Interviews

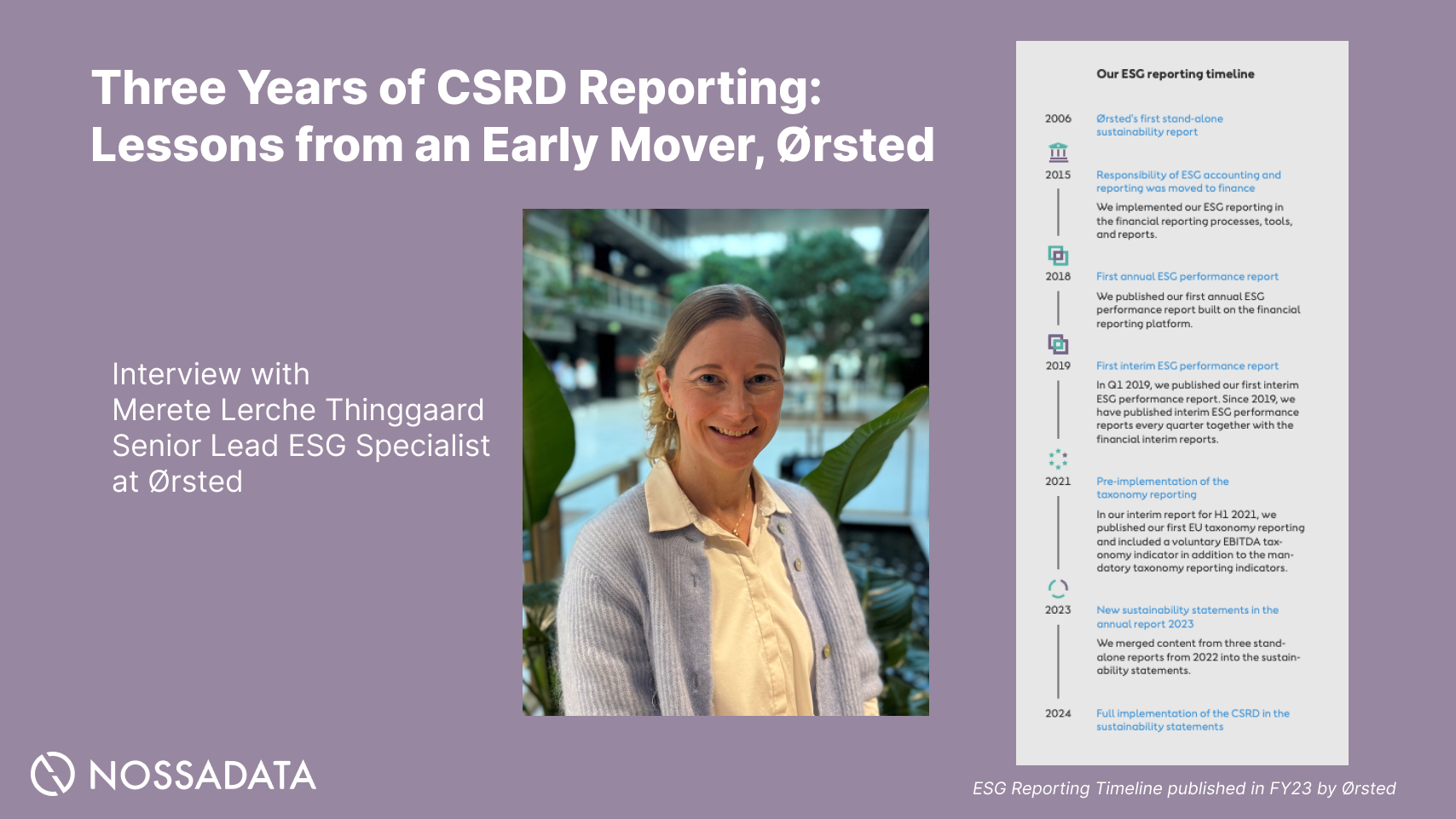

Three Years of CSRD Reporting: Lessons from an Early Mover, Ørsted

An expert interview with Merete Lerche Thinggaard, Senior Lead ESG Specialist at Ørsted, on three CSRD reporting cycles.

We interviewed Jeremy Richardson, Global Equities Senior Portfolio Manager at RBC Global Asset Management (UK).

In 2020, RBC published its Corporate Governance and Responsible Investment Annual Report, which can be read in full here.

We have a shared appreciation of the challenges of investing and what we're trying to do for our clients. Because we have similar clients, those clients have similar challenges. Therefore, when we think about how we can best deliver for our clients, it’s natural that we end up in a similar place.

Every investment team has the freedom to develop and implement its own investment philosophy, and yet when you look at all the investment teams, there's a silver thread that runs through them because we all have a similar definition of success.

“We all understand that one of the best ways to add value to a client's portfolio over time is to take a long-term approach. When you take a long-term approach, you care about things that should drive long-term fundamentals.”

When you think about your goals in owning great businesses and being a long-term owner, you realise that ESG is an extension of that because it’s being mindful about those long-term consequences of your actions. So, it seems very natural to think about ESG issues from the investment team’s point of view. This is reflected in the nature of the exposures we have and the types of companies we're investing in across the firm.

Climate is one area that I would highlight. It’s been developing and started off with informal conversations between clients and managers, but now we’re beginning to see this becoming formalised within the deliverables and, in some instances, within contracts. On one level this is a very positive development, because as a society, we have a very significant challenge in front of us. This demand from asset owners will play an important part in generating solutions that are needed to hit society’s global climate targets.

Asset owners making such expectations explicit, rather than implicit, is very powerful. If the customer is clear about what they expect from their asset manager, then the asset manager will adjust their behaviours or develop solutions and products that specifically address those needs. I think this is a very constructive development, although it does put greater onus and requirements on the asset manager’s reporting.

“Asset owners are really beginning to understand the influence they have within the asset management industry as well as their ability to shape outcomes by making their expectations explicit in this way.”

However, we need to be careful about this because there are potential pitfalls about creating elevated expectations. For example, perhaps you favour a particular type of company, maybe for its ESG credentials, and you decide to buy a stock. That purchase is a financial transaction. The money goes to the person who sold you that stock, it doesn't go to the company. When we think about secondary markets, we also need to be cognizant that we're really talking about a kind of signalling in terms of directing flows of capital to businesses of which we approve in terms of ESG. That signalling can be helpful but to what extent does it meet investors’ expectations of making an impact on the world?

When the pandemic happened, there was a big focus of attention from companies on the ‘S’ of ESG; I think this remains incredibly topical. Back in the middle of 2020 it was all about PPE, social distancing and supporting remote workers. Employers were trusting their workforce to do their jobs when they were no longer clocking in and out every day. For many businesses this proved to be manageable. But for many it was also incredibly stressful. For example, we would not have been able to get through the pandemic nearly as well as we did were it not for the continuation of food delivery, etc.

“At the moment, it seems to be evolving as conversations focus on the longer lasting consequences of the pandemic.”

For example, for workers today there's a growing sense that the salary is not the primary attraction of a job, rather it's the nature of the job itself and whether the work is rewarding. I think the pandemic highlighted that there are many jobs that offer little sense of reward.

Let’s take road haulage, the meat packing industry or delivery drivers; these are all examples of jobs where the competitive forces within those industries have meant that there hasn’t been the investment into the nature of work. We’re familiar with the phrase ‘The Great Resignation’, where we are now faced with a reduced workforce. With many people deciding to retire earlier and with reduced migration, there is a much more constrained labour market and it's putting power back into the hands of the worker. So, we’re seeing shortages, not across the board, but within particular industries and I would argue that this has much to do with the nature of the job itself.

I think this is going to be quite a challenge for certain business models to respond. However, they must respond if they're going to survive. This could actually be a very positive dynamic in the long run because if we can get investment to improve the quality of these jobs, then that would be good for society.

I think it's a particularly tricky one as an outside investor. This is because we have an outside view rather than an inside view. In this sense, you don't get to see the detail of the levels of inventory the company has or its number of unfulfilled orders, etc. This is commercially sensitive information not appropriate for the public domain. This is where active shareholder engagement with companies can give investors some comfort around the way in which management approaches things like operational risk.

“By talking with companies and learning details such as the number of suppliers on which they depend, we can generate an understanding of their sources of risk.”

A good example would be within the automotive industry in Japan, whose chip providers in Thailand were severely impacted by floods a few years ago. Their ability to produce cars depended on just a handful of key components which came from a limited number of suppliers. Japanese producers learned about their supply chain sensitivity. In response, they took steps to diversify their sources of supply. They also took steps to manage their inventory levels in case of future difficulties.

In contrast, many European manufacturers have an aggressive focus on price. In the interest of efficiency, they’ve been lowering the numbers of inventories and have a ‘just in time’ kind of approach. Now, as a result of the pandemic, semiconductors have been in scarce supply once again. But we've seen bigger manufacturing impacts coming from some of the European automotive makers than we have from some of the Japanese makers. I would argue that this is because lessons were learned around the security of their supply chains. So, is it ‘just in time’ or do we have to move to a ‘just in case’ type of supply chain?

I would like to point out the importance of the relationship companies have with their supply chains. Within our investment team, we often talk about these providers of extra financial capital.

“If you enjoy healthy relationships with your suppliers and you look after them when times get difficult, they're more likely to look after you. In times of scarcity, they will provide those scarce resources to their customers who they know are going to pay on time and who have supported them.”

We often talk about trying to understand the personalities of companies. I believe that by asking contextual questions and actively engaging with management, we can get a stronger sense on how they appreciate these risks and the extent to which they're building a more resilient business.

We have always asked about management teams and considered the long-term consequences of investment actions. Much of this was doing ESG before ESG was even an accepted term and flows from our long-term ownership approach and mindset. This is why we have always encouraged investors not to be intimidated by ESG because many investors are probably already doing it to some extent. If you're thinking about the long-term, then there's naturally going to be elements of ESG already within your process.

Carbon emissions reporting: I'm pleased to say that as an industry, there's been a significant increase in the number of companies that are now reporting on their emissions. There used to be a lot of guesswork and benchmarking against competitors. Now, with scope 1 and scope 2 emissions, the quality of data has significantly improved. It’s given way to more recent conversations around things like the TCFD regarding the impact of climate change on a company's financial capital.

Engagement with companies: Now the most recent climate conversations are about how resilient the business is and what the business can do in preparation for climate change. A lot of companies are moving along that conversation, but not everybody is moving at the same speed. We see differences by size as larger companies have the resources to think about net-zero. But for smaller companies, this is a challenge that still lies in front of them. As owners, we need to engage with companies to help them along that journey.

Communication with stakeholders: Companies can work really well when they listen to shareholders and shareholder democracy is a great thing. But the way that the proxies are put forward are often not easy for investors to digest. I would love for companies to be able to better communicate what they’re trying to achieve to their shareholders. Let's have a narrative around what governance means to companies and how that connects with stewardship, and why these proxy voting proposals are congruent with that narrative arc. Because if you look at a lot of the documents, you find that they're long, they're written in legalese and they're really hard to digest. Going forward, I would like to see simple language in context. I think that will really help a lot of people understand the direction of travel.

On the one hand, I feel enormously heartened that ESG has gone from being a peripheral point of view, to now being very much mainstream. If we think about ESG as a movement, it’s never been healthier. However, if we think about ESG as a goal, I'm less clear about what the target is. My caution comes down to the desire of some within the investment world to have easy answers. It’s challenging because ESG issues often require context. Distilling everything down to a quantitative number doesn't necessarily work and can raise the risk of greenwashing because you end up building a portfolio to maximise the quantitative output.

There’s a risk of collective window dressing in order to improve quantitative scores. There is no positive financial impact here because the money goes to the market, it doesn’t go towards improving the world. So, we absolve ourselves of these responsibilities. This was the criticism of ESG mentioned by Tariq Fancy (Ex-BlackRock Global Head of Sustainable Investing). He makes some very fair points, but my rejoinder would be that when shareholders engage with companies, they can make a positive difference.

Active owners have a duty to hold companies to account on their pledges. Maybe there's a role for an independent aggregator to be a ‘repository of promises’? The real issue is that companies are incentivised to lower their cost of capital in the short-term by making these types of promises and assertions. Yet the average age of a US CEO is 54 years of age, and if you're talking about net-zero and 2050 commitments, well they'll be in their 80s by 2050. Therefore, being held to account for meeting climate targets is not even your successor’s problem. There's an accountability-gap. It’s up to engaged shareholders to ask for those milestones and detailed plans so that they can have confidence to hold companies to account on their CEO statements.