarised at the top again but this time providing the contacts on the related Policies, Targets and Actions. See below an example for Climate Change Mitigation.

Metrics Data

Similar to other year one CSRD reports, their metrics data begins in their first CSRD reporting cycle. They do not offer historic data points for their quantitative figures. See below their employee data tables.

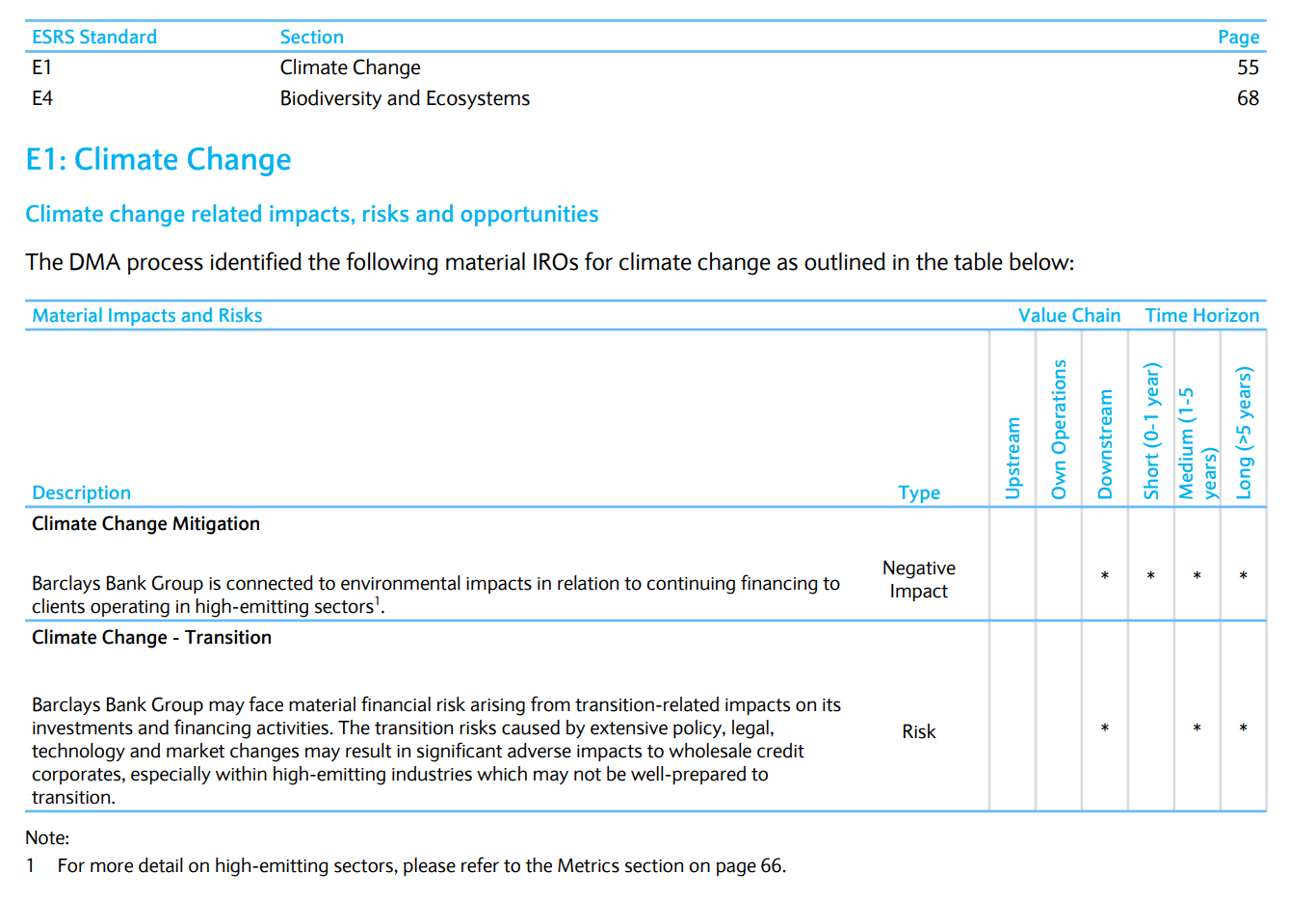

Like we have seen on quite a few ESRS reports now, Barclays points out their material IROs at the start of each topic standard section.

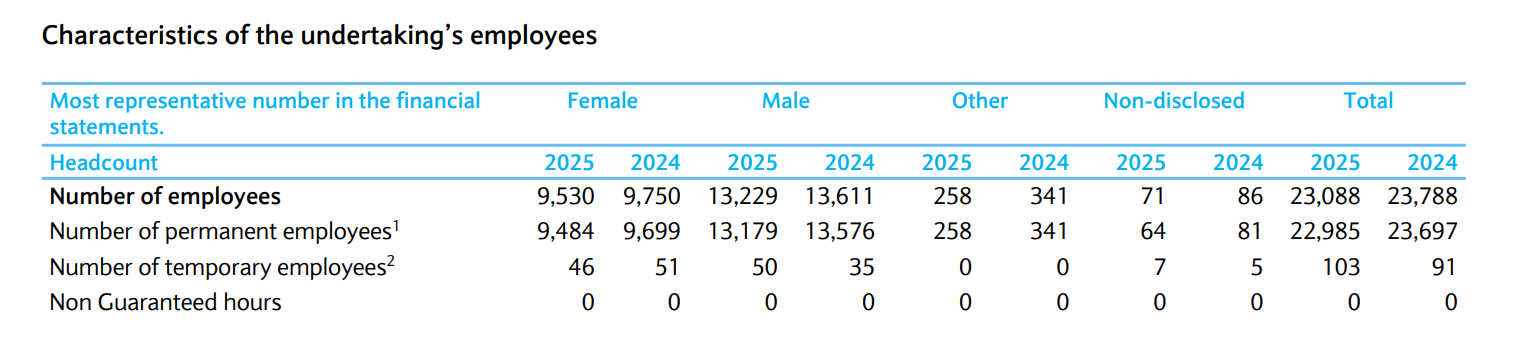

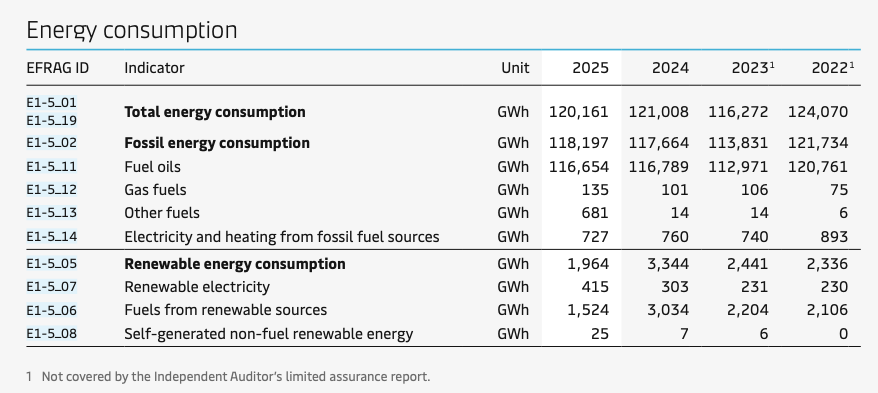

Similar to other CSRD reports assessed, Barclays metrics are summarised for the CSRD reporting years only. They do not provide historic data prior to CSRD.

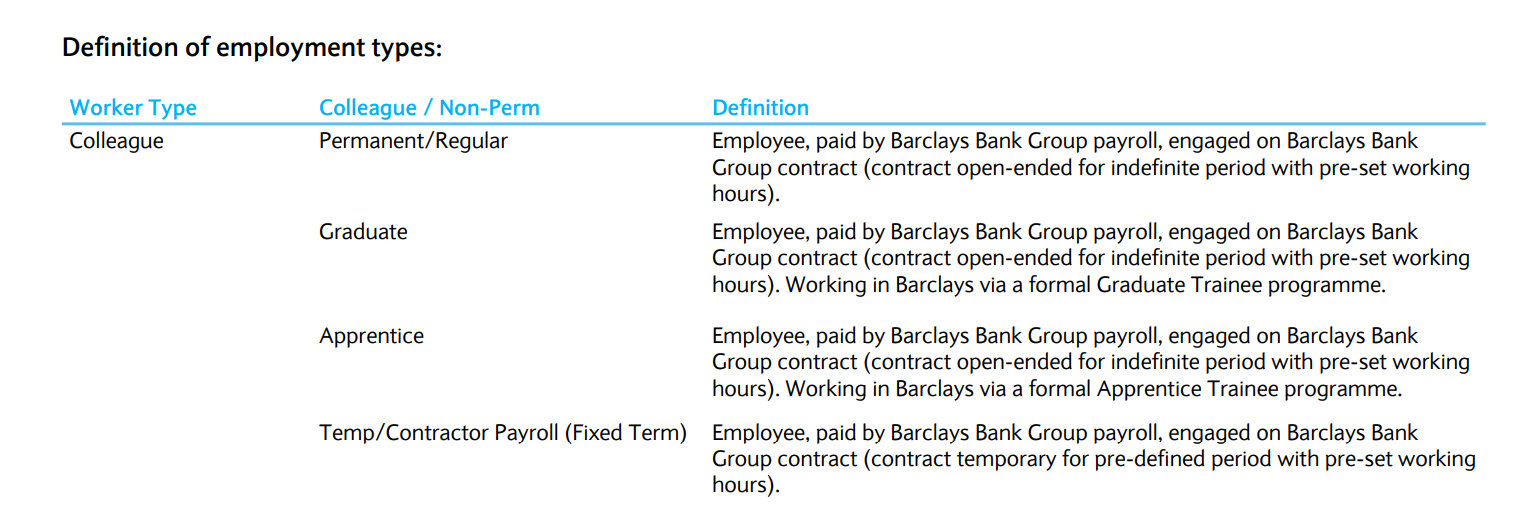

Below their metrics disclosure they provide additional information about the definitions used in their disclosures.

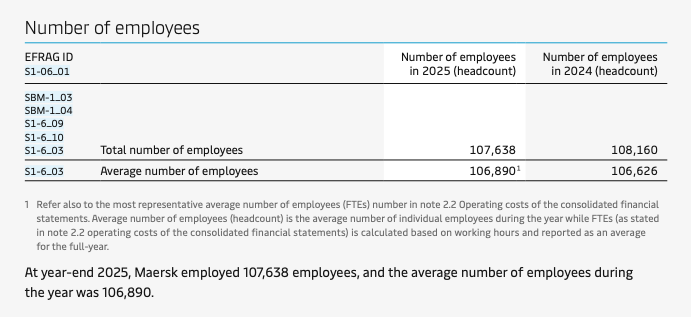

Maersk, similar to other best practice companies we have seen included the EFRAG data codes by their metrics. We also saw metrics going back until 2022 which is farther back than most other CSRD companies who have done only FY24 and FY25.

For other data categories they did not go as far back in time, for example, employee data is only until 2024.

When they open each material topic section they show their target and current progress versus the target.

A best practice from the Maersk report is when they did amend an IRO they made this very clear to the reader by labeling IROs as “No Change” or “Amended.”