Interviews

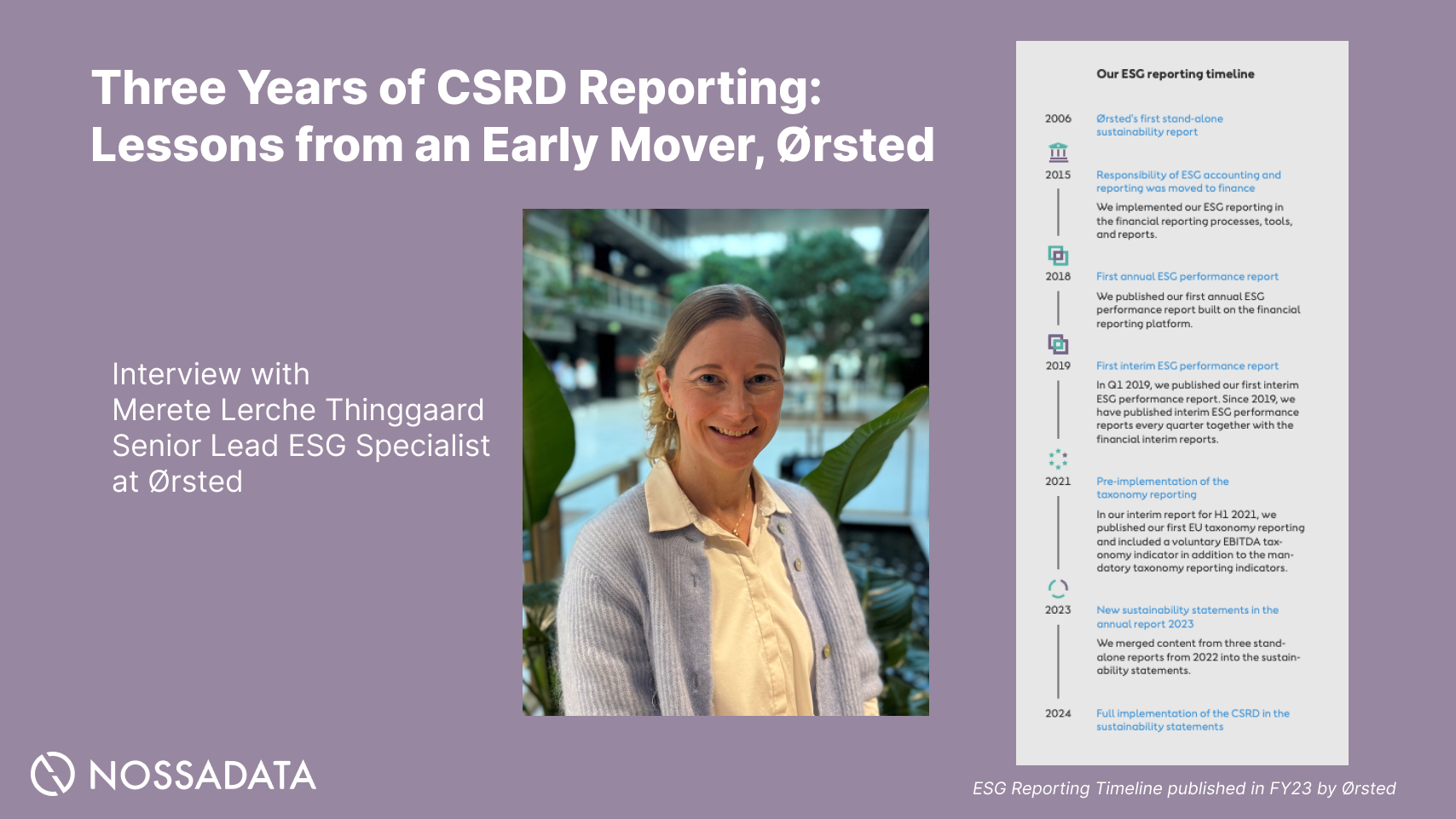

Three Years of CSRD Reporting: Lessons from an Early Mover, Ørsted

An expert interview with Merete Lerche Thinggaard, Senior Lead ESG Specialist at Ørsted, on three CSRD reporting cycles.

With the majority of FY 2024 CSRD reports on the market, I decided to have a look at what the Big 4 Audit firms have been saying. I have previously analyzed CSRD reports from each of the audit firms. In light of the Omnibus, we do expect there to be a significant amount of revisions in the regulation (CSRD revision timelines available here). This article will look at what each of the Big 4 firms are saying around CSRD.

All 4 firms have already published an analysis of FY 24 CSRD.

EY: Published the EU CSRD Barometer 2025

KPMG: Published the Real-time ESRS Fast 50

Deloitte: I found region publication from Finland and Denmark

PwC: Published Insights from the first 100 CSRD reports

The below article dives into key learnings from each of these ESG reports.

Want to work with Nossa Data on your CSRD Disclosure? Get in touch to learn how we streamline ESG reporting for listed corporates.

Average Length of a Sustainability Statement: All of the reports commented on length with different figures depending on the batch of company reports they assessed. Overall it seemed that the average length of a Sustainability Statement was 70-80 pages total. Sectors with the highest average number of pages are Financial Services, 147 pages, Infrastructure, 139 pages, Transportation, 125 pages.

What topic standards were chosen: Nearly all companies (above 95%) chose E1, S1 and G1. The next most commonly chosen topic standards were S2: Workers in the Value Chain and E5: Resource use and circular economy.

Number of IROs that companies pick: Multiple of the analysis commented that there was a very wide spread overall in the number of IROs chosen. Around 30 appears to be average and it is noted by PwC that: “Clear tables laying out material topics, sub-topics and associated IROs are supremely helpful for readers.”

Location of the Sustainability Statement: Nearly ALL companies assessed include dthe sustainability statement either as part of the management report or outside the management report (but still inside the annual report). EY notes: “In the future, we can expect to find the sustainability statements in the management report (as required by the accounting directive)”

Level of Assurance: Most companies stuck to limited assurance however a small number of companies chose to do reasonable or a hybrid approach (e.g. where some of their data was under reasonable assurance and some was not)

Structure of the Statement: The vast majority follow ESRS 1 Appendix F structure. Example image provided by EFRAG below of this appendix.

EY Shares the Length of Topical Standards within the Sustainability Statement:

EY shares use of phased in requirements by sector

EY offers an analysis of phased in S1 disclosure requirements that were allowed to be omitted

KPMG shows a spread of number of IROs chosen

KPMG also showcases stakeholder involvement with IROs in regards to providing input

Deloitte offers insight into use of other ESG ratings providers

Deloitte also shows where ESG is used in boards and related policies

Deloitte breaks down the ESG topics mentioned in disclosure

Want to work with Nossa Data on your CSRD Disclosure? Get in touch to learn how we streamline ESG reporting for listed corporates.