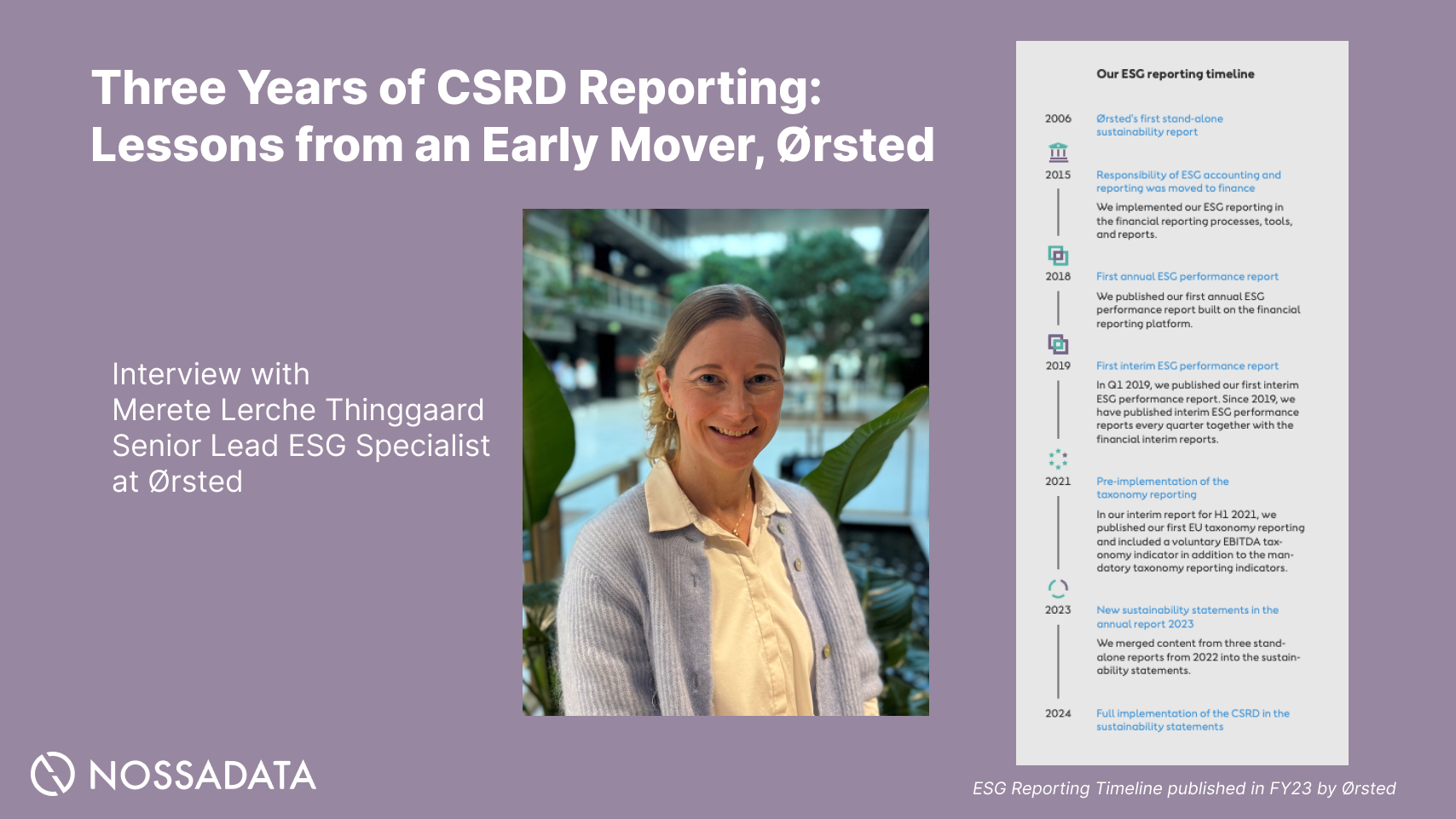

Interviews

Three Years of CSRD Reporting: Lessons from an Early Mover, Ørsted

An expert interview with Merete Lerche Thinggaard, Senior Lead ESG Specialist at Ørsted, on three CSRD reporting cycles.

If you report corporate emissions, you are almost certainly using the GHG Protocol, similar to the 97% of companies in the S&P 500 that used the standard in 2023. For about twenty-five years those GHG Protocol standards changed slowly. In 2026 they are changing fast (from a standard setters perspective).

This year the Protocol has open consultations covering Scope 2, Scope 3 and carbon credits as well as a new standard for land and carbon removals. If you work with emissions data, it is worth getting your head around these now. On top of that, they have had changes to how the organisation is governed overall. This piece walks through what the GHG Protocol is and what is actually changing.

The Greenhouse Gas Protocol is the most widely used framework in the world for measuring and managing greenhouse gas emissions. It gives companies, cities and governments a common set of rules for working out how much they emit, where those emissions come from, and how to report them. It is run as a partnership between the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD).

It started with a fairly simple problem. By the late 1990s plenty of companies wanted to measure their emissions, but there was no agreed way to do it, so no two inventories were really comparable. In 1998 WRI, working with companies including BP and General Motors, published a report called Safe Climate, Sound Business that argued for a standardised way to measure emissions. WRI and WBCSD pulled together a group of environmental organisations and large industrial firms to hammer out the details, and in 2001 they published the first edition of the Corporate Standard.

That standard is the reason the language of "scopes" exists. Scope 1 covers emissions a company makes directly, from its own facilities and vehicles. Scope 2 covers the emissions tied to the energy it buys, mostly electricity. Scope 3 covers everything else across the value chain, from the goods a company purchases to what happens when customers use and eventually throw away the products it sells. Over the following decade the Protocol filled in the details with dedicated guidance for Scope 2 and Scope 3, plus calculation tools to go with it.

Almost everyone now leans on the result. The Corporate Standard sits under effectively every corporate GHG reporting programme going, and around 97% of disclosing S&P 500 companies use it for their inventories. CDP, the Science Based Targets initiative, the ISSB and most mandatory disclosure regimes are all built on GHG Protocol accounting. When a regulator asks for Scope 1, 2 and 3 figures, that is the Protocol's language.

Before the standards content changed, the governance of the organisation changed. The GHG Protocol established an independent Independent Standards Board (ISB), to oversee a formal Standard Development and Revision Procedure. With that board, expert Technical Working Groups draft proposals; the ISB reviews and approves them; and the public is consulted along the way. In Q1 2026, ISO technical experts joined the working groups, and partner “Observing Entities” were added to keep frameworks built on the GHG Protocol aligned.

In addition to this, on 28 April 2026 the GHG Protocol named Tim Mohin as its first ever chief executive, starting on 1 June. The new CEO Tim Mohin is a strong choice as he used to run the Global Reporting Initiative (GRI), held sustainability roles at Intel, Apple and AMD, worked at the US Environmental Protection Agency and in the US Senate, and most recently led climate and sustainability work as a partner at Boston Consulting Group. He has called the job "the most important climate infrastructure job in the world."

On top of this, the COP30 Presidency has asked the GHG Protocol and ISO to lead a global push to harmonise greenhouse gas accounting through the COP Action Agenda, with a deadline tied to the 2028 Global Stocktake. The two have been told to take the current tangle of overlapping accounting methods and pull it toward one science-aligned system. For any company reporting across several countries and frameworks, this sits behind everything else happening this year, and it is the clearest sign that things are heading toward fewer, more aligned rules.

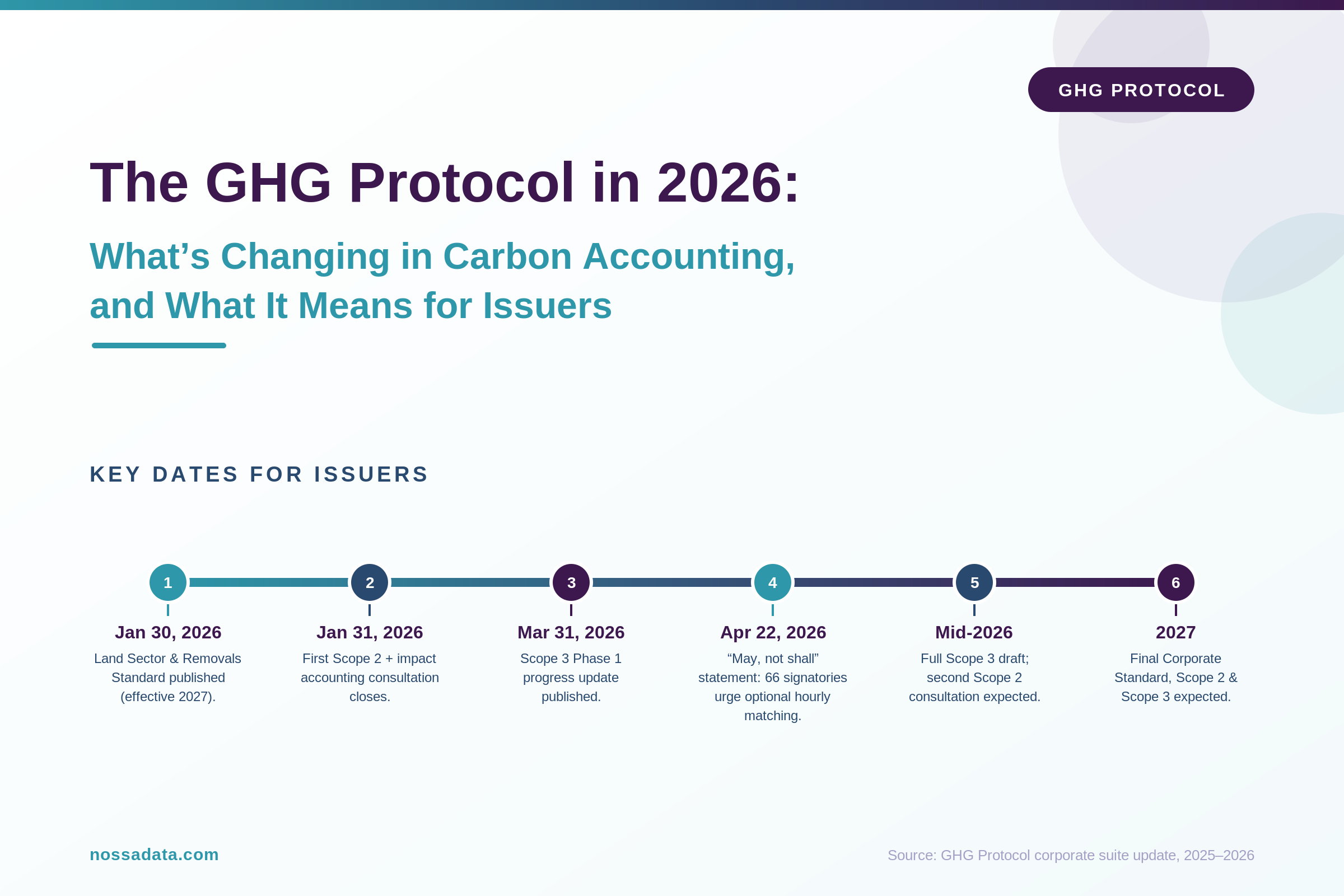

Jan 30, 2026: Land Sector and Removals Standard published — the first finished piece of the update (effective Jan 1, 2027).

Jan 31, 2026: First public consultation closes on the Scope 2 update and electricity-sector consequential accounting (open since Oct 20, 2025).

Q1 2026: ISO technical experts join the Corporate Standard, Scope 2, Scope 3 and Actions & Market Instruments working groups.

Mar 31, 2026: Scope 3 Phase 1 progress update published by a 65-member working group.

April 22, 2026: Public response to the standard requesting “May” not “Shall”

Mid-2026: Full Scope 3 consultation draft expected; a second Scope 2 consultation to follow.

2027: Final revised Corporate Standard, Scope 2 and Scope 3 expected (Scope 2 no sooner than end of 2027); Land Sector Standard takes effect.

The corporate suite update is being delivered through four parallel Technical Working Groups:

• Corporate Standard. Working through base-year recalculations, how companies consolidate emissions across group structures, data quality, which gases must be reported, and which global warming potential values to use.

• Scope 2. A 60-day public consultation on revising the 2015 Scope 2 Guidance, plus a parallel one on consequential methods for electricity-sector actions, drew almost 1,400 responses now being worked through. Anything that changes market-based versus location-based accounting lands directly in most companies' reported numbers.

• Scope 3. After settling boundary-setting questions across the categories, the group has moved on to processing of sold products (category 10), use of sold products (category 11), and is turning to circularity. These are some of the trickiest categories to measure, so the outcomes will matter for manufacturers and consumer brands in particular.

• Actions and Market Instruments (AMI). A Phase 1 White Paper went out for a 60-day Request for Information from 31 March to 31 May 2026. It proposes a multi-statement reporting framework that would add three new statements alongside the physical inventory, a real rethink of how carbon credits and mitigation actions get reported. This is not yet a draft standard; a formal public consultation on one is planned for the third quarter of 2027.

Separately, the Land Sector and Removals Standard - the first finished piece of the broader effort - was published on January 30, 2026 and takes effect January 1, 2027. It gives companies the first GHG Protocol methods to account for land emissions and CO₂ removals, a growing concern for food, agriculture and forestry-exposed value chains. Some aspects of this standard have already been incorporated into the 2026 CDP questionnaire.

Take a look at the Scope 2 standard under consultation here.

The Scope 2 update is the change issuers will feel first. The proposal keeps the familiar dual location-based and market-based reporting methods, but adds a major new requirement for market-based reporting: hourly matching and regional deliverability. In practice, a clean-energy purchase would only count toward your scope 2 inventory if the electricity is generated in the same grid system and time period in which you consume it. Buying renewable energy certificates from a distant, unconnected region to claim “100% renewable” would no longer reduce your reported scope 2 total.

To capture the value of clean-energy actions that fall outside those tighter inventory boundaries, the GHG Protocol is developing a complementary, impact-based metric - Marginal Emissions Impact - reported separately from the inventory. The aim is to keep inventories comparable while still recognising purchases that genuinely displace fossil generation on dirtier grids. Recognising the data burden, the proposal includes feasibility measures: load profiles to approximate hourly data, exemption thresholds for smaller electricity users, a legacy clause for existing contracts, and a multi-year phased rollout. A first consultation ran from October 2025 to January 31, 2026; a second will follow in 2026, with final publication no sooner than the end of 2027.

The loudest of the current fights is over Scope 2. 66 companies representing over 33,500 organisations have requested the standard setter to follow a “May” instead of a “Shall” approach. See the list of signatories here: https://www.maynotshallscope2.com/

The Protocol's case for changing the rules is reasonable insofar that the Scope 2 Guidance dates from 2015 and has not had a serious update since. Grids have changed a lot in that time, the guidance has ended up baked into mandatory regimes like Europe's ESRS and the IFRS standards, and clean-energy claims are under far more scrutiny. The Protocol says it wants to fix three things:

The proposed revision keeps the basic shape, including the requirement to report under both the location-based and market-based methods, but tightens each. The location-based method gets a stricter emission-factor hierarchy that pushes companies toward the most precise data they can freely get hold of. The market-based method is where the trouble starts. The Protocol wants clean-power purchases matched to consumption hour by hour, drawn from generation that could actually reach the company's grid, with a fairer split of publicly funded "standard supply service" power and tighter residual-mix rules to stop double counting. The thrust of it is a move away from buying annual certificates across broad markets and toward matching the clean power you use to when and where you use it.

The Protocol knows this is a big ask, so it has added some cushions. Companies without hourly data can use load profiles to approximate it. Smaller reporters would be exempt from hourly matching altogether, and the Protocol's own analysis suggests most CDP-reporting companies would qualify for that exemption while most of the electricity on the grid would still be covered. There is a legacy clause for existing contracts, and a multi-year, phased rollout, with the revised standard not expected before late 2027.

On 22 April 2026 a coalition put out a public statement, now widely called the "may not shall" letter, asking the Independent Standards Board and Steering Committee to make hourly matching and strict deliverability optional, a "may," instead of a required "shall." The 66 signatories include Amazon, Apple, General Motors, BYD, Honda, FedEx, Mars, Salesforce, Patagonia, Corning and Schneider Electric, plus a string of clean-energy developers and trade bodies, and together they say they speak for more than 33,500 organisations and over 300 GW of carbon-free electricity. Their case is that the 2015 guidance helped bring on more than 250 GW of clean energy, and that forcing hourly, location-matched accounting would do little for accuracy while making voluntary procurement harder and more expensive, which would slow decarbonisation rather than help it. There is a real accounting point buried in the lobbying, too: many virtual power purchase agreements, which have driven a lot of new clean-energy build, would no longer count inside the Scope 2 inventory under the proposal, and would instead be reported separately as consequential impacts.

Mohin is right in the middle of this. He uses the row to make the point that standards matter: “The reason why all these stakeholders get so interested in standards is that they are truly global; they have impact across the world.” He still wants a single method. “You will need to select a common methodology,” he said. “That makes it a lot harder, but at the end of the day we need consistency and comparability, which will lead to decarbonization.” And the risk is real. The Science Based Targets initiative, which has more than 10,000 corporate members, has been reported as a possible breakaway over Scope 2. Mohin says he does not expect a split, because “that would add to fracturing, which is the opposite of what we want to do,” and he admits the Protocol has not always got these calls right: “Have we always got it right? Of course not. That's something we'll have to continuously improve as the organization matures.”

The Scope 3 Standard hasn't been updated since 2011, yet it now drives the majority of most companies' reported emissions and disclosure scrutiny. A 65-member working group spanning 20-plus countries published a Phase 1 progress update on March 31, 2026, working through thorny issues such as category boundary-setting, quantification for processing and use of sold products, and circularity. A full public consultation draft is expected mid-2026, with a final standard targeted for late 2027. Expect tighter expectations on data quality and methodology - the areas where most companies' scope 3 numbers are weakest today.

Two substantial pieces of standard-setting moved forward in 2026.

The first is the Land Sector and Removals Standard, published on 30 January 2026 (Read the standard here). It is the Protocol's first standard for accounting land emissions, land-use change and CO₂ removals, including biogenic products and technological removals such as direct air capture and CO₂ capture with geologic storage. It took five years and more than 300 external reviewers to produce, and it takes effect on 1 January 2027, with the companion Guidance due in the second quarter of 2026. Notably, forest carbon accounting was left out of this first version because experts could not yet agree on the science and feasibility; the Protocol plans to gather more input and run field tests before adding it. Companies in food, agriculture, forestry and consumer goods, or anyone counting removals, should be reading this one now.

The second is a joint product-level standard with ISO. In April 2026 the two organisations set up a Joint Working Group to build a single, harmonised standard for product-level carbon accounting, drawing on ISO 14067 and the existing GHG Protocol Product Standard. The appetite for it was clear: more than 450 applications came in, from over 410 organisations across more than 50 countries. It matters because carbon border measures such as the EU's Carbon Border Adjustment Mechanism rely on credible, comparable product-level data, and at the moment that data is patchy.

For sustainability and reporting teams, none of this is a single rule / is imminent. It is more a read on where things are heading, and a few of those directions are worth planning around now.

Start with convergence. Between the COP30 mandate and the tie-ups with ISO and the ISSB, the long-run trend is toward fewer, better-aligned methods, which should make life easier for anyone reporting across several regimes. While the standards are being actively rewritten, the ground keeps shifting, so it pays to follow the consultations rather than assume today's methods will hold.

Expect demand for value chain and product data to keep rising. The joint product standard and the ongoing Scope 3 work both push toward more granular, more comparable numbers, and carbon border measures add a hard commercial reason to produce them. Companies in trade-exposed and manufacturing sectors should be investing now in the data systems and supplier relationships that produce primary, product-specific figures, because rough industry averages will not carry the same weight for much longer.

Land and removals are moving into the mainstream inventory too. With the LSR Standard taking effect in January 2027, companies with land-related emissions, and anyone accounting for removals, finally have formal rules to follow. If that is you, a gap analysis against the new standard is a good use of the months before it bites, with one eye on the Guidance due later this year and on how forest carbon eventually gets handled.

The AMI work is worth watching closely if your climate strategy leans on credits or claims. The multi-statement idea is designed to keep a company's physical emissions separate from its use of market instruments and the impact of its actions, so offsets cannot simply be netted off against gross emissions out of sight. That is a deliberate response to greenwashing concerns, and it points to a future where credits and claims have to be reported far more transparently.

Behind all of this, the Protocol is turning into a more institutional body, and institutional bodies revise their rules more often. The days of rare, generational updates are ending. The sensible response is to treat carbon accounting as something that needs an owner: someone watching the GHG Protocol consultations, and a little budget set aside for the methodology changes that are now going to keep coming.

So the framework that standardised corporate carbon accounting over the last quarter-century is being rebuilt for a time when emissions data sits much closer to regulation, capital and strategy. For issuers, the moves that matter are not glamorous: stay close to the consultations, firm up your Scope 3 and product data, get ready for land and removals if it touches you, and assume the rules will keep changing. The body behind the numbers is taking on a much bigger role, and the numbers themselves are about to count for more.

Sources

Corporate Value Chain (Scope 3) Standard

Corporate Value Chain (Scope 3) Accounting and Reporting Standard (full PDF)

GHG Protocol appoints Tim Mohin as CEO (press release, 28 April 2026)

ISO and GHG Protocol finalize Joint Working Group on product-level standard (9 April 2026)

Upcoming Scope 2 Public Consultation: Overview of Revisions (GHG Protocol)

Public Statement on Scope 2 Guidance Revisions (“may not shall” letter)

WSJ: Climate Reporting Is Key to Decarbonization, Says New CEO of Greenhouse Gas Protocol

GHG Protocol Newsletter: March 2026