Interviews

Three Years of CSRD Reporting: Lessons from an Early Mover, Ørsted

An expert interview with Merete Lerche Thinggaard, Senior Lead ESG Specialist at Ørsted, on three CSRD reporting cycles.

On June 11, 2026, the Science Based Targets initiative (SBTi) published Version 2.0 of its Corporate Net-Zero Standard - the most significant overhaul since the framework launched in 2021. SBTi calls it a “major revision”: 42% of the standard's sections are entirely new, and the remaining 58% have been modified. With more than 11,000 companies already holding validated targets, the changes will shape how corporate issuers set, deliver and report climate targets for the rest of the decade.

What is the change about?

Version 1 was largely about ambition - committing to science-aligned targets.

Version 2.0 is built as an action framework: a “navigation tool” meant to sit inside the business and connect climate targets to capital allocation, procurement and investment decisions made by boards, CFOs and operations teams. A key difference is that Version 2.0 runs on a best-efforts basis, explicitly recognising that companies do not control everything in their value chains.

The standard is final, but it does not take effect immediately. There is a deliberate transition window, and existing validated targets remain valid through their current cycle.

June 11, 2026: V2.0 published. The rules are final; supporting Methods & Pathways, Assurance and Claims documents follow.

Through end of 2027: Version 1.x stays open. Companies with commitments or renewals due in 2026-2027 are advised to keep using V1.3 and move to V2 next cycle.

February 1, 2027: V2.0 becomes effective for target validation.

From 2028: Companies with existing 2030 targets should start setting their next cycle (2030-2035) under V2.0 to allow implementation lead time.

2035: Ongoing emissions responsibility (carbon removals / climate contributions) shifts from voluntary to mandatory for the largest companies.

Renewal in 2026-2027: If your target commitment or renewal falls in 2026-2027, SBTi recommends staying on V1.3 for now and adopting V2.0 at your next cycle. SBTi also expects to publish a renewal policy that folds V2 elements into guidance for companies already in the system.

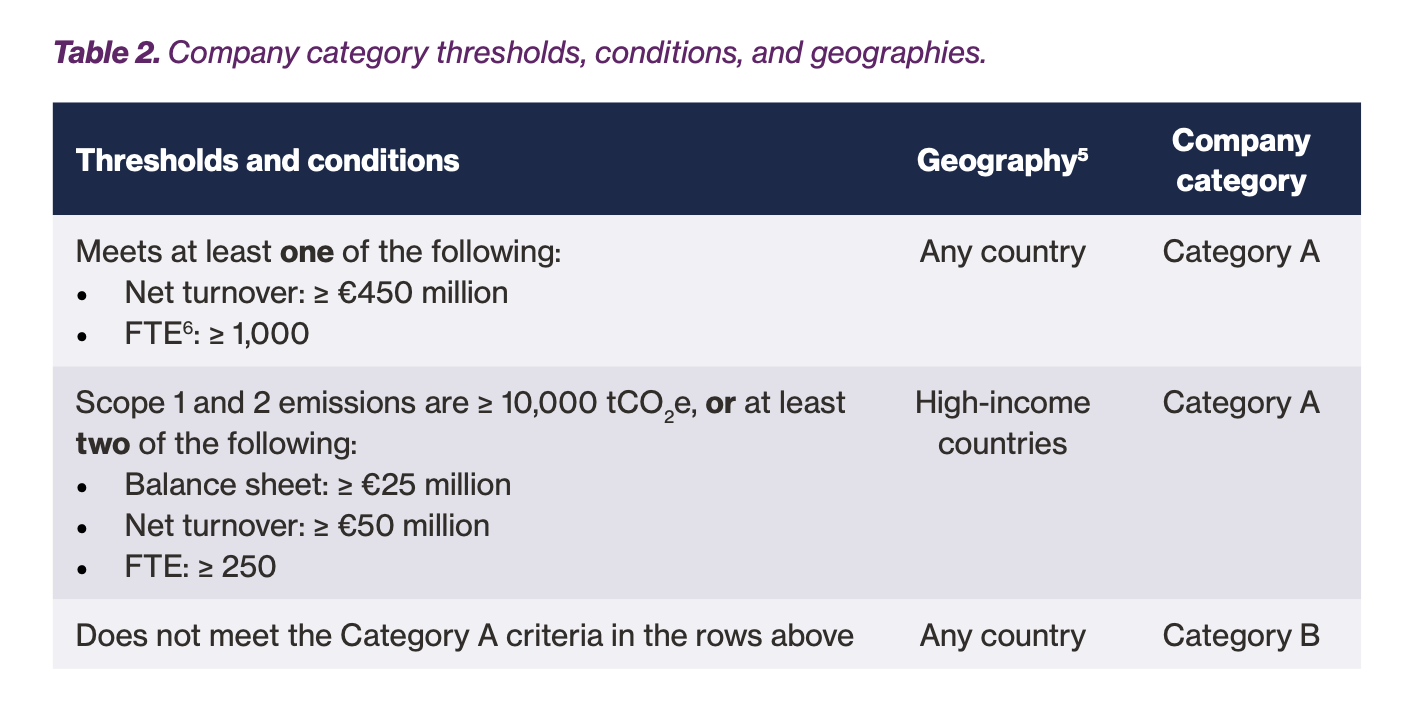

V2.0 introduces differentiated requirements based on size and country income level. Category A - large companies everywhere, plus medium-sized companies in high-income countries - faces the full set of requirements.

Category B - small companies everywhere and medium-sized companies in lower-income countries - gets relief on several obligations (transition plan disclosure, base-year assurance and scope 3 target setting become optional), though SBTi encourages them to go further. Subsidiaries operating as distinct businesses can be treated as separate companies.

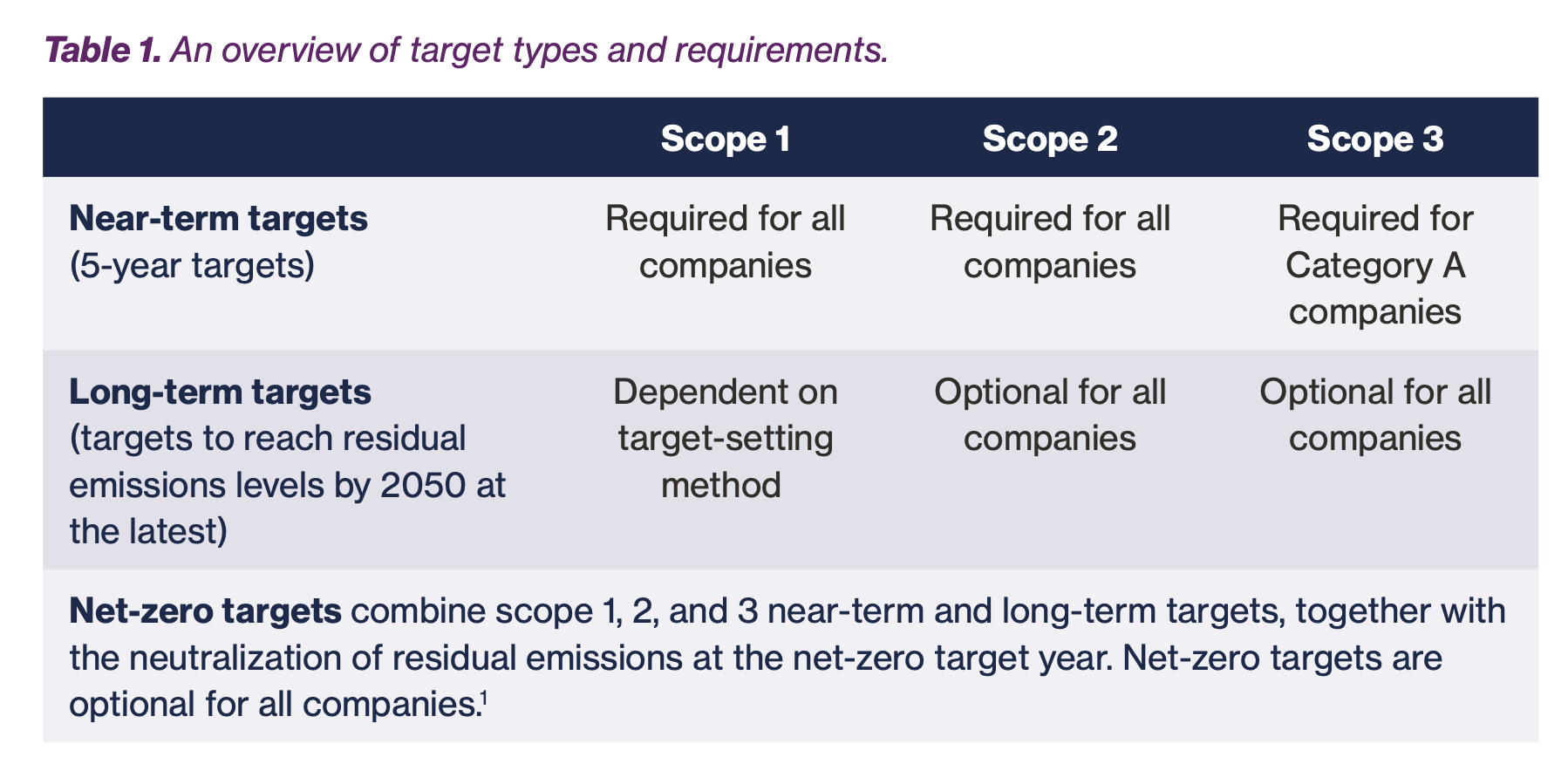

For example, the below table shows rules around targets for companies in Category A vs B.

If you would like to understand what category your company falls into SBTi also publishes the below information around the x2 categories of companies.

Companies no longer make a public net-zero commitment before setting targets. Instead, they must secure internal sign-off at the highest level of governance - the board or equivalent must formally assume accountability for setting, submitting and overseeing targets. SBTi made the change to remove a barrier to adoption and reduce the reputational and legal risk of announcing pledges before they are backed by plans.

Every company must now develop and maintain a transition plan covering the actions, timeframes, assumptions and dependencies behind its targets, formally approved by the board and aligned with corporate strategy.

Category A companies must publicly disclose that plan within 15 months of validation. SBTi validates that a compliant plan exists - a move toward board-level accountability and transparency.

V2.0 replaces the historical base year with a forward-looking “target base year” built on the most recent data, keeping targets aligned to net-zero pathways. Category A companies must obtain at least limited assurance of their base-year inventory (this is also recommended for Category B). Companies can still communicate progress against an earlier base year if they wish.

V1's combined scope 1+2 target is gone. Companies now set separate targets, with more flexibility:

• Scope 1 - three options: absolute reduction, sector emissions-intensity pathways (e.g. steel, cement, chemicals), or an asset-transition approach for capital-intensive businesses whose asset turnover is not linear.

• Scope 2 - two options: emissions-reduction targets, or increasing the share of low-carbon electricity (renewables, nuclear and CCS-fitted generation) over time, with optional long-term 100% targets.

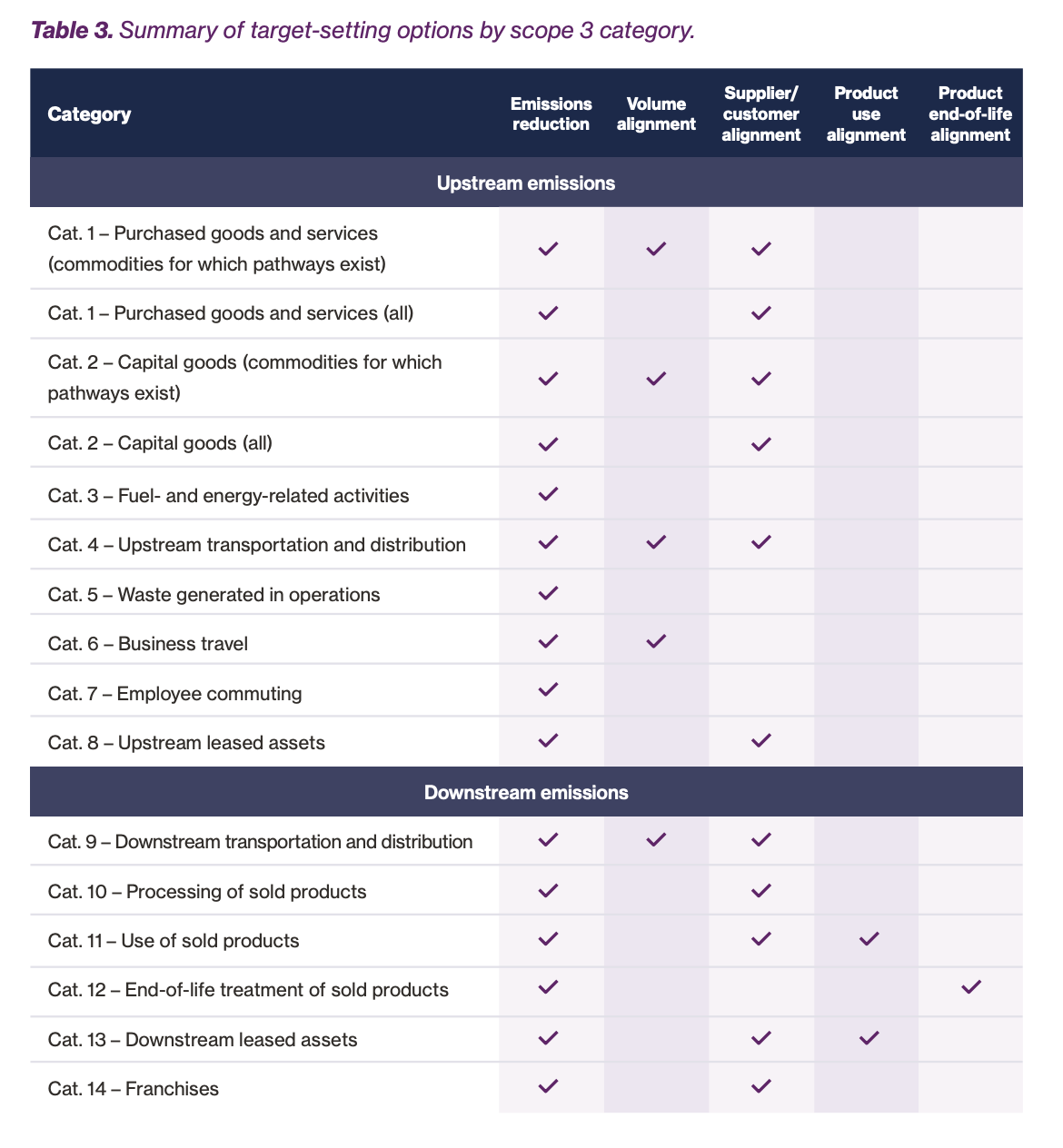

• Scope 3 - more flexibility: companies may make limited, justified exclusions (e.g. categories under 5% of scope 3) and choose between overarching reduction targets, supplier/customer alignment targets, or category/activity-specific targets. Scope 3 near-term targets are required for Category A.

Companies set two or more near-term (5-year) targets; an overarching net-zero target is optional. A new option also lets leaders earn SBTi recognition for hourly matching of electricity consumption with low-carbon supply.

To understand what types of targets you can set under Scope 3, the standard provides the below information to help Issuers understand what they can / cannot do.

V2.0 spells out how companies should cut emissions, in priority order: direct actions at source first; then actions within shared systems (“activity pools”) such as grids or supply sheds, which may use market instruments (energy and commodity certificates under mass-balance or book-and-claim models); and only then sector-level actions where structural constraints genuinely block progress. Market instruments must meet integrity criteria including additionality, and claims depend on whether the action actually reduces emissions in the company's own inventory.

Targets are pursued on a best-efforts basis: companies report annually, undergo periodic assurance, and face an end-of-cycle assessment. Falling short means steeper reductions in the next cycle, and minimum progress criteria will govern re-validation. Separately, the new Ongoing Emissions Responsibility program is voluntary for now - recognising companies that fund removals or other climate contributions as a complement to (not a substitute for) cutting their own emissions. From 2035 this becomes mandatory for the largest companies, reportedly requiring support for eligible carbon removals of at least 1% of ongoing emissions across scopes 1, 2 and 3, alongside neutralisation of residual emissions at net-zero.

• Check your timing. Map your current target cycle against the window above - decide whether to validate under V1.3 now or wait for V2.0.

• Confirm your category. Whether you are Category A or B determines which requirements are mandatory.

• Get governance ready. Brief the board now; internal sign-off and a board-approved transition plan are prerequisites, not afterthoughts.

• Strengthen your data. A latest-year inventory and limited assurance take lead time to put in place.

• Re-examine scope 2 and scope 3 strategy. The new options (asset transition, low-carbon electricity share, scope 3 exclusions) may change your most cost-effective path.

Nossa Data helps corporate issuers stay ahead of fast-moving sustainability standards like the SBTi Corporate Net-Zero Standard V2.0. Our platform centralises sustainability data, maps your disclosures against evolving framework requirements, and helps sustainability, finance and board teams build the governance and transition-planning evidence these standards now demand. Talk to our team to learn more about how Nossa Data’s software can help you.