ESG Insights

World’s Most Sustainable Companies 2026: Who Leads TIME’s Ranking and How It’s Scored

Overview of TIME 100 list and the companies that made the list in 2025 and 2026

An expert interview with Merete Lerche Thinggaard, Senior Lead ESG Specialist at Ørsted, on three CSRD reporting cycles, from disclosing voluntary under the draft ESRS standards in FY2023 to FY2025 .

Merete Lerche Thinggaard works in Group Finance with ESG at Ørsted, a Danish energy company and global leader in offshore wind, where she is responsible for CSRD compliance. Her team sits under the CFO, and she came to the role from a financial and audit background.

Ørsted is one of very few companies to have completed three consecutive cycles of CSRD-aligned disclosure: a voluntary report under draft standards in 2023, their first fully compliant report in 2024, and a follow-on report in 2025.

We spoke with Merete about the benefits of front-loading the work with voluntary disclosure, why the report evolved in size, how to work with auditors, and what she would tell Wave 2 and Wave 3 companies just getting started.

“[When speaking internally] This should not be sold as a compliance exercise. The primary argument is that it improves governance and gives you more robust data — frame it around business value.”

Want to visit the last 3 years of Ørsted’s reporting? See FY2023, FY2024 and FY2025.

Q Can you introduce yourself and your background?

I have a financial background and my first job was with one of the Big Four audit firms. I've worked across a range of projects and functions since then. Today I'm in ESG Reporting and Accounting, where I'm responsible for CSRD compliance and related work.

Q How did you get involved with CSRD, and what were the first steps?

I joined the team in 2022, just as it was starting to prepare for the new disclosures focused on project managing that work. A real benefit was that our management supported the new disclosures very early — before they were even transposed into legislation. In 2022 we defined six workstreams to prepare for CSRD, including a comprehensive mapping of our existing ESG metrics against the future requirements of the ESRS.

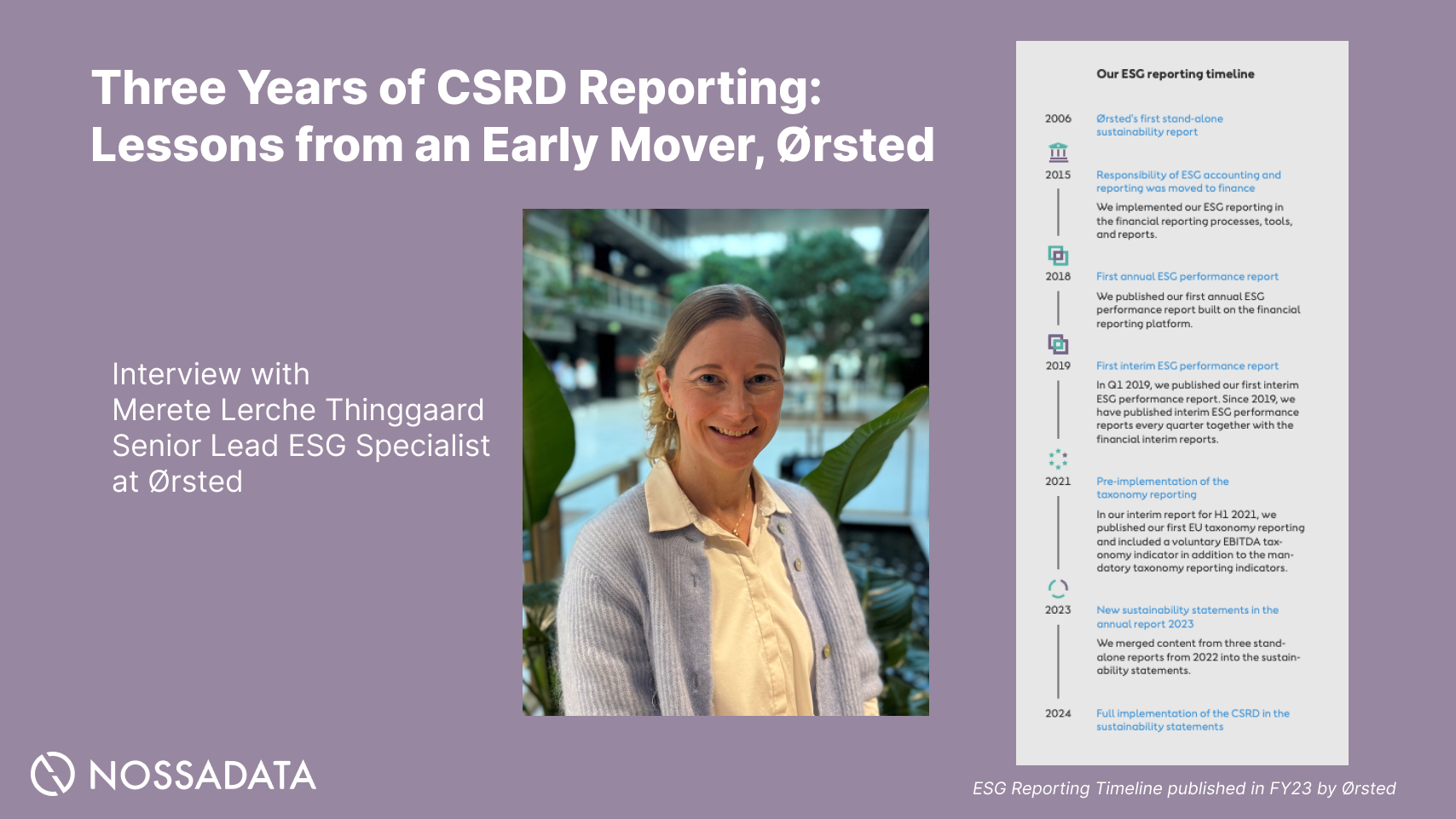

Prior to CSRD - our existing ESG reporting processes were a major advantage. We already had a robust setup for collecting and controlling ESG data on a voluntary basis through our ESG performance report (See their FY2022 report). Ørsted published its first standalone ESG performance report back in 2018, for financial year 2017. Because we started getting limited assurance so early, we were almost there when it came to preparing for limited assurance under CSRD. In our 2023 annual report we published a visual of our ESG reporting timeline showing that we've actually been on this journey since 2015. That head start is why we could move so quickly on the ESRS standards, a lot was already in place.

Q 2023 was voluntary, under draft standards. What was that first year like?

It was exciting to work with draft standards across the teams and figure out how our three existing reporting products could be combined. Before, we had the standalone ESG performance report; a sustainability report where we presented our sustainability programmes and ambitions across environment, social and governance; and our financial accounts. That first year was about working out how to bring everything together.

I learned that this is fundamentally a cross-functional, team effort, from the workstreams and the double materiality assessment workshops to drafting the narrative, you activate a lot of teams. That also spreads the word and educates people about why we're doing this. So in 2023 a lot of it was about education and getting everyone on board, explaining that we're doing this to strengthen sustainability governance and management, and that we very much welcome more balanced, transparent and consistent disclosures.

“This is a cross-functional and team effort. You activate a lot of teams, and therefore you also spread the word and educate why we are doing all of this.”

Q 2024 was your first mandatory, fully compliant report. What changed?

Front-loading in 2023 turned out to be a very good decision. We'd already made a lot of decisions on the fundamental structure of the report, and we got a lot of recognition for that. We took some decisions that weren't compliant in 2023, but the aim was not to obtain the auditors’ assurance a year ahead, but they referred to our report as good inspiration, and we were recognised among both Danish and non-Danish peers.

In 2024 the challenge was that we now had to comply with every single data point stemming from the double materiality assessment which triggered a very long list. Our report grew from 75 pages in 2023 to 100 pages in 2024. Some of those data points felt very theoretical, and we'd effectively skipped them the year before because we didn't see that they added anything decision-useful. Some of that information, including negative statements we'd never have written before, now had to be included.

We got feedback, internally and higher up, that it was hard to find the key messages. People asked where the executive summary was, said the structure felt very rigid, and pointed to duplications.

Q Then came 2025, with the Omnibus discussions underway. How did that play out?

It did have an impact. Management again told us the report was simply too long, 100 pages was far too much, and we needed to reduce significantly. So I had compliance on one side and our highest decision-making body on the other, and had to find where the two could meet. We defined four or five levers to bring the length down.

We aimed for a 25% reduction and ended up at 40%. We scrapped all the pictures, combined tables, tightened the spacing, put the policies for the social indicators onto a single page, and cut duplication. We also revisited those very theoretical negative statements checking whether they were still in the amended draft, and they weren't so we could remove some of those data points while staying compliant. That brought the 2025 report down to 60 pages. It's still a lot, but against the EFRAG ‘state of the play’ comparison it's actually below the average in the utility sector, and we're proud that we managed to cut it that significantly.

“We had an ambition of reducing the report by 25%. We actually ended at 40%.”

Q What have you learned from working with the auditors?

It's been a good learning curve on both sides — the auditors are learning, we are learning, and we've shared a lot of good experiences. Sometimes you can see that the standard is being applied for the first time but you should also apply common sense. Fair presentation, for instance, now makes so much sense in the amended draft.

The option for flexibility in the structure is something we'd already done in 2023 but weren't allowed to in 2024. We reintroduced a slightly different structure in 2025 because we could see it would probably be in the new standard. We brought back the appendix and moved the less prominent information down there.

Q Any advice on managing the audit relationship internally?

What really helped was mirroring what the financial teams have done for decades reporting under IFRS. Talking to the financial teams and the financial audit teams helped us apply more common sense and zoom in on what's most decision-useful. Use your internal stakeholders and draw on the experience other teams have already built. For example, we made a list of the data points we thought weren't relevant or decision-useful. Having that very specific, in a list, helped us have the compliance conversations with the auditors with good arguments.

“Use your internal stakeholders and draw on the experience other teams have already built.”

Q What about documentation and evidence for the auditors?

It's a very good exercise to make sure that whatever you put in the report, you also gather the documentation for. The minimum disclosure requirements for actions, for example. Even if you only use them as your own checkmark before the auditors ever look, it prompts very good questions to the input providers: Have you thought about the scope and the time horizon? What's the expected outcome? Is this a key action, or something you're just doing on an ongoing basis? It actually helped us produce a crisper report.

Q You put a lot of emphasis on value chain mapping. Can you share more?

We wanted to show where the results from our double materiality assessment actually sit, because it makes clear where our actions are focused. You can't necessarily manage everything, so it's also about acknowledging that you have impacts and risks outside your own operations, where you have less control. In the 2023 visual we only included top layer of the DMA results, we had around 30 impacts, risks and opportunities and couldn't fit them all in. It's a very good tool for showing where your IROs are concentrated and brings the report alive. We developed it year on year, and last year we put all of the IROs into the visual. It's quite busy, but if you know what you're looking for, it's a good way to show everything on a single page.

Q What are you most proud of in your FY2025 report?

The at-a-glance pages we introduced as a separate first section. That sits outside the mandated structure, but we added at-a-glance pages with an executive summary, because we learned from feedback — and from talking to peers — that some readers only have ten minutes to get a high-level overview. Those pages serve that need, and if you're specifically interested in one IRO you can still flip through the report to find it. I actually think we'll see more companies introducing these executive summaries, because a lot of people don't have time for a 100-page read.

“A lot of people don't have time for a 100-page read.”

Q What advice would you give Wave 2 and Wave 3 companies preparing their first reports?

Starting early is what helped us get to where we are and it's how we secured management buy-in. Tell them why CSRD is actually needed: it should not be sold as a compliance exercise — that shouldn't be the key argument. The primary argument is that it catalyses development of a more systematic way of working with sustainability internally including improved governance. Frame it around business value: you'll get a more robust report, you'll enhance investor confidence, and you'll be better prepared for the questionnaires that come up when you're seeking funding from your banks. Then start early, and you can mature along the way.

“It should not be sold as a compliance exercise. Frame it in a way where you get the business value out of it.”

Q Any final advice?

Talk with your networks. It helps a lot to share, because reading the standards paragraph by paragraph can get very theoretical, and digesting it with peers face-to-face aids understanding. We've found it valuable to combine desktop comparison with meeting people in person — sometimes you pick up new information in a face-to-face conversation that you simply can't read in the reports.