Interviews

Building Internal Controls for CSRD: Lessons from a Wave 1 Company

An interview with Seraphina Kim about applying internal controls for CSRD disclosure.

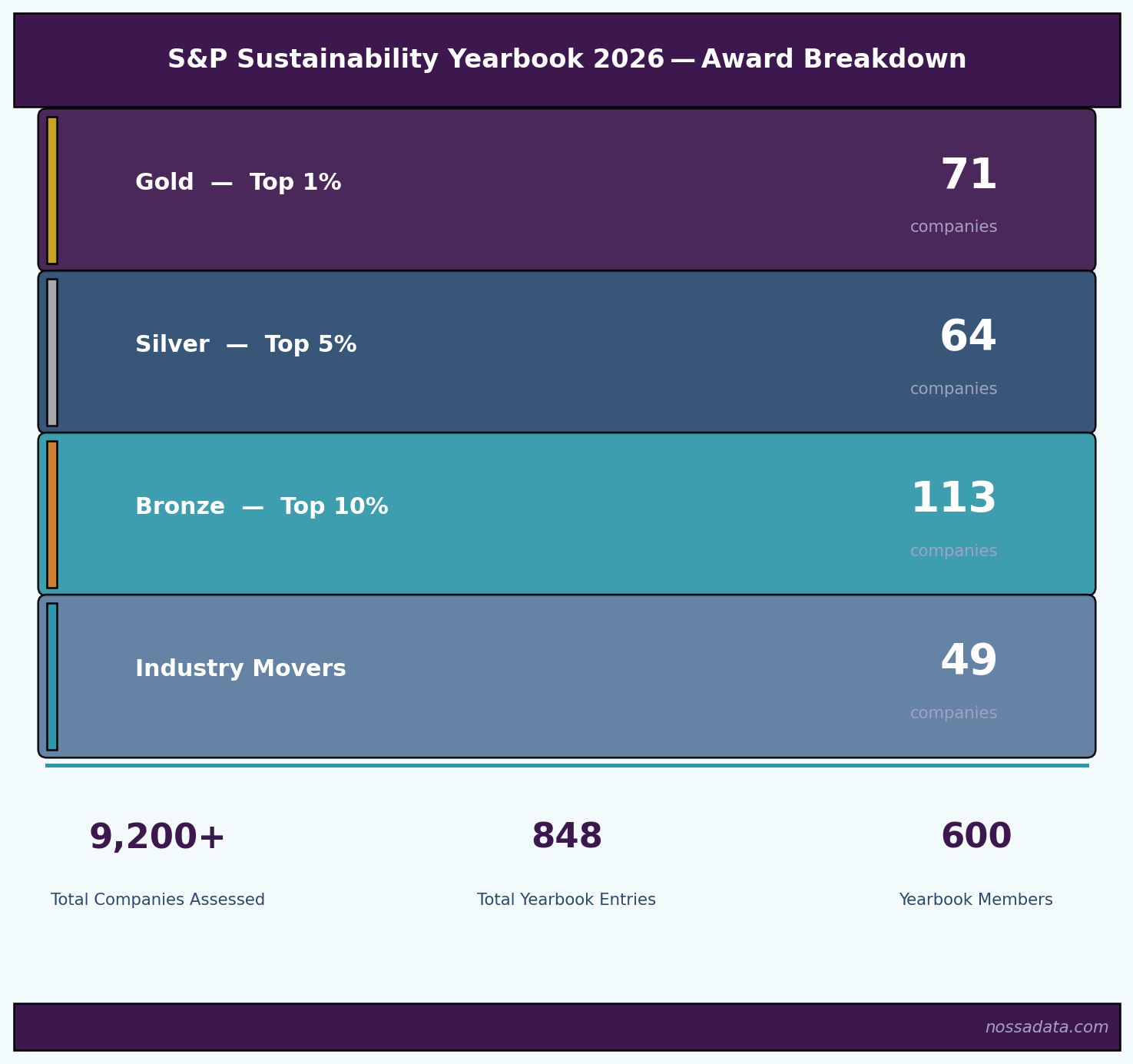

We are just over one month into the 2026 S&P CSA rating cycle, so we decided to review the headline results from the S&P Global Sustainability Yearbook 2026. The Yearbook considers the ESG performance of over 9,200 companies assessed during the 2025 CSA cycle (results of which feed the 2026 Yearbook). Of those companies, just 848 earned a place in the Yearbook — fewer than 10% of all participants. You can view the full list of ranked companies here.

In this article we unpack what the S&P CSA actually is, how the Yearbook selection process works, what changed in the 2026 methodology, and what the results tell us about the global state of corporate sustainability — from which countries are dominating to which European companies achieved the coveted Top 1% Gold classification.

The S&P Global Corporate Sustainability Assessment — commonly referred to as the CSA — is one of the world’s most widely recognised ESG evaluation frameworks. First launched in 1999, the CSA has spent more than two decades refining how corporations measure, manage, and communicate sustainability performance across environmental, social, and governance dimensions.

At its core, the CSA uses industry-specific questionnaires to assess how well companies manage the ESG risks, opportunities, and impacts that are financially material to their business. S&P Global translates an average of 1,000 data points per company into a single S&P Global CSA Score on a 0–100 scale, enabling transparent, like-for-like benchmarking across 62 industries. The assessment covers an average of 23 sustainability topics across approximately 110 questions per industry, of which roughly 40–50% relate to general cross-industry criteria and the remainder are tailored to sector-specific risks and opportunities.

Participation in the CSA is open to any company worldwide. S&P Global directly invites thousands of companies each year, though any organisation can request inclusion. In the 2025 assessment cycle (feeding the 2026 Yearbook), more than 9,200 companies took part — a figure that has grown substantially year-on-year as investor and regulatory expectations around ESG disclosure continue to rise. The CSA is also used by financial institutions managing over $35 trillion in assets to benchmark portfolio companies, manage investment risk, and build engagement strategies.

Companies participate by completing their industry-specific CSA questionnaire. Submissions are supported by documentary evidence, which S&P analysts then independently review — they may revise responses either upward or downward based on publicly available information. Companies receive their scores within a target window of 6–10 weeks after submission. For a full overview, refer to the CSA factsheet published by S&P Global Sustainable1.

Scores are determined by performance across three dimensions: Economic, Environmental, and Social. Within each dimension, industry-specific criteria are weighted according to their financial materiality. Key factors that influence a company’s score include the quality and comprehensiveness of sustainability policies, the robustness of management systems, the transparency of KPI reporting, and the degree to which strategies align with recognised global frameworks such as the Paris Agreement. Since 2026, the S&P CSA also formally incorporates a Sustainable Artificial Intelligence criterion (see the methodology updates section below).

Want to speak to Nossa Data to learn about ESG Reporting and Benchmarking? Contact solutions@nossadata.com to learn more about how we work with listed issuers across their ESG disclosure.

The S&P Global Sustainability Yearbook is published annually and recognises the highest-scoring companies from the prior year’s CSA cycle. Selection is based on a company’s S&P Global ESG Score — specifically, the raw CSA score without any modelling adjustments. To be eligible, a company must clear three hurdles simultaneously: it must score at least 30 overall; it must rank within the top 15% of its industry peer group; and its score must fall within 30% of the highest score in that same industry. Additionally, companies are screened through S&P Global’s Media and Stakeholder Analysis (MSA) process, which can disqualify those with serious ESG controversies regardless of their CSA score. The full Yearbook selection process overview is publicly available on the S&P Global Sustainable1 website.

For the 2026 edition, the underlying universe was fixed on 31 December 2025, covering all companies assessed in the 2025 CSA cycle up to that date. From a starting universe of more than 9,200 assessed companies, only 848 made the Yearbook — highlighting just how competitive inclusion has become.

Within the Yearbook, companies are further recognised through four distinction levels based on where they rank within their industry:

• Gold — Top 1%: CSA score of at least 60, ranking in the top 1% of their industry.

• Silver — Top 5%: CSA score of at least 57, ranking between the top 1% and top 5%.

• Bronze — Top 10%: CSA score of at least 54, ranking between the top 5% and top 10%.

• Industry Mover: Companies that have shown the most significant score improvement year-on-year within their industry.

Figure 1: S&P Sustainability Yearbook 2026 — Award Breakdown

Each year, S&P Global publishes an overview of methodology updates to help companies understand what has changed before they begin their assessment. The full CSA 2026 Methodology Updates Overview was published on 26 March 2026 and is required reading for any sustainability team preparing their submission. Below are the headline changes for the 2026 cycle:

Perhaps the most significant structural change in 2026 is the elevation of Sustainable Artificial Intelligence from a “future questions” pilot into a fully weighted criterion. This reflects the rapidly evolving AI landscape and its direct operational sustainability implications. The updated criterion now formally asks companies whether they have a policy on responsible AI that covers: data and cybersecurity; human oversight in critical decisions; transparency in AI outcome generation; and the avoidance of exploitative or manipulative AI behaviour. A new “Artificial Intelligence KPIs” question has also been introduced, requiring companies to report measurable indicators against their AI governance commitments.

A new Transition Plan question has been added under the Climate Strategy criterion. This question assesses whether a company has a formally documented climate transition plan aligned with the Paris Agreement, including clear interim milestones, capital allocation commitments, and accountability mechanisms. This reflects the growing convergence between the CSA and major climate disclosure frameworks such as TCFD and the ISSB standards.

A new question under the Product Stewardship criterion requires companies to report on their formal programmes for developing and scaling sustainable products or services. This moves the needle from policy commitments toward evidence of execution — companies will need to demonstrate active programmes rather than aspirational statements.

A notable shift in 2026 is the strengthening of transparency requirements: several questions that previously accepted non-public documentation as supporting evidence now require or strongly incentivise the use of publicly available sources. This increases the premium on proactive, accessible ESG disclosure and is likely to widen the gap between companies with mature sustainability reporting and those relying on internal-only evidence.

Key Takeaway for 2026 Participants:

If your company has not yet formalised an AI governance policy or a Paris-aligned transition plan, these two areas represent meaningful scoring opportunities in the 2026 cycle. S&P’s methodology shift toward public evidence also rewards companies with strong, accessible sustainability reports.

Want to speak to Nossa Data to learn about ESG Reporting and Benchmarking? Contact solutions@nossadata.com to learn more about how we work with listed issuers across their ESG disclosure.

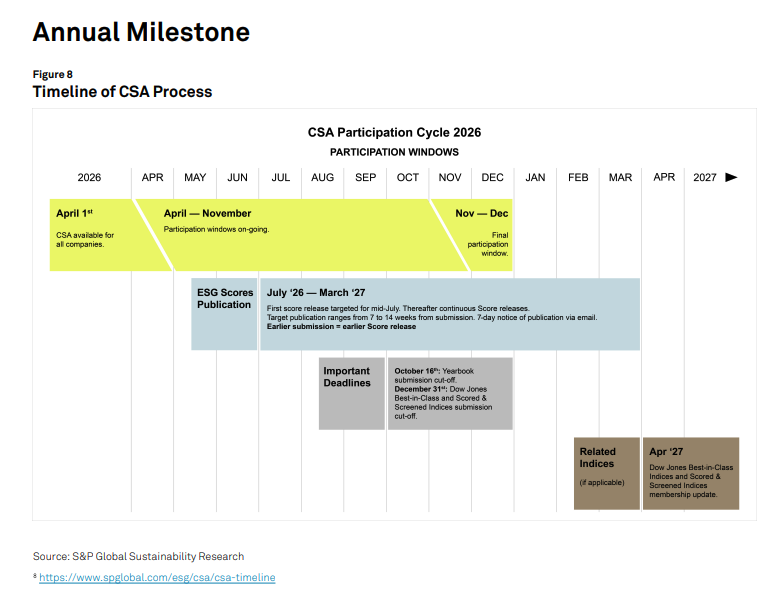

The 2026 CSA cycle opened on 1 April 2026, with the industry-specific questionnaires becoming available in the Sustainability Reporting Portal on that date. Participation windows are offered on a rolling basis, starting at the beginning and middle of each month between April and November 2026. November is the final available window and does not have a mid-month start option.

Key dates to note for the 2026 cycle:

• First score release: Intended for mid-July 2026.

• Score turnaround: Companies can expect results within 6–10 weeks of submission, depending on S&P analyst workload.

• Yearbook eligibility deadline: The latest participation window for companies to be considered for The Sustainability Yearbook 2027 is the August 17–October 16, 2026 window (submission by 16 October 2026).

• DJSI Best-in-Class Index (DJBICI) eligibility: Companies must submit their 2026 CSA by 31 December 2026.

The CSA spans 58 industries in total, making it one of the broadest ESG benchmarking frameworks available. However, participation is far from evenly distributed. Eight industries each had more than 300 assessed companies in the 2025 cycle, reflecting either the scale of those sectors in global capital markets or the intensity of investor scrutiny they face:

• Banks

• Chemicals

• Diversified Financial Services and Capital Markets

• Electronic Equipment, Instruments & Components

• Equity Real Estate Investment Trusts (REITs)

• Machinery and Electrical Equipment

• Real Estate Management & Development

• Retailing

The dominance of financial services and industrial sectors reflects sustained investor pressure for ESG transparency in capital-intensive and systemically important industries. For companies in these sectors, strong CSA performance is increasingly a prerequisite for institutional investor engagement.

Of the 848 companies that made the 2026 Yearbook, the geographic distribution tells a striking story:

Asia dominates the top 20 countries, accounting for six of the top seven positions. Taiwan leads the Yearbook with 79 member companies, followed closely by India (76) and Japan (69). The first non-Asian country in the ranking is the United States at position eight with 47 companies. The first European country to appear is Spain, at position nine jointly with Chile, with 33 companies each.

This geographic pattern reflects both the depth of sustainability reporting cultures in Asian markets and, in some cases, the scale of corporate sectors in countries like Taiwan (semiconductors), India (IT and pharmaceuticals), and South Korea (diversified conglomerates). For European and North American companies, the data suggests that despite strong regulatory pressure, Asian peers have developed a consistent edge in CSA participation and performance.

Figure 3: Top 20 Countries by Number of S&P Sustainability Yearbook 2026 Members

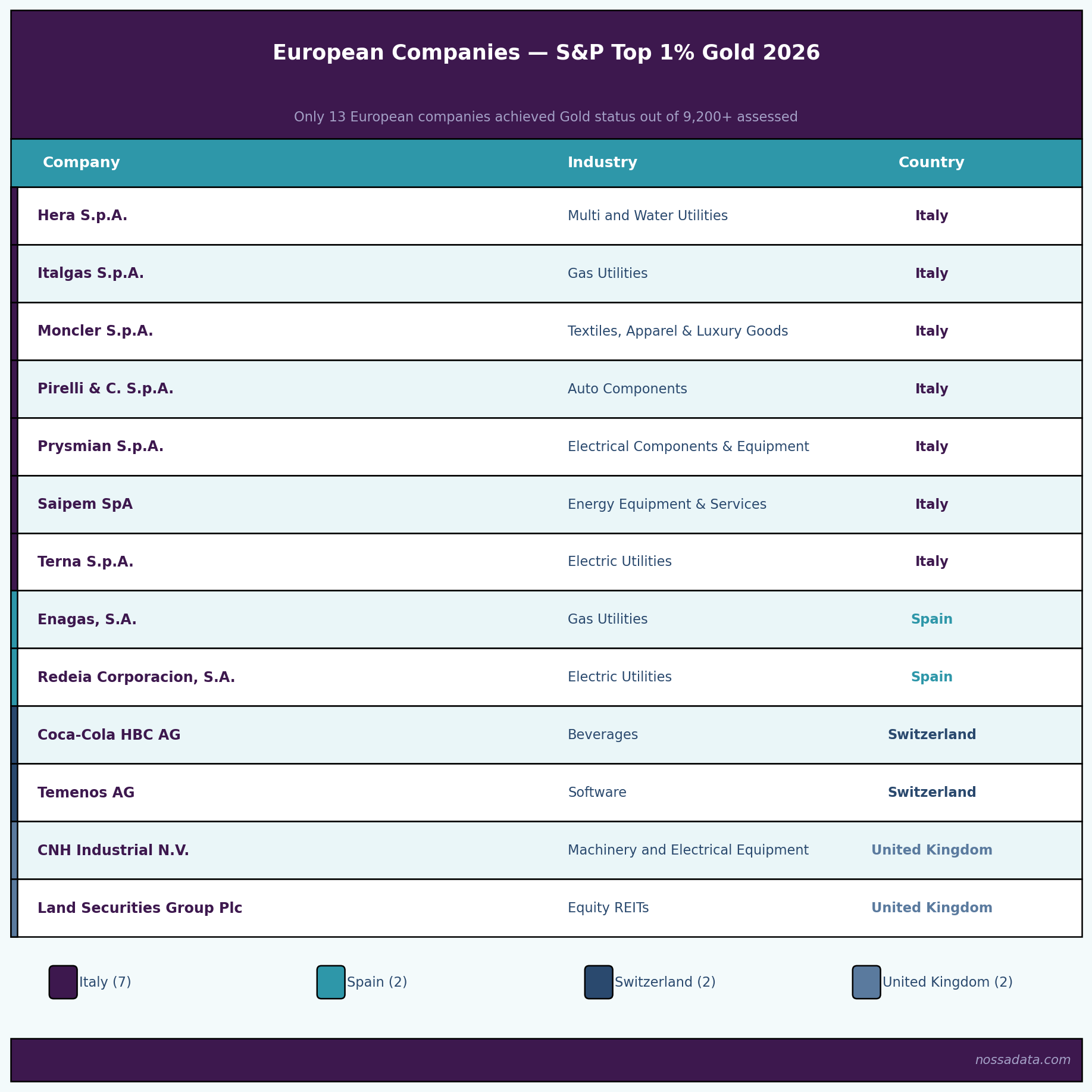

Of the 848 companies in the 2026 Yearbook, 71 achieved the coveted Gold distinction — placing them in the Top 1% of all companies in their industry globally. Achieving Gold requires a CSA score of at least 60 and a top-1% ranking within the peer group: a bar that fewer than one in 130 assessed companies clears.

A notable headline from the 2026 results is that only a single American company achieved Gold status: Owens Corning, the Ohio-based building products manufacturer. This underscores that size and market capitalisation are no guarantee of ESG performance, and that Gold classification requires sustained, evidence-based disclosure across a broad range of sustainability criteria.

Europe contributed 13 Gold-classified companies in 2026 — a figure that, while respectable, reinforces the scale of the competitive challenge facing European corporates when measured against a global peer group. Italy is the standout European performer with seven Gold companies, spanning utilities, industrial, and luxury goods sectors. Spain contributes two companies, and Switzerland and the United Kingdom two each.

Figure 4: European Companies Achieving S&P Top 1% Gold Status in 2026

The S&P Global CSA Sustainability Yearbook 2026 paints a clear picture: the bar for recognised sustainability performance continues to rise, competition for distinction is intensifying, and geography continues to play a significant role in shaping who reaches the top.

For companies currently working through the 2026 CSA cycle, the methodology shifts toward AI governance, climate transition planning, and public disclosure transparency present both challenges and material scoring opportunities. For those not yet participating, the Yearbook data makes a compelling case: with Yearbook membership increasingly cited in investor engagement and procurement due diligence, CSA participation is fast becoming a baseline expectation rather than an optional exercise.

If you’d like to understand how your organisation can improve its CSA score or prepare a stronger submission, the Nossa Data platform is built to help sustainability teams find, organise, and surface the exact evidence that Sustainability analysts are looking for — efficiently and at scale. Get in touch at solutions@nossadata.com

• S&P Global Corporate Sustainability Assessment (CSA)

• S&P Global Sustainability Yearbook 2026 — Full Rankings

• CSA Yearbook Selection Process Overview

• CSA 2026 Methodology Updates Overview (PDF)

• CSA Corporate Sustainability Assessment Factsheet (PDF)

• CSA Timeline & Participation Windows