Interviews

Building Internal Controls for CSRD: Lessons from a Wave 1 Company

An interview with Seraphina Kim about applying internal controls for CSRD disclosure.

This article compares two consecutive years of CSRD-aligned disclosures across five large, Denmark-headquartered companies—Ørsted, Novo Nordisk, Vestas, Danske Bank, and Pandora—to understand what shifts after the “first-time reporting” year. We are specifically focusing on decisions made around IRO disclosure related to their DMAs.

While we give company specific examples in this article and screenshots, we have highlighted the changes found below:

Reduction of IROs: Most of the companies we looked into did reduce their IROs overall and in some cases removed Topic standards from their disclosure. We generally saw this addressed directly by the company to explain the difference.

Material Topics Grouped By E, S and G theme versus Priority Theme: 4 of the 5 companies maintained the grouping of their material issues by “Environmental,” “Social” and “Governance” themes. Novo Nordisk took a different approach where they had x4 “Prioritised Topics” and a longer list of “Other Material Topics.”

Year on year data comparison for CSRD data but not necessarily previous fiscal year: A good learning for Wave 2 / Wave 3 companies is while we did see consistently historic data for FY2024 versus FY2025, virtually no company published data for FY2023 (e.g. Before CSRD). The expectation would be is that companies are not attempting to recalculate historic data before their first year of official CSRD disclosure.

Check out the article we published last year on FY2024 CSRD disclosure in Denmark.

We looked at:

Orsted’s topic standards stayed the same but their material Issues decreased from 40 to 31. See below the respective statements on this:

FY2024: “In total, 40 impacts, risks, and opportunities (IROs) have been assessed as material, comprising of 7 positive impacts, 23 negative impacts, 8 risks, and 2 opportunities (see pages 69-72).” Page 67.

FY2025: “In 2025, we conducted a double materiality assessment (DMA), in which we identified and assessed 31 material impacts, risks, and opportunities (IROs) comprising 6 positive impacts, 15 negative impacts, 8 risks, and 2 opportunities. “ Page 65.

Orsted also offered narrative about this change:

“While the same material ESRS topics were reaffirmed in our 2025 DMA, we merged some IROs that were similar in nature and management, reducing the number of IROs from 40 to 31. Our materiality threshold is unchanged, and even though some topics have IROs scored differently, this did not change the overall outcome of which topics are above and below our materiality threshold.”

Other Highlights from Orsted Disclosure:

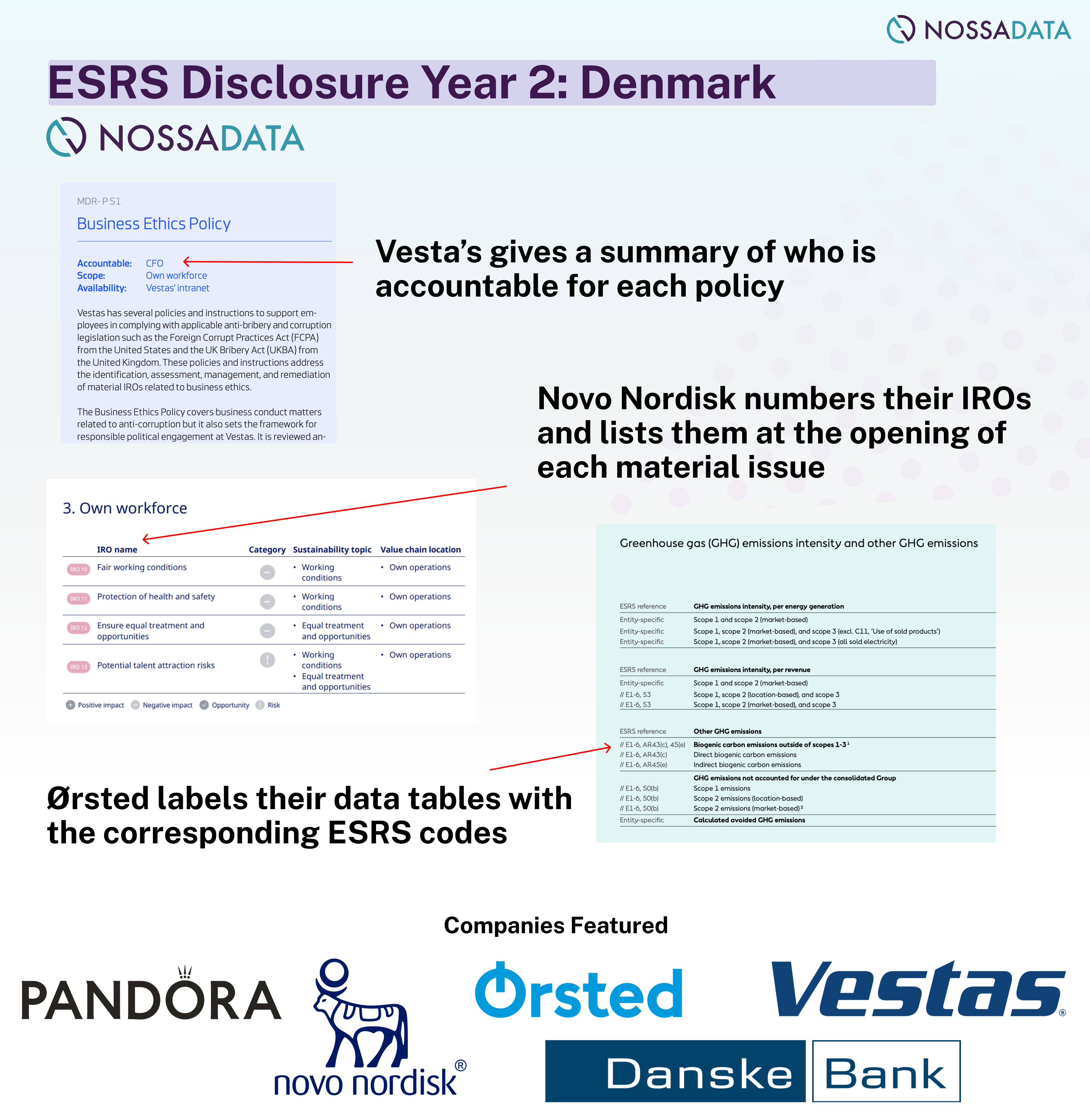

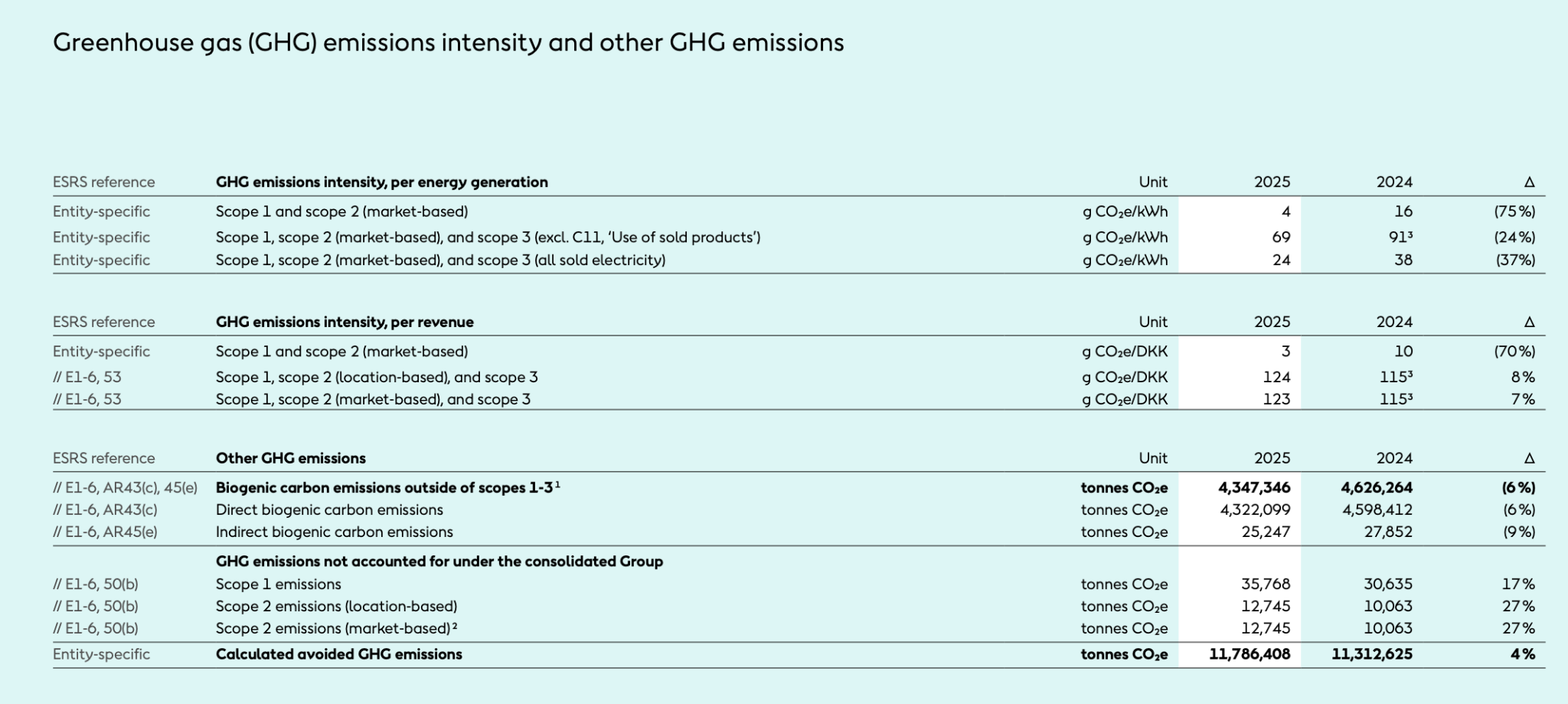

Orsted’s data tables are a great best in class example for companies that want a clean way to present their quantitative metrics. They helpfully label each data point with it’s corresponding ESRS code and show the YoY comparison.

Example of IRO changes: See below a comparison of what was listed as a Positive Impact in FY 2024 vs FY2025.

Positive Impacts in FY2024

Positive Impacts in FY2025

Novo Nordisk changed their topic standard communication from classifying them under E S and G to having x4 “Prioritised Topics” and x5 “Other Material Topics”. Alongside that, they explained “Only minor refinements have been made since the 2024 Sustainability statement, mainly to clarify and reclassify certain IROs. As part of this update, the following sub-topics have been descoped for 2025: substances of concern (E2), severe human-rights-related impacts (S1) and equal-opportunities-related topics (S2).”

See comparison images below:

Considering their IROs, each IRO was numbered and shown by its corresponding topic.

Similar to Orsted, they did offer data comparability for FY2024 and FY2025. They did not always show data from before their first CSRD report. See the below data tables as an example.

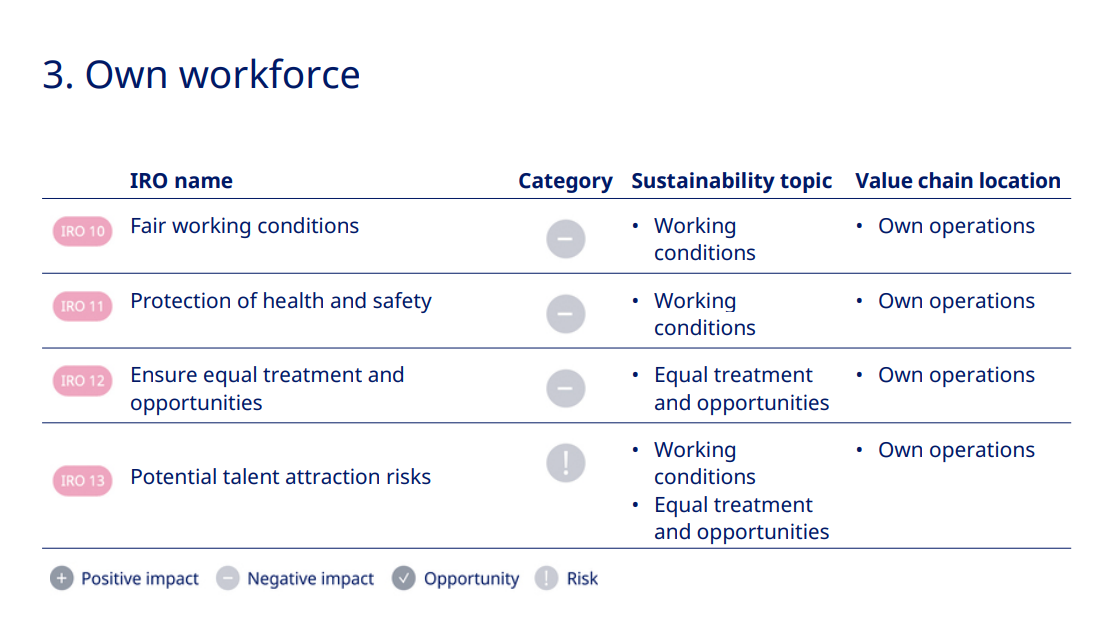

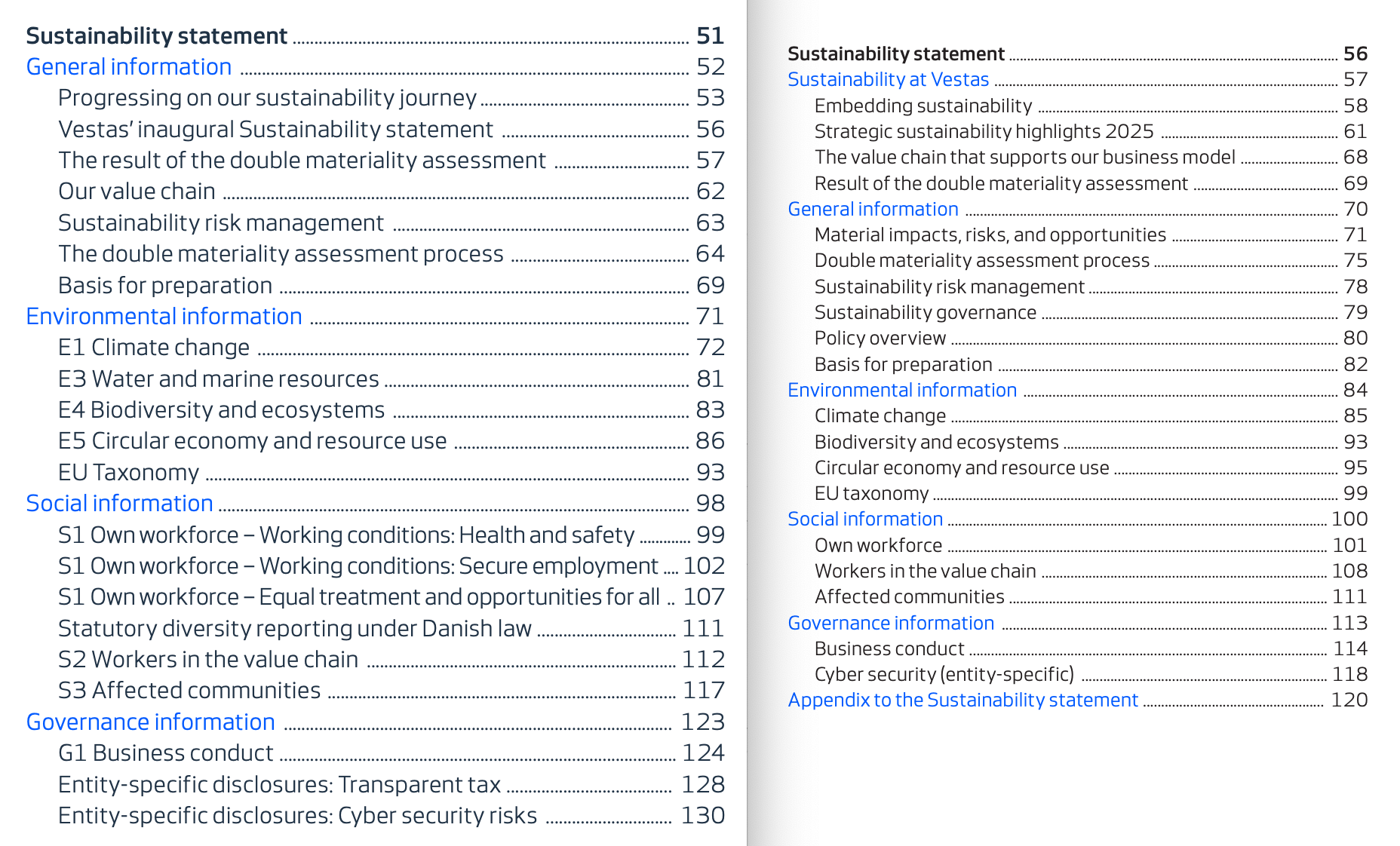

Similar to other companies we have assessed, Vestas did remove some topic standards in FY2025 and overall shortened their sustainability statement versus FY2024. See the below image comparing the appendixes listing Sustainability Topics in FY2024 (Left) and FY2025 (Rights). Vestas explained in regards to their DMA: “Only minor refinements have been made since the 2024 Sustainability statement, mainly to clarify and reclassify certain IROs. As part of this update, the following sub-topics have been descoped for 2025: substances of concern (E2), severe human-rights-related impacts (S1) and equal-opportunities-related topics (S2).”

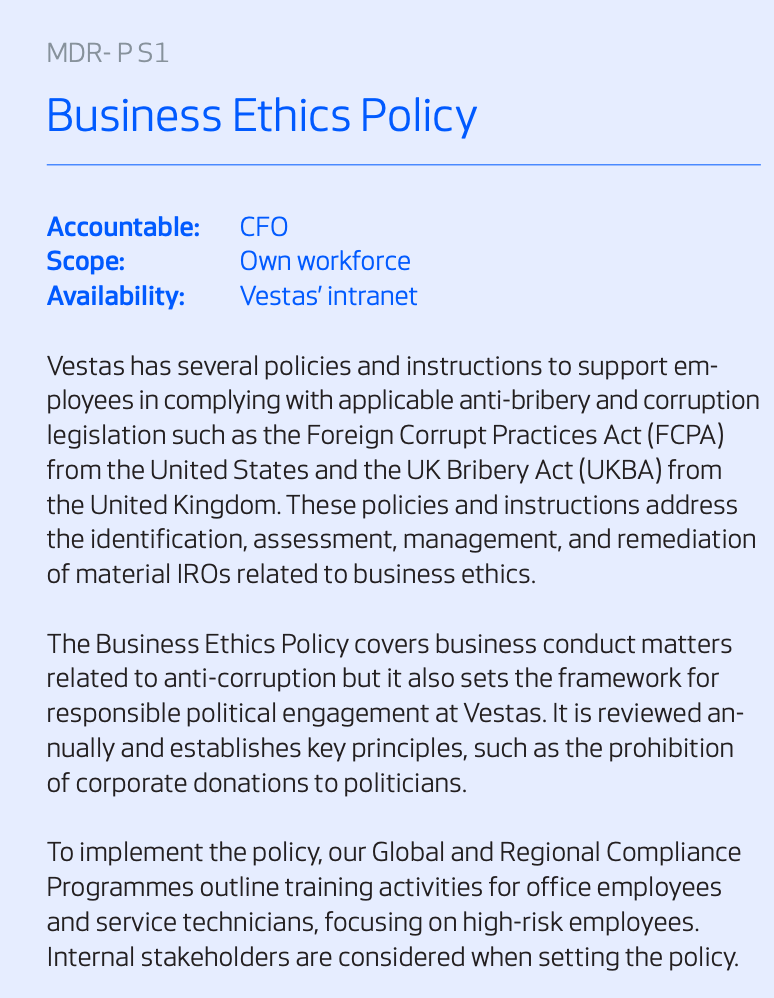

A strength in Vestas disclosures is it is very clear their accountability structure on policies. Each policy is labeled with Accountable, Scope and Availability. See the below example on Business Ethics.

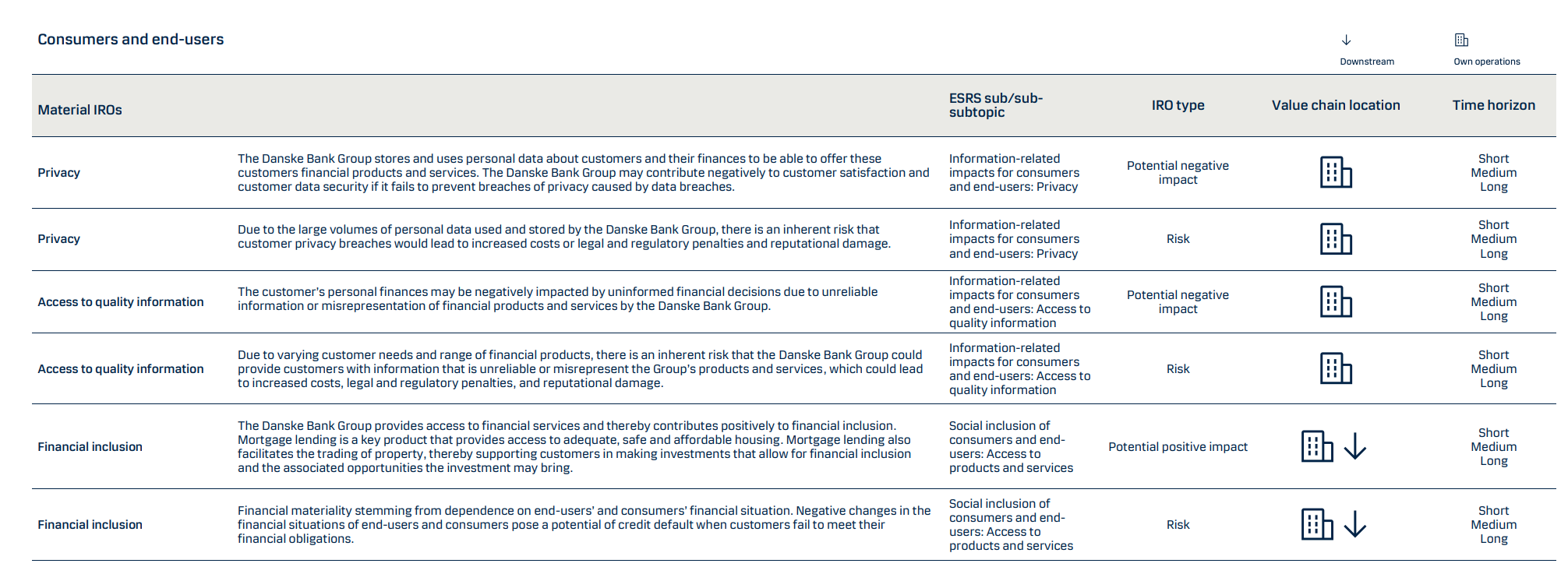

Like the other companies assessed, Danske Bank has also made changes to their material issues and IROs overall. “We have refined the 2024 DMA process by aligning the impact materiality assessment and financial materiality assessment further and have integrated these into one single assessment process. Additionally, we have introduced a strategic overlay, calibrating the two assessments with each other and with stakeholder perspectives, industry trends and existing strategic priorities. The refined 2025 DMA methodology has resulted in an identification of three impacts related to S1 Own workforce (see Step 3 below) and the removal of four entity-specific risks and impacts related to Governance (see Step 2 below).”

See the below example on their material IROs for Own Workforce:

Pandora was the only company we looked at that showed an additional material topic standard introduced in Pandora’s cases was “Nature-related” Financial Disclosures. They also changed the language of one material issue from “Diversity and Inclusion” to “Inclusion and belonging” - a popular choice after the D&I disclosure backlash of 2025.

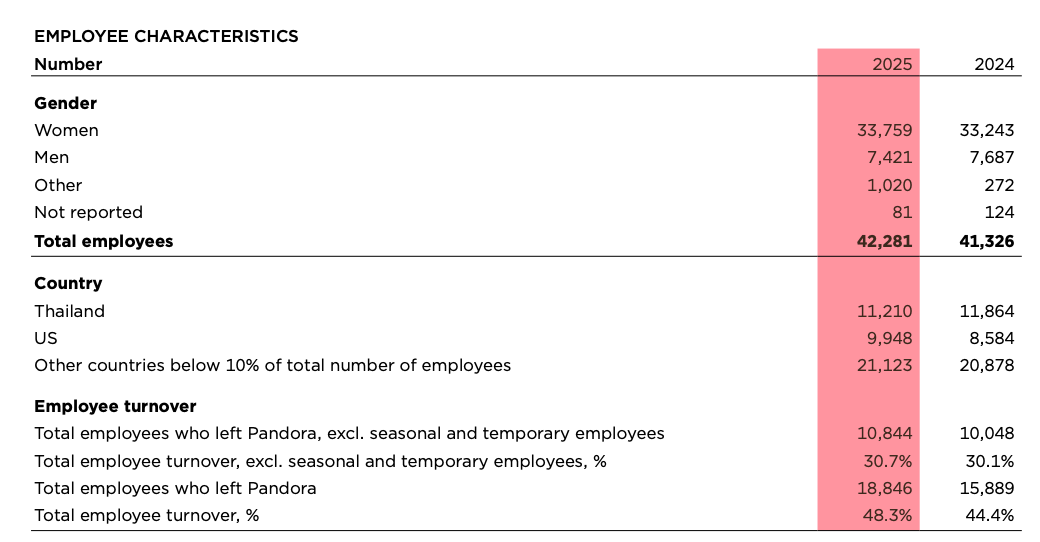

Similar to other companies we looked at, Pandora shares their data tables with comparisons between FY2024 and FY 2025. See example below on “Employee Characteristics”