Interviews

Building Internal Controls for CSRD: Lessons from a Wave 1 Company

An interview with Seraphina Kim about applying internal controls for CSRD disclosure.

As of August 2025, the landscape for climate- and sustainability-related reporting under the IFRS Sustainability Disclosure Standards is evolving rapidly, with growing jurisdictional adoption and an expanding library of guidance and examples. IFRS S1 and IFRS S2 are increasingly serving as the global baseline for consistent, decision-useful disclosures, while national regulators adapt and align these requirements within their own legal frameworks.

This article explores the current state of IFRS-aligned disclosure, highlights which jurisdictions have formally adopted or integrated the standards, shows high-value educational materials and implementation resources, and reviews disclosure examples that can help preparers understand and apply best practices if their organisation adopts IFRS.

IFRS S2 is the International Financial Reporting Standards Sustainability Disclosure Standard focused on climate-related disclosures. Published by the International Sustainability Standards Board (ISSB) in 2023, it sets out specific requirements for companies to disclose information about their governance, strategy, risk management, and metrics and targets related to climate change. IFRS S2 builds on the framework of the Task Force on Climate-related Financial Disclosures (TCFD) and aims to ensure that investors and other stakeholders have consistent, comparable, and decision-useful information on how climate-related risks and opportunities could affect a company’s prospects. The standard is designed to be applied alongside IFRS S1, which establishes the general requirements for sustainability-related financial disclosures.

For companies, IFRS S2 is relevant whether they operate in high-emission industries or sectors less directly exposed to climate change, because it addresses both transition risks (e.g., policy changes, shifting market preferences) and physical risks (e.g., extreme weather events). Its applicability is broad: listed companies, entities seeking investment, or those in jurisdictions adopting ISSB standards may need to integrate IFRS S2 into their reporting processes. Even if not mandated, companies can adopt IFRS S2 voluntarily to enhance transparency, strengthen investor confidence, and align with global best practices. Implementing IFRS S2 may involve cross-departmental collaboration, robust data collection, and the integration of climate risk assessment into corporate strategy and financial planning.

At Nossa Data, we make IFRS-aligned sustainability reporting simple, streamlined, and stress-free. Our platform is built to help you navigate the complexity of IFRS S1 and S2 disclosure. We streamline data collection, build in alignments to other frameworks, and offer direct links to the latest ISSB guidance. From first-time reporters to seasoned sustainability teams, we provide the tools, templates, and real-world examples you need to confidently meet evolving regulatory requirements and showcase your ESG leadership. Interested in seeing a Demo of Nossa Data? Get in touch on our contact form.

Below, we have created a table that summarised IFRS requirements by jurisdiction and when the regulation is coming into effect. Note: The IFRS Website also keeps a jurisdiction tracker you can access here.

Australia

Australia has mandated climate reporting based on AASB S2 (aligned with IFRS S2) from periods beginning 1 Jan 2025, phasing in through 2027. IFRS+1

Brazil

Brazil’s CVM permits use of ISSB standards from 2024 and makes them mandatory for listed companies from 2026. IFRS, conteudo.cvm.gov.br

Malaysia

Malaysia requires listed issuers to provide climate-first disclosures in line with IFRS S2 from FYs beginning 1 Jan 2025 (Group 1), with broader ISSB adoption phased to 2027–2030. IFRS

Singapore

Singapore will mandate climate reporting aligned with ISSB for listed issuers from FY2025 and for large non-listed companies from FY2027. SGX Links, IFRS

Hong Kong SAR

HKEX’s enhanced climate disclosures—effective 1 Jan 2025—are aligned with IFRS S2, with a government roadmap targeting full ISSB adoption by 2028. HKEX, IFRS

United Kingdom

The UK has set a pathway to endorse UK Sustainability Reporting Standards aligned to ISSB, with consultation underway to finalize endorsement and implementation. GOV.UK, IFRS

Canada

Canada’s CSSB issued CSDSs (Dec 2024) aligned with ISSB; currently voluntary pending regulatory incorporation, with CSA pausing its climate rule in Apr 2025. IFRS

Japan

Japan’s SSBJ issued exposure drafts (29 Mar 2024) modeled on ISSB standards and consulted on making sustainability disclosure mandatory. SSB-J

Nigeria

Nigeria’s FRC issued a March 2024 roadmap adopting IFRS S1/S2, permitting application from 2024 and mandating for public-interest entities from 2028 (SMEs from 2030). IFRS

Switzerland

Switzerland consulted in 2024–2025 on moving from TCFD to allow companies to report using ISSB (or ESRS), with decisions expected in 2025. IFRS

Jordan

Jordan’s Amman Stock Exchange permits ISSB use from 2025 and mandates climate (IFRS S2) for ASE20 firms from 2026. IFRS, Ase

The June 2025 IFRS guidance on disclosing climate-related transition plans explains how entities can apply IFRS S2 to provide clear, comparable, and decision-useful information about their strategy for moving toward a lower-carbon and/or climate-resilient economy. Drawing on the UK Transition Plan Taskforce’s framework, the document does not impose new requirements but clarifies how existing IFRS S2 provisions—and related IFRS S1 principles on materiality, presentation, uncertainty, and comparatives—should be used to report material details of an entity’s climate strategy, risk and opportunity responses, and planned business model changes. While having a transition plan is not mandatory, any plan or related disclosures must be clearly identifiable, not obscured, and may be presented within financial reports or via cross-references, with jurisdictions free to add supplemental requirements without undermining core ISSB-aligned sustainability disclosures.

Issued in May 2025 by the IFRS Foundation, this document offers a clear, Q&A‑style breakdown of how entities should measure and disclose greenhouse gas (GHG) emissions under IFRS S2—without introducing new standards. Designed to clarify the existing GHG emissions disclosure requirements, it covers topics such as the mandate to report absolute gross emissions across Scopes 1, 2, and material Scope 3 categories; the prioritised use of the GHG Protocol for measurement (while noting that IFRS S2 prevails in case of conflicts); and the requirement to transparently disclose methodologies, assumptions, organizational boundaries, and financed emissions for financial institutions, supported by illustrative examples.

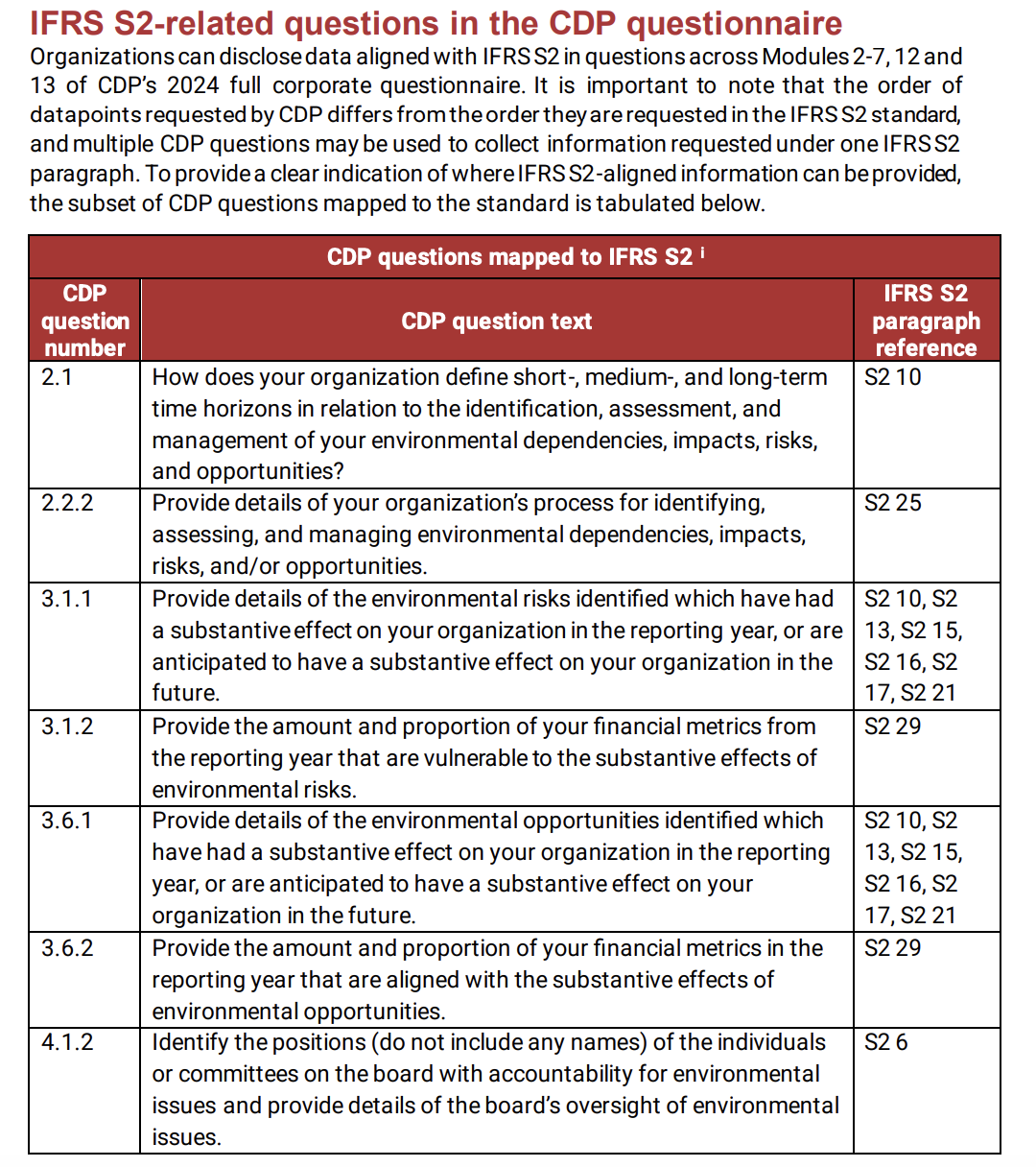

This document goes question code by question code and shows how IFRS aligns to CDP. See the example of how the disclosure breakdowns work.

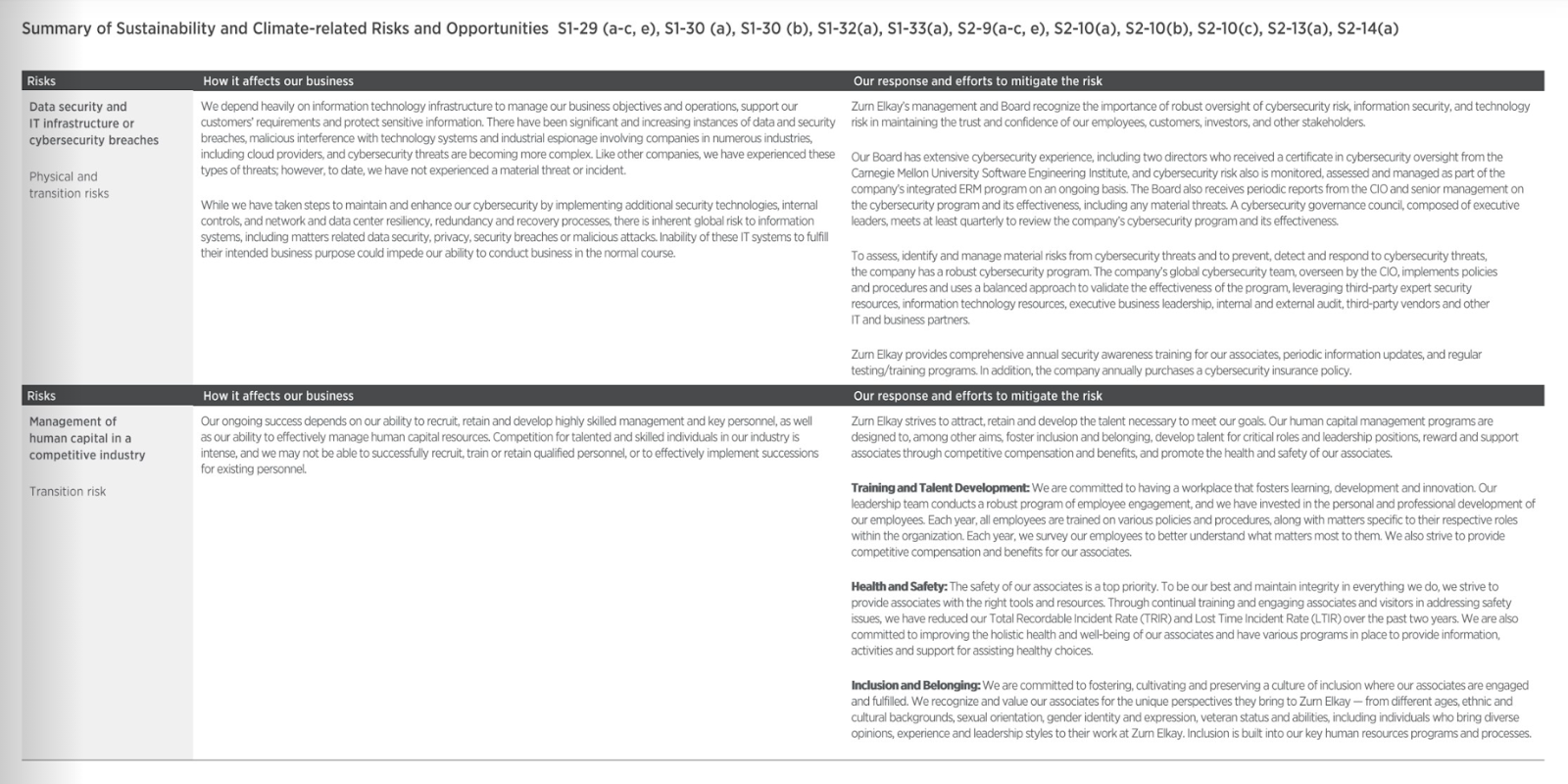

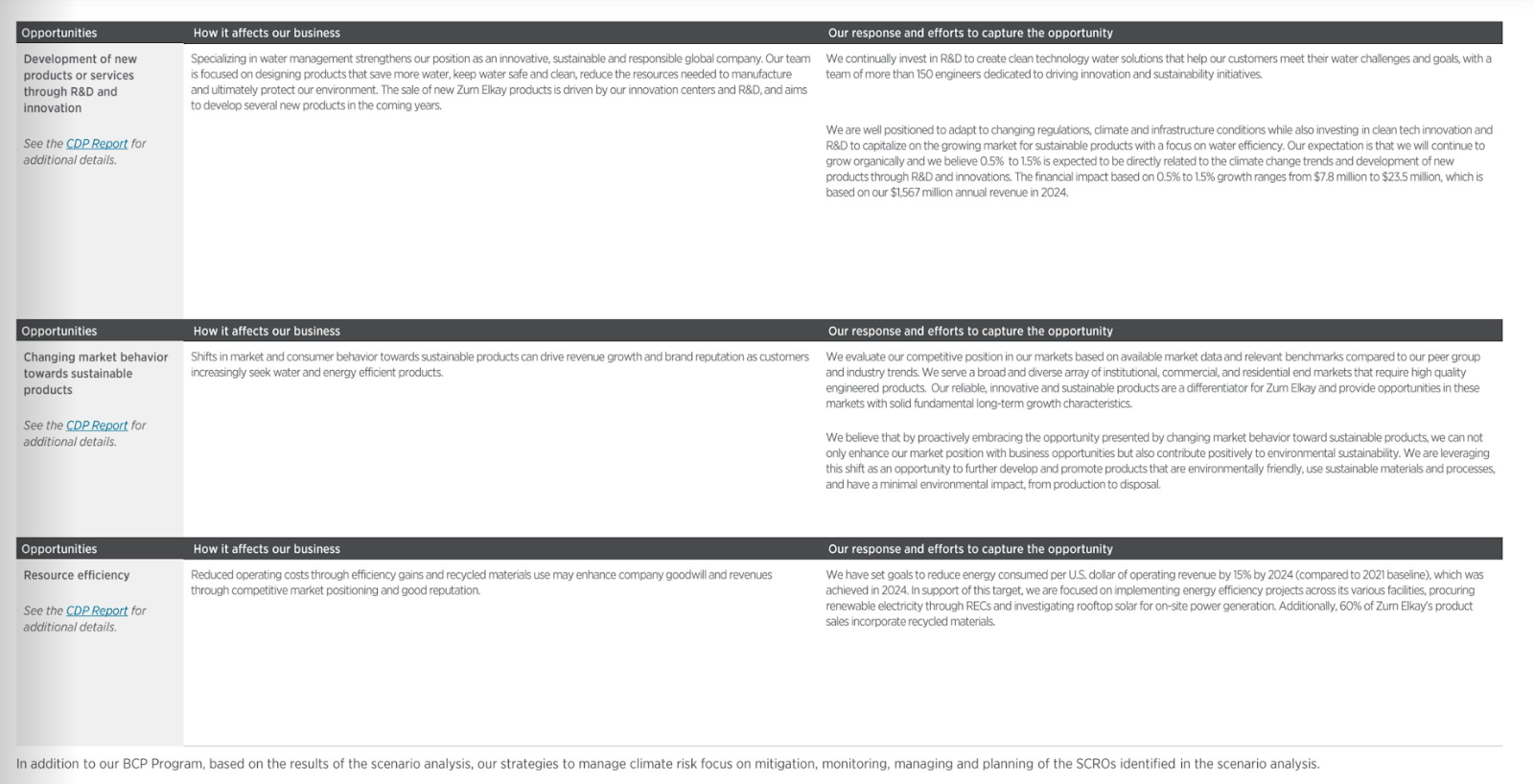

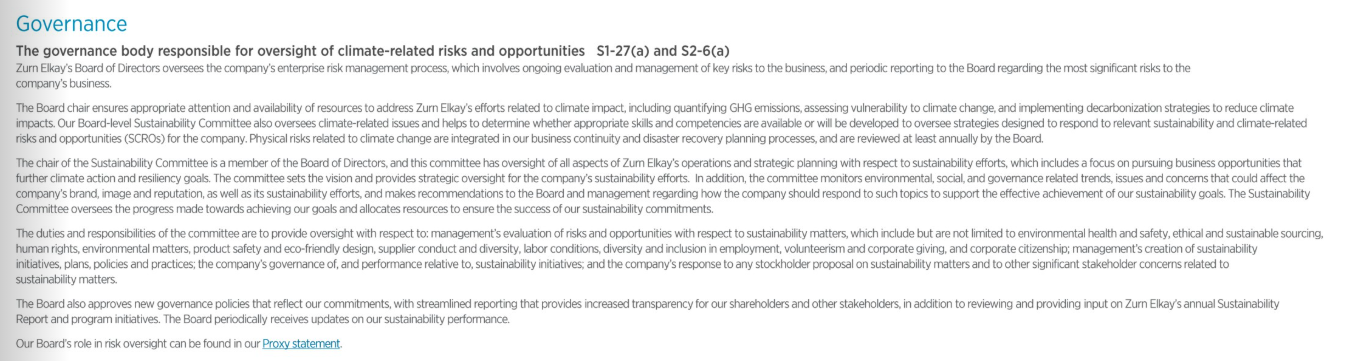

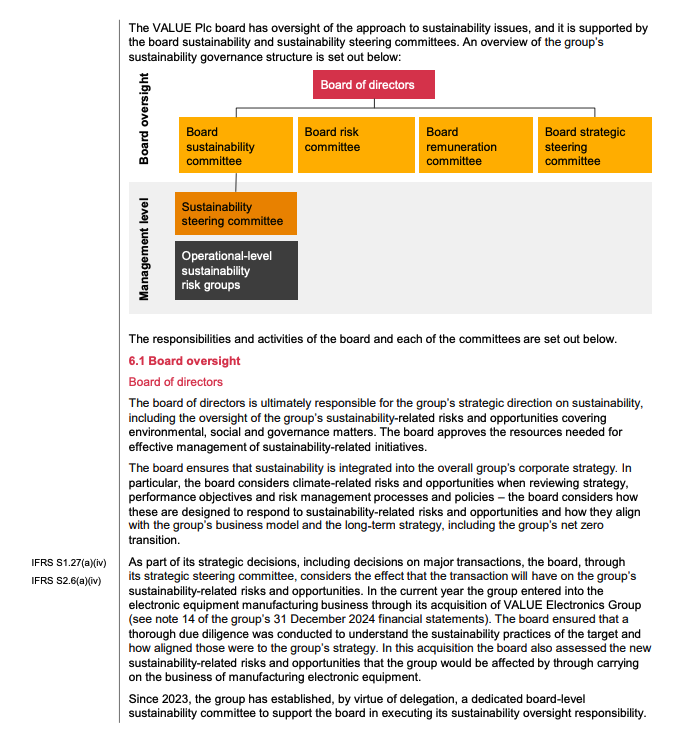

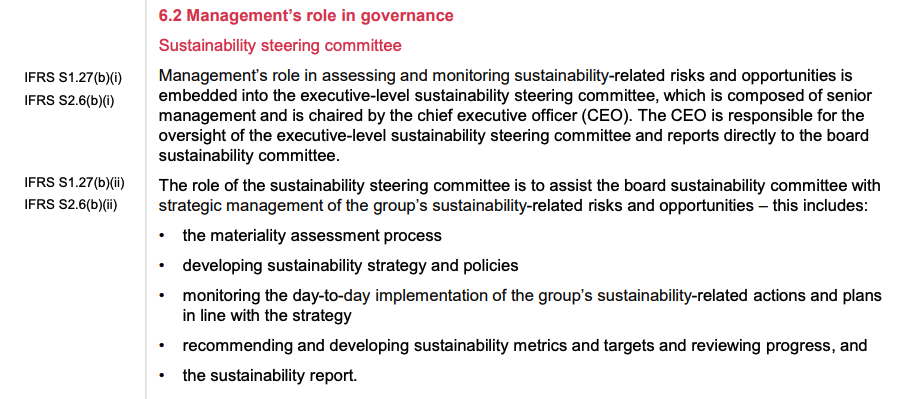

We have only found one example of an IFRS index where a company actually puts the answers by the disclosure requirement and that is done by Zurn Elkay -> Zurn Elkay: IFRS Index. The other best example we have found is a fictional report published by PwC around what an IFRS content index could look like. Pwc -> Example Index. A handful of additional companies have published IFRS Index’s but those are harder to use as best practice example as most of those disclosures use the framework as an index reference to their annual report they do not disclose within the framework itself.

Below we showcase more examples from Zurn Elkay and PwC:

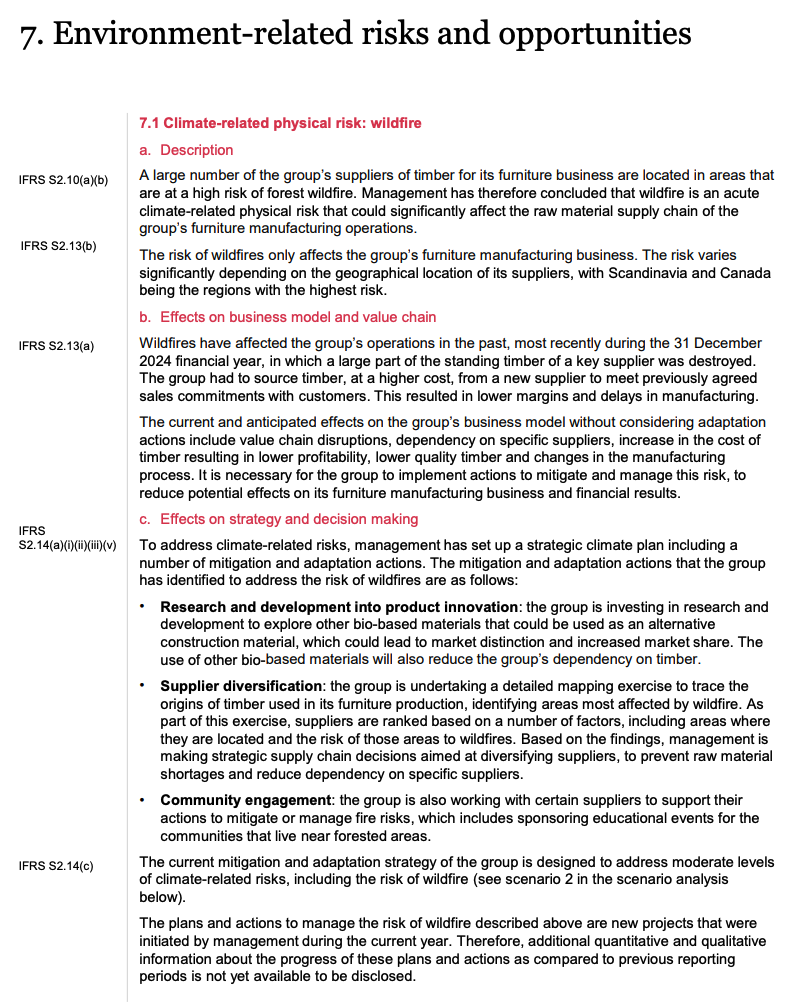

In IFRS S2 regulation, risk and opportunity disclosure refers to the requirement for companies to provide transparent, decision-useful information about the climate-related risks and opportunities that could reasonably be expected to affect their business model, strategy, cash flows, access to finance, or cost of capital over the short, medium, and long term. This involves detailing both physical risks (such as those arising from extreme weather events or chronic climate changes) and transition risks (stemming from policy, legal, technological, or market shifts in response to climate change). Companies are also expected to outline climate-related opportunities—for example, market expansion through low-carbon products or efficiency gains from green technologies. The purpose is to enable investors and other stakeholders to assess how resilient the company’s strategy is in light of climate change and how management plans to adapt, mitigate, or leverage these evolving factors.

Below we show examples of how a company could disclose in line with these expectations.