Interviews

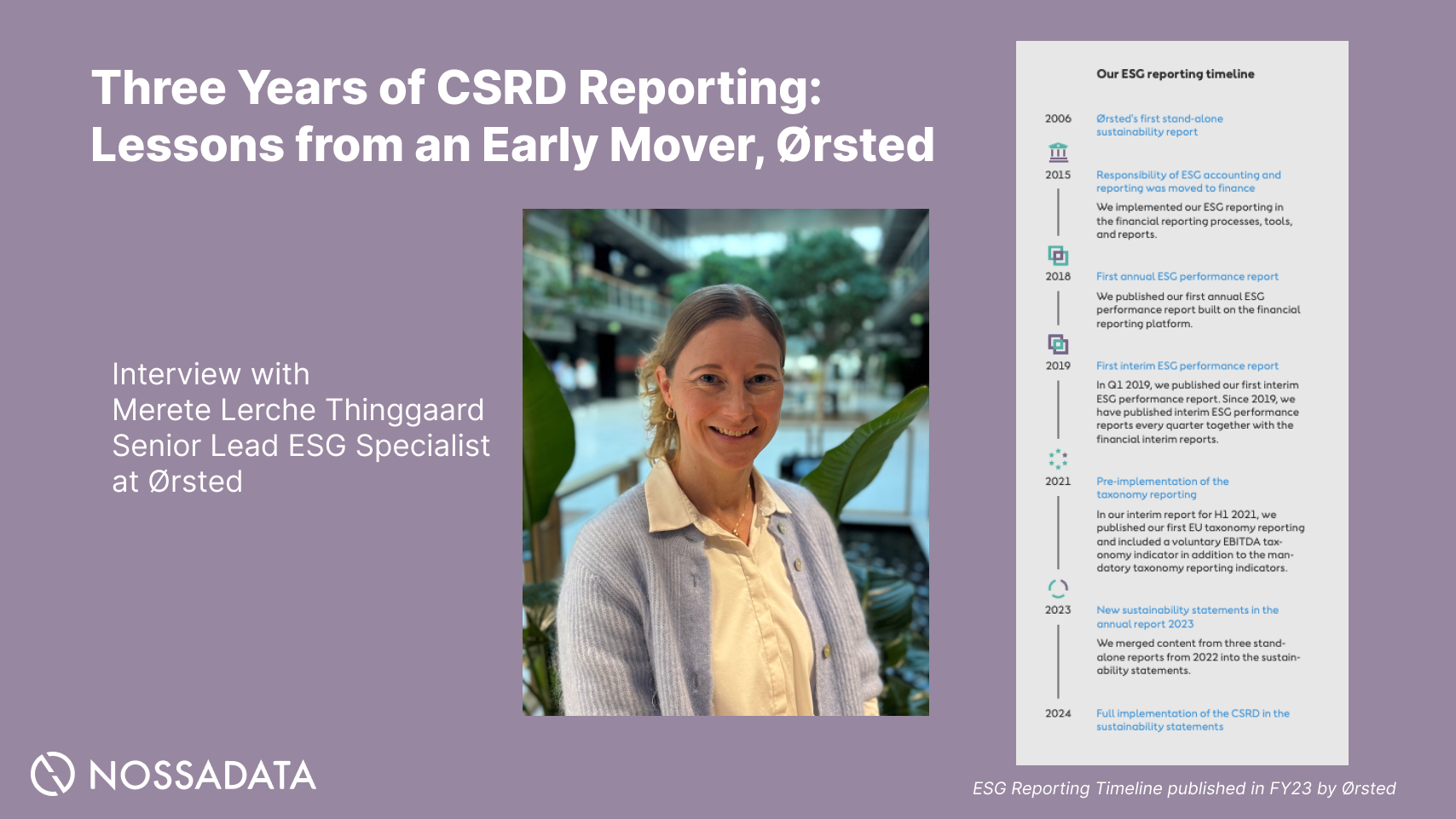

Three Years of CSRD Reporting: Lessons from an Early Mover, Ørsted

An expert interview with Merete Lerche Thinggaard, Senior Lead ESG Specialist at Ørsted, on three CSRD reporting cycles.

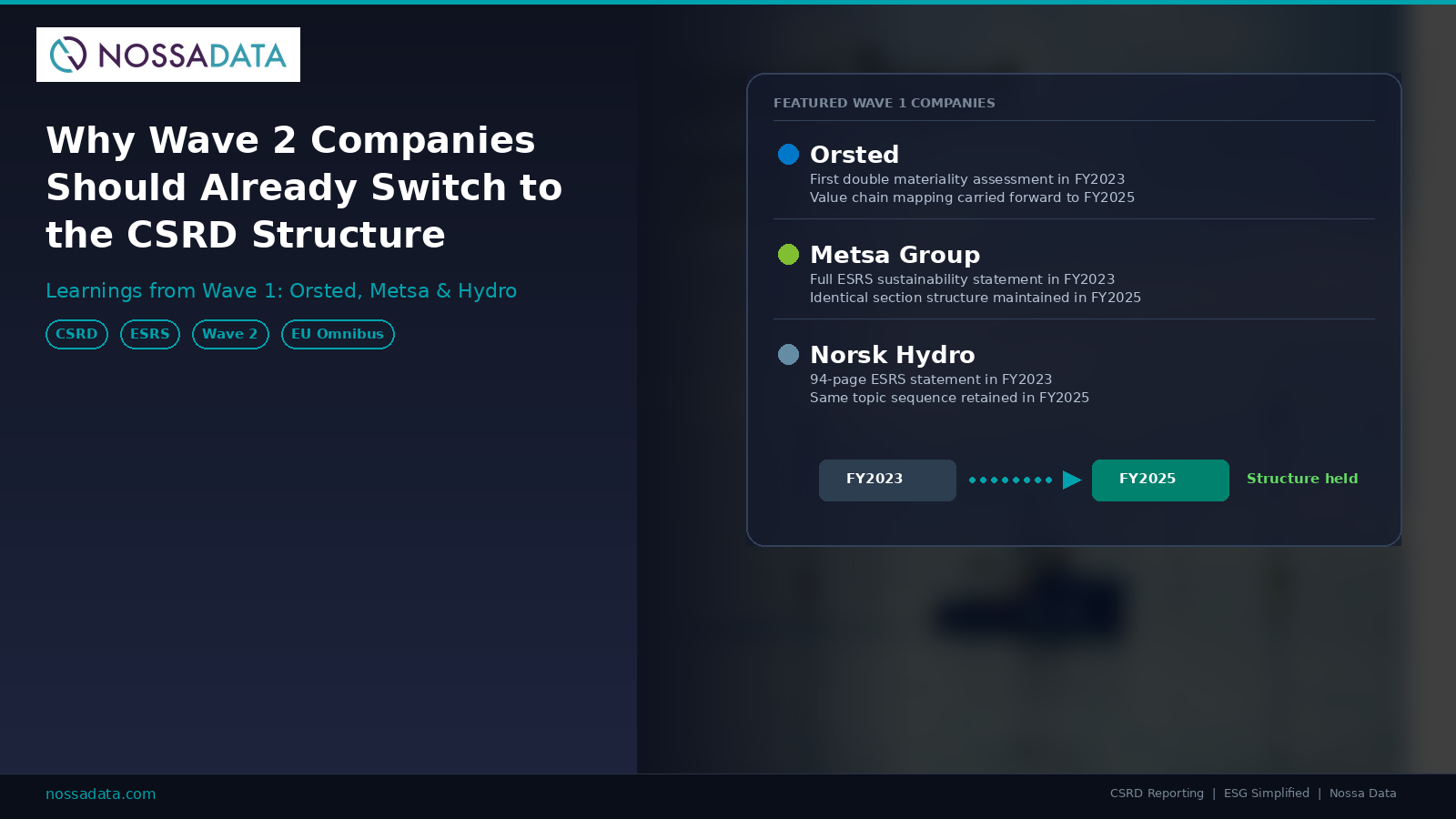

As Wave 2 companies are publishing their FY2025 sustainability reports under the CSRD, attention is shifting to what comes next for sustainability reporting. This article is for Wave 2 companies planning their reporting approach ahead of the FY2027 omnibus deadline.

We recommend, rather than starting from scratch, there is a wealth of practical insight to draw from companies that have already made the transition during FY2023 to FY2024 and FY2025. We examine how Ørsted, Metsä Group, and Norsk Hydro began structuring their sustainability disclosures to the ESRS framework as early as FY2023 — a full year before CSRD compliance was required. In this article we will show you side-by-side comparisons of their FY2023 and FY2025 reports to highlight that the structures they put in place before CSRD compliance held. For Wave 2 companies weighing whether to act now or wait, the evidence from Wave 1 is clear: start early, and the work compounds in your favour.

Omnibus already delayed progress for issuers

The EU Omnibus package, granted Wave 2 companies a two-year reprieve. Reporting obligations originally set for FY2025 have shifted to FY2027, with the European Commission expected to adopt simplified ESRS by mid-2026. New scope thresholds now require over 1,000 employees and €450 million in net turnover for EU entities.

Many Wave 2 companies have interpreted this as permission to pause. However, this article wants to dive into why companies that wait until 2027 will face the same data gaps and assurance bottlenecks that caught unprepared Wave 1 reporters off guard.

Nossa Data helps companies navigate the transition to CSRD-structured reporting. From benchmarking current disclosures against ESRS requirements to building end-to-end reporting frameworks, our platform accelerates your readiness. Contact us at nossadata.com.

What Wave 1 Leaders Proved in FY2023

The strongest Wave 1 reporters did not wait for their mandatory reporting year. During FY2023 — a full year before CSRD compliance was required — companies like Ørsted, Metsä Group, and Norsk Hydro had already begun restructuring their sustainability disclosures to mirror the ESRS framework. Their subsequent CSRD-compliant reports were stronger as a result.

Ørsted integrated sustainability reporting into its Annual Report for FY2023, conducting its first double materiality assessment and incorporating the fundamental structure of the ESRS a year ahead of the mandatory deadline. A cross-functional team led by ESG and Accounting Reporting in Finance ensured sustainability data was embedded alongside financial reporting from the outset.

Metsä Group took a similar approach. Its FY2023 Annual Review included a full sustainability statement structured to ESRS requirements before the directive applied. CFO Vesa-Pekka Takala stated that the company "wanted to progress more quickly than required by the directive." Metsä positioned itself as a leader in assured sustainability reporting a year ahead of schedule (source).

Norsk Hydro published a 94-page ESRS sustainability statement within its FY2023 Integrated Annual Report. The report addressed nine material ESRS topics, from climate change and biodiversity to workforce and community impacts.

FY2023 Reporting Foundations Carried Through to FY2025

The ESRS structures these companies adopted early helped them when it came to their first and second year CSRD reporting. Comparing their FY2025 reports with their FY2023 originals reveals remarkable continuity — the same section architecture, topic ordering, and disclosure logic carried forward.

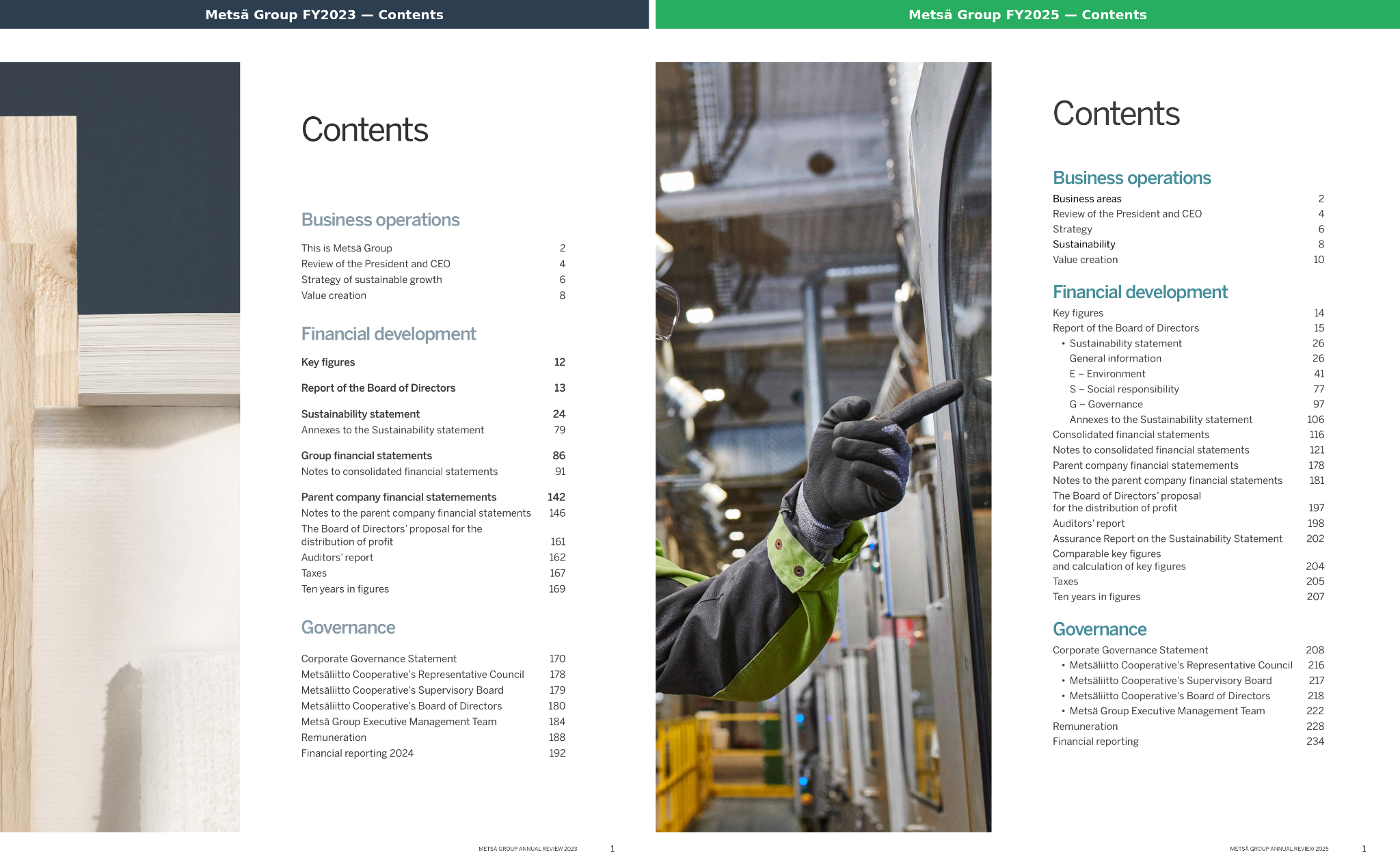

Example 1 — Metsä Group: Identical sustainability statement structure from FY2023 to FY2025. Both reports organise their sustainability statement under the same ESRS headings: General disclosures (p.24/26), E – Environment (p.41), S – Social responsibility (p.77), and G – Governance (p.97), with Annexes at p.79/106. The table of contents comparison below shows this continuity clearly:

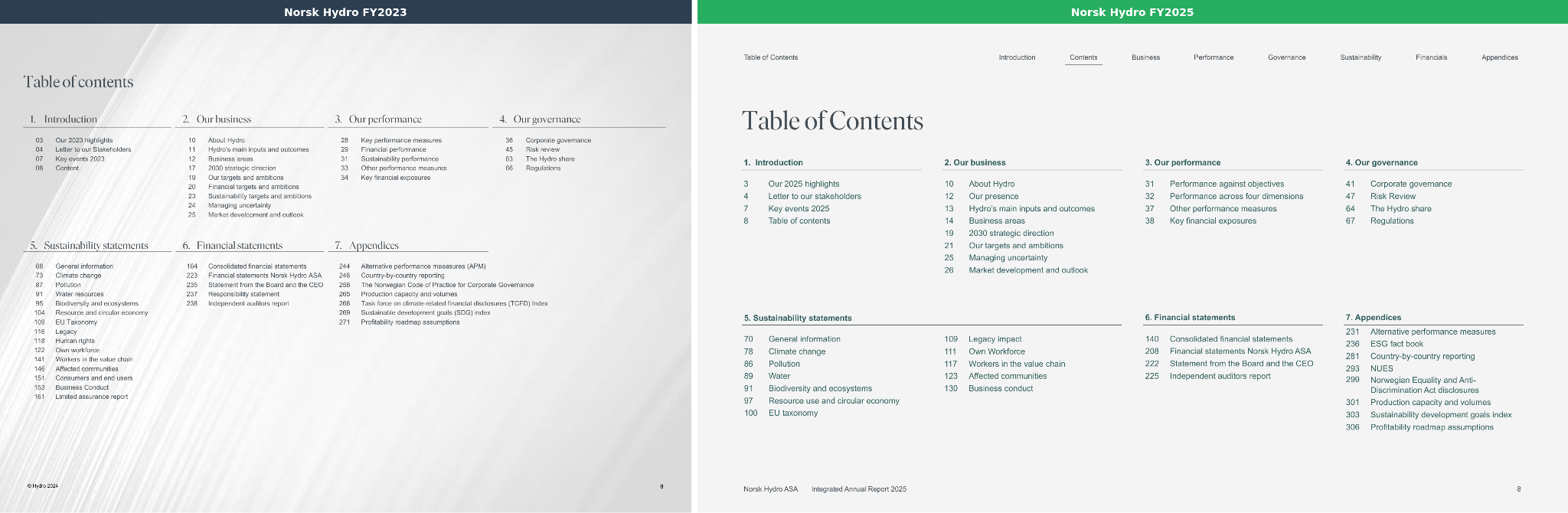

Example 2 — Norsk Hydro: Consistent ESRS topic architecture from FY2023 to FY2025. Hydro's FY2025 Integrated Annual Report retains the same sustainability statement structure established in FY2023. Both reports follow an identical sequence: General information, Climate change, Pollution, Water, Biodiversity and ecosystems, Resource use and circular economy, EU Taxonomy, Legacy, Human rights, Own workforce, Workers in the value chain, Affected communities, and Business conduct.

Example 3 — Ørsted: Value chain mapping carried forward from FY2023 to FY2025. One of the most compelling examples of structural continuity sits within Ørsted's sustainability statements. In its FY2023 Annual Report (p.72), Ørsted published a detailed value chain overview mapping material sustainability impacts and risks across upstream, own operations, and downstream activities. The company's FY2025 Annual Report (p.57) retains the same visual framework, updated with its 2025 double materiality assessment identifying 31 material impacts, risks, and opportunities — but built on the structure established two years earlier.

Why you should report aligned to CSRD now?

Wave 2 companies should treat FY2026 reporting cycles as dry runs. Begin mapping disclosures to ESRS topics, conduct a double materiality assessment, and establish cross-functional reporting governance. The companies that performed best under CSRD were those that started early.

Nossa Data helps companies navigate the transition to CSRD-structured reporting. From benchmarking current disclosures against ESRS requirements to building end-to-end reporting frameworks, our platform accelerates your readiness. Contact us at nossadata.com.