Interviews

Building Internal Controls for CSRD: Lessons from a Wave 1 Company

An interview with Seraphina Kim about applying internal controls for CSRD disclosure.

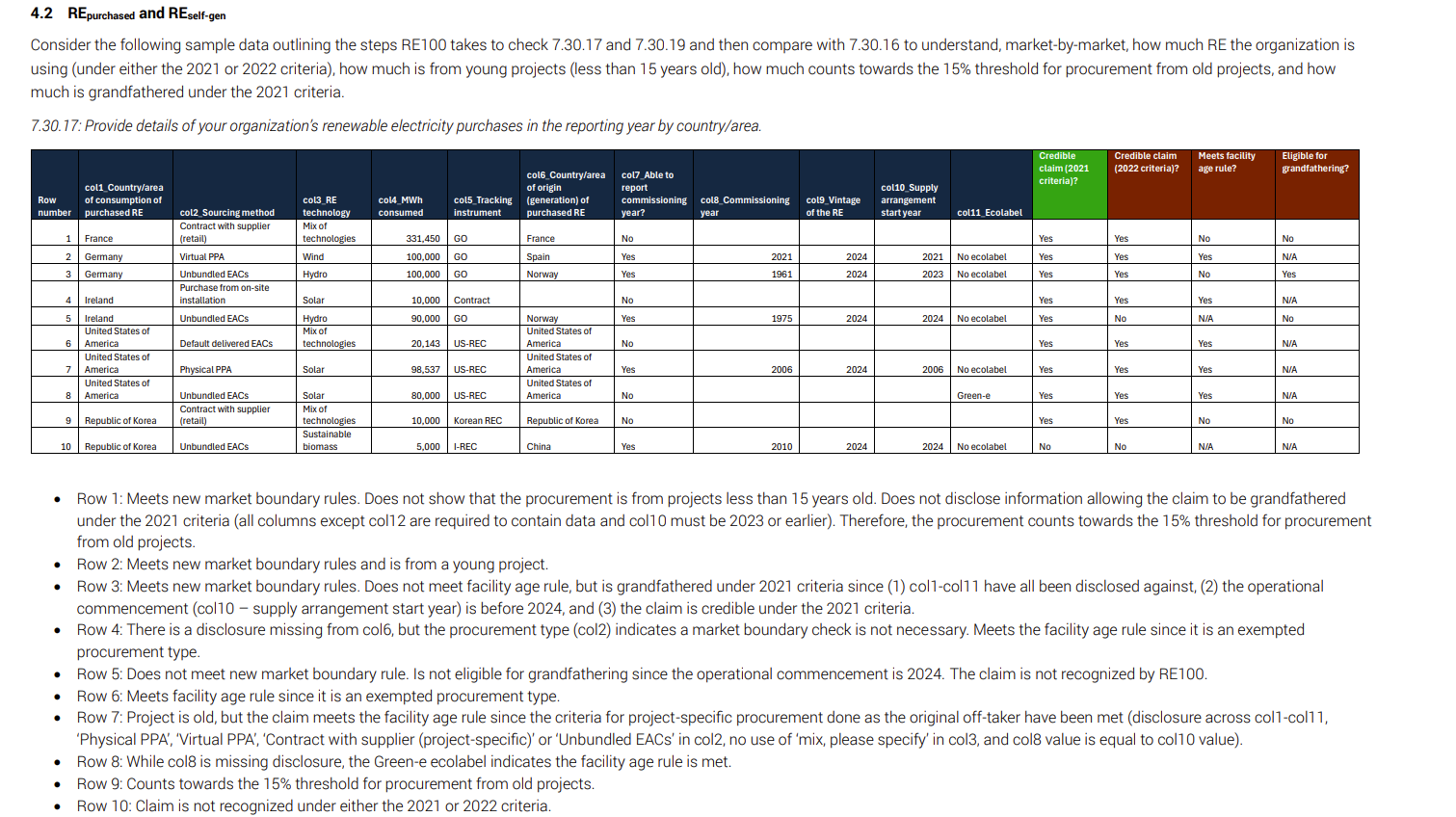

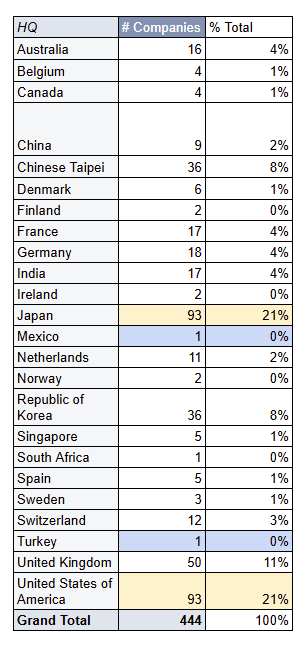

Over 440 companies worldwide have committed to 100% renewable electricity through the RE100 global initiative. These big companies consume more electricity than entire countries and have massive influence over global energy markets and the transition to zero carbon grids.

The relationship between RE100 membership and Carbon Disclosure Project (CDP) performance is fascinating. While renewable electricity is just one part of a company’s overall climate strategy, the overlap of these two influential frameworks gives us a unique view into how companies navigate the energy transition and sustainability reporting landscape

Reach out to us to access Nossa Data's database of RE100 companies' CDP 2024 scores.

RE100 was born as a global initiative during Climate Week NYC in 2014 and is now the world’s most influential corporate renewable energy program. Led by Climate Group in partnership with the Carbon Disclosure Project (CDP), this collaborative framework has changed the way big companies approach renewable electricity procurement and reporting.

The initiative’s mission is to accelerate the global shift to zero carbon grids at scale through collective corporate action. By creating clear demand signals for renewable power, RE100 drives market transformation that goes far beyond individual company operations to influence entire energy systems and policy frameworks.

Since its launch, RE100 has grown rapidly from a handful of founding members to over 440 companies in 175+ markets. This rapid growth reflects growing corporate recognition that renewable electricity procurement is both a climate imperative and a business opportunity.

The combined electricity demand of RE100 member companies is over 570 TWh annually, making the collective membership the equivalent of the 10th largest electricity consumer in the world. This scale gives RE100 massive influence in renewable energy markets, driving project development and policy reforms across multiple regions.

The partnership between Climate Group and CDP creates a full ecosystem for renewable electricity commitments. Climate Group provides strategic leadership and market development expertise, while CDP provides technical frameworks, disclosure platforms and independent scoring methodologies that many members use to report progress and governance quality.

The primary eligibility threshold is companies with over 100 GWh annual electricity consumption, focusing on the world’s biggest businesses to amplify market-shaping demand signals. This threshold means membership includes companies with sufficient scale to drive meaningful renewable energy market development and grid transformation.

Exceptions are made for Fortune 1000 companies, major industry players and strategic regional participants who have significant influence even if their absolute consumption is lower. These exceptions recognize that market leadership goes beyond pure consumption metrics to include innovation capacity, supply chain influence and regional market development potential. All RE100 members must make a public commitment to get to 100% renewable electricity by 2050 or earlier for their entire operations across all global facilities. This commitment covers all electricity used in company-controlled operations, requiring comprehensive accounting and procurement strategies that often span multiple markets and regulatory frameworks.

The program requires interim targets that provide accountability milestones: 60% renewable electricity by 2030 and 90% by 2040. These interim targets ensure steady progress while allowing companies flexibility in procurement timing and strategy development based on market conditions and business planning cycles.

Annual reporting through RE100 or CDP disclosure platforms provides transparency and enables progress tracking across the membership. Companies must provide detailed electricity data annually, including facility-level consumption, renewable sourcing methods, commissioning dates and third party verification of renewable electricity claims.

Third party verification has become more important since 2024, with enhanced requirements for credible claims and data integrity. Companies must ensure chain-of-custody certification or independent auditing aligned with CDP reporting standards, provided all RE100 technical criteria are met.

RE100 accepts specific renewable sources including solar, wind, sustainable hydropower, geothermal and biomass that meet established sustainability criteria. These sources must demonstrate environmental integrity and avoid negative ecological impacts through appropriate certification and monitoring systems.

Nuclear energy is explicitly excluded from renewable accounting within RE100, despite being low carbon. This exclusion reflects the initiative’s focus on truly renewable resources that can be indefinitely replenished and align with broader sustainability principles beyond carbon reduction alone.

The 2025 introduction of a 15-year age limit for renewable facilities represents a significant shift towards additionality and system transformation impact. Under these updated technical criteria, electricity from renewable facilities older than 15 years will not receive full credit towards RE100 progress targets, encouraging procurement from newer assets.

Geographic matching requirements mean companies must source renewable electricity within the same market boundaries as their consumption. This rule maintains environmental integrity by ensuring renewable electricity procurement creates real grid impact in the regions where companies operate their facilities.

Additionality principles require unique, traceable renewable electricity attributes that contribute to new renewable capacity or system transformation. Companies must demonstrate their procurement drives incremental renewable energy development rather than simply redirecting existing renewable electricity from other uses.

The program conforms to GHG Protocol Scope 2 quality criteria, requiring vintage alignment to reporting years, avoidance of double counting and proper documentation of attribute ownership through Energy Attribute Certificates or equivalent contractual instruments.

The membership process typically takes 8 steps and 2-3 months from initial engagement to public commitment. Companies must first validate eligibility through electricity consumption thresholds or demonstration of strategic industry influence.

Initial assessment includes scoping of global electricity loads and operational boundaries to ensure accurate target setting and procurement planning. This phase often reveals data management challenges and metering gaps that need to be resolved before membership approval.

Development of renewable electricity roadmaps and target timelines requires detailed analysis of market access, procurement options and cost implications across all operational markets. Companies must show feasible pathways to 100% renewable electricity by 2050 and interim milestones.

Commitment to annual reporting requires integration with CDP disclosure platforms and establishment of third party verification processes. Early data governance setup is key as RE100 requires facility-level commissioning date disclosure and comprehensive electricity data annually.

The onboarding process includes training on technical criteria, market boundary rules and acceptable procurement instruments. Companies must understand evolving requirements like the 15-year facility age limit and enhanced verification standards to remain compliant over time.

Implementation planning for complex global portfolios often takes longer than the initial approval process, requiring ongoing coordination between sustainability teams, procurement departments and facilities management across multiple geographic markets.

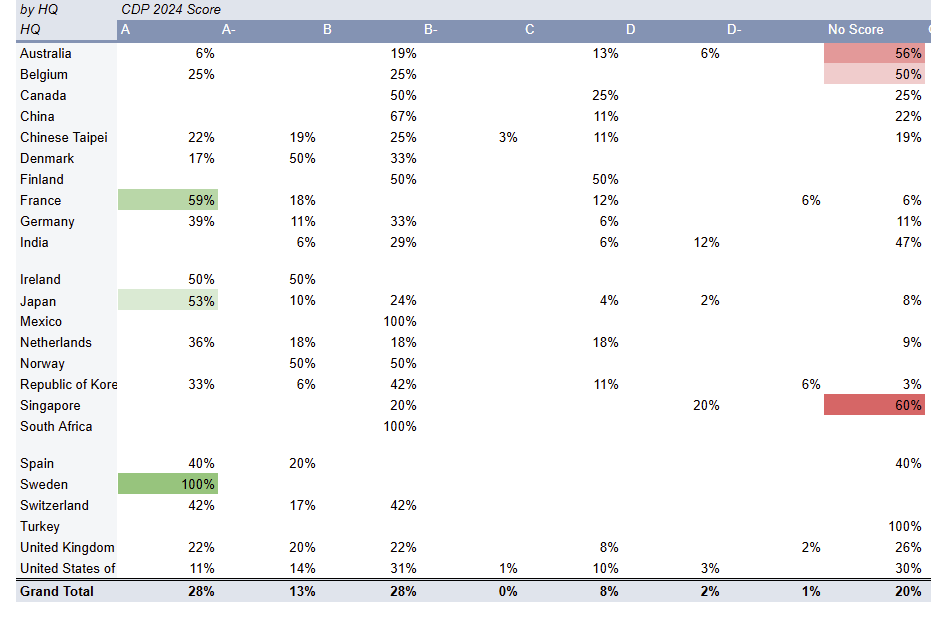

RE100 and CDP have partnered to support company disclosures on their renewable electricity commitments. RE100 companies disclose this information through CDP on an annual basis. The best performing companies for CDP are listed on CDP's A-list. Since renewable electricity is only found in the Climate Change module, we're only looking at the CDP Climate Change A-list.

For the full dataset of RE100 Members and their CDP scores, schedule a call with a Nossa Data representative.

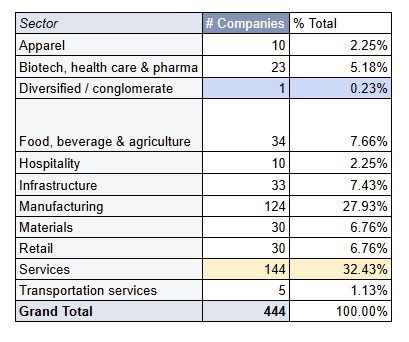

Of the 444 member companies, ~60% of RE100 members are from the Services and Manufacturing sectors, 144 and 124 respectively.

Interestingly, Infrastructure can rank as both one of the best performing sectors (% of companies on A-list) and one of the worst (% of companies without a score). It has 12 companies on the A-list, and another 12 without a score.

The top performing sectors, as a % of companies from that sector included in CDP's A-list, are:

The worst performing sectors, as a % of companies from that sector who didn't receive a CDP score in 2024, are:

There were a couple standalone companies who were either the only company listed in its sector, or the only one to achieve an A in CDP Climate Change:

Japan and the USA account for the most members respectively, with 93 companies (21%) each of all RE100 member companies. However, there is a definite disparity in how well they do in CDP:

Sweden and France were the top 2 performers in front of Japan. Despite only 3 Swedish companies are RE100 members, all 3 are on CDP's A-list (100%), while France have 10 out of 17 companies on the CDP A-list (59%).

The worst performing countries, as a % of RE100 members without a CDP score, are:

Only 2 countries were only represented by 1 RE100 member: Mexico and Turkey. Those companies are:

With CDP no longer publishing public disclosures (requires payment to access), the impetus is on companies themselves to disclose their progress towards their targets, including renewable electricity performance.

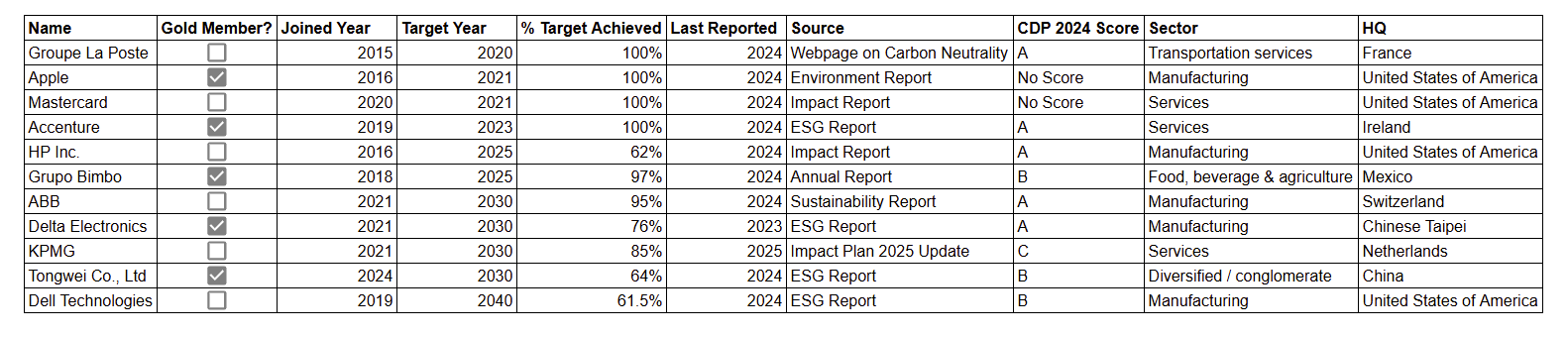

Are there any commonalities between A-listers and % targets achieved?

Short answer: not really. CDP encompasses many more requirements than just renewable energy within its climate change module, with only 5 CDP questions directly assessed based on RE100 metrics.

Aside from the companies already mentioned above, we analysed a further 8 companies from the Services and Manufacturing industries to lead us to this conclusion:

Since 2024 third party verification is required for all renewable electricity claims, with increased focus on chain-of-custody for Energy Attribute Certificates and market boundary rules. Companies must navigate multiple certification requirements across multiple markets and procurement instruments.

Common mistakes are counting retail “green” products without underlying Energy Attribute Certificates, using certificates outside market boundaries, or relying on biomass and hydropower without recommended sustainability certifications. These errors can put RE100 compliance and CDP scoring at risk.

Power plant commissioning date disclosure is now critical under the new 15 year facility age limit. Companies sourcing from older hydro or legacy wind facilities must re-assess their portfolios to maintain full credit, potentially increasing certificate costs or requiring new PPA development.

Global electricity data management across multiple operations is a recurring challenge, especially for companies with varied utility structures, leased sites and complex submetering arrangements. Service-heavy and hospitality portfolios have particular difficulties with tenant-landlord metering splits and multiple utility relationships.

The 2025 age-limit requires companies to blend old attributes (partial credit) with new-build linked instruments to stay on track to targets. This transition requires sophisticated procurement strategies and potentially higher costs for credible claims.

Market boundary compliance across evolving European certificate rules requires ongoing attention to regulatory changes and cross-border trading developments. Companies must ensure their procurement strategies adapt to changing geographic eligibility requirements.

On-site renewable generation is the most direct way to renewable electricity through solar panels, wind turbines and other technologies installed at company facilities. This approach provides clear traceability and often cost savings and reduced grid dependence, but site constraints and intermittency means full load coverage is not possible.

Power Purchase Agreements (PPAs) have become the central instrument for large electricity demand, offering long term price stability and direct connection to renewable project development. Virtual PPAs allow geographic flexibility within market boundaries while delivering bundled energy attribute certificates to buyers, enabling procurement across multiple operational footprints.

Energy Attribute Certificates are the most global way to match electricity consumption with renewable attributes, especially in regions with limited PPA frameworks. These instruments enable annual true-up accounting but raise questions around additionality when sourced from existing plants or low priced markets. Investing in new off-site renewable power plants supports industrial-scale commitments and demonstrates clear additionality through project financing and development support. Many manufacturing companies do this to secure long term renewable electricity supply and contribute to renewable capacity expansion.

Hybrid approaches combining multiple procurement strategies cover companies with diverse portfolio geographic and timing requirements. These strategies often evolve over time to higher-additionality instruments as markets mature and company expertise develops.

The shift towards new-build sourcing reflects growing recognition that renewable electricity procurement should drive system transformation rather than simply redistribute existing renewable attributes. This aligns with the 15 year facility age limit and broader additionality principles.

European markets lead global EAC solutions through mature Guarantees of Origin (GOs) systems that enable robust corporate renewable electricity verification. The region’s established market infrastructure and regulatory frameworks provide many options for contractual instruments and disclosure practices.

North American Renewable Energy Certificates (RECs) operate under established standards and registries that complement utility green tariffs and corporate PPAs. This market structure allows for blended portfolios that combine unbundled purchases with direct procurement instruments based on company needs and market access.

International RECs (I-RECs) expand global coverage across Asia, Latin America, Africa and the Middle East, providing standardized attribute tracking in regions without domestic certificate systems. The growing liquidity of I-RECs has made Energy Attribute Certificates the primary instrument for many to claim renewable electricity globally.

Market access through EACs enables companies to achieve 100% renewable electricity targets even in regions with limited PPA frameworks or regulatory barriers to direct procurement. This has been critical for global companies with operations across multiple markets with varying renewable energy policy maturity.

RE100’s market boundary criteria require that certificates be procured within the same market or recognized boundary as consumption to maintain environmental integrity. Recent European boundary clarifications reflect evolving grid integration realities and cross-border trading developments.

What is the minimum electricity consumption requirement for RE100 membership?

The initiative primarily targets companies with annual electricity demand above 100 GWh, focusing on influential businesses that can create significant market demand signals. Exceptions exist for Fortune 1000 companies and strategic industry participants with significant influence despite lower consumption levels.

**How do Energy Attribute Certificates work for renewable electricity verification?**Energy Attribute Certificates represent the environmental attributes of 1 MWh of renewable electricity generation. When properly claimed and retired within the right market boundaries and vintage periods they enable companies to match electricity consumption with renewable generation and report market-based Scope 2 emissions accordingly.

What happens to renewable facilities older than 15 years under new 2025 criteria?

Electricity from facilities older than the 15 year age limit will not get full credit towards RE100 progress after 2025. Companies must disclose commissioning dates and may need to shift procurement towards newer assets or instruments linked to incremental capacity to maintain full counting under the new criteria.

Can companies join RE100 if they operate in markets with limited renewable options?

RE100 allows counting high-renewable grid mixes (above 95%) where no active procurement mechanisms exist and recognizes International RECs and cross-border solutions within defined boundaries. This enables participation from markets with limited options, though compliance and verification remain essential.

How often must RE100 members report their renewable electricity progress?

Members report annually through RE100 or CDP disclosure platforms, with third party verification now required. Documentation must include certificate retirements, PPA details, on-site metering, commissioning dates and market boundary adherence to maintain compliance.

What support does RE100 provide for developing renewable electricity procurement strategies?

RE100 provides technical guidance on procurement instruments, market boundary requirements and verification standards. The initiative offers resources on Power Purchase Agreements, Energy Attribute Certificates and on-site generation options and connects members with market expertise and best practices.

The relationship between RE100 membership and CDP performance shows that renewable electricity procurement is one part of overall climate leadership, but success in renewable electricity targets doesn’t guarantee high CDP scores without broader climate strategy elements. As both frameworks evolve companies pursuing a sustainable future must balance renewable power procurement with carbon footprint management, supply chain engagement and transition planning to be recognized as true climate leaders in the accelerating energy transition.