Interviews

Three Years of CSRD Reporting: Lessons from an Early Mover, Ørsted

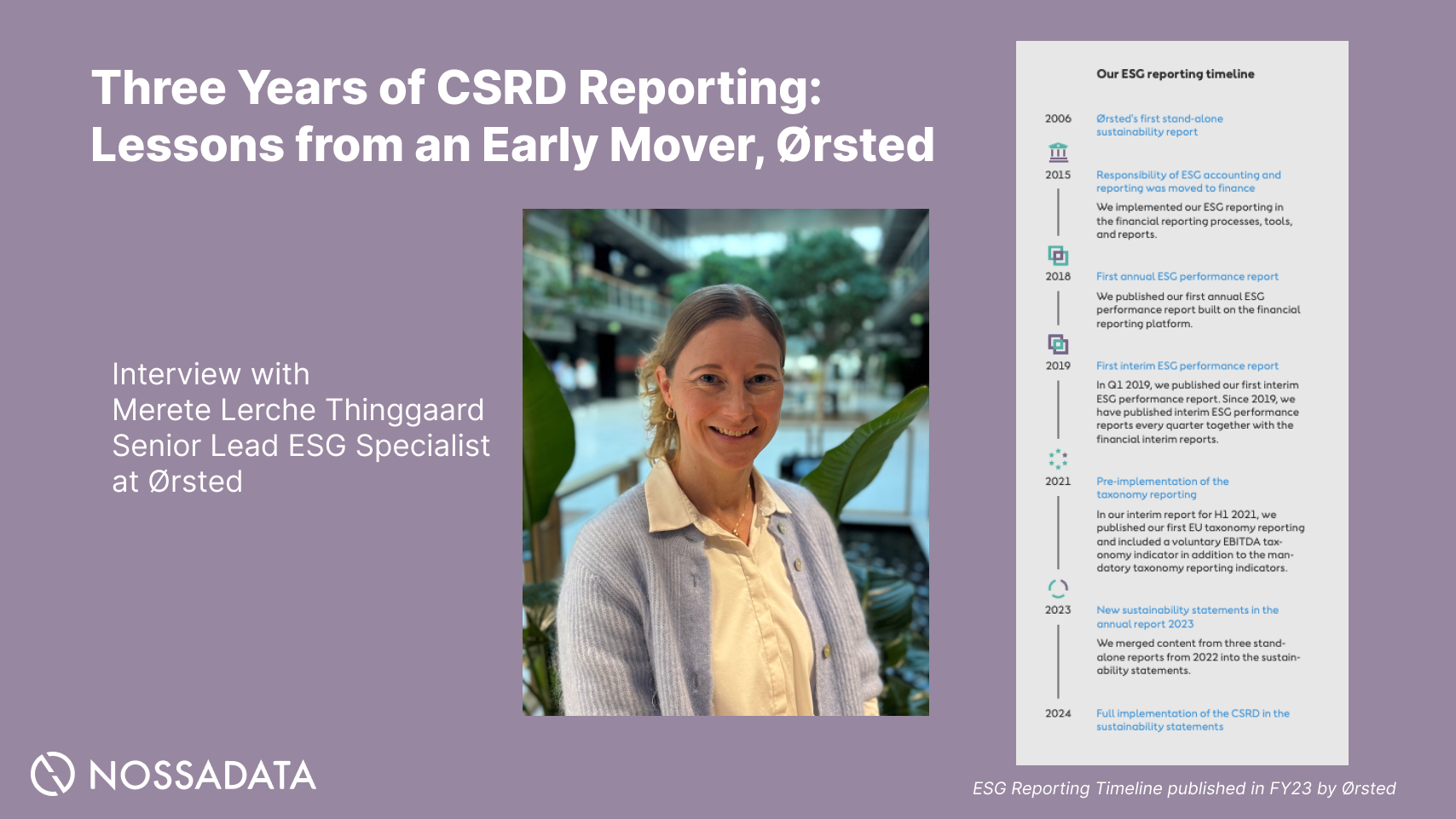

An expert interview with Merete Lerche Thinggaard, Senior Lead ESG Specialist at Ørsted, on three CSRD reporting cycles.

With ESG gaining traction comes the need to understand the different investment vehicles within it. One of the key topics in its growth is Sustainable Debt. To help you get up to speed on the Sustainable Debt space we have created an introductory guide.

*Still have questions about ESG? Read our intro to ESG guide and subscribe to our weekly educational newsletter.

Sustainable Debt is the issuance of bonds and loans that fund projects serving environmental, social, and sustainability purposes. The Sustainable Debt market is composed of Green, Social, and Sustainability Bonds (GSS Bonds) and Green, Social, and Sustainability-linked Loans, which raise capital for projects with positive GSS benefits, such as climate mitigation and public health initiatives. The GSS acronym is also seen expanded to GSSS to include Sustainability-linked debt types.

Traditionally, Sustainable Bonds fall into two general categories, Use-to-process bonds and Sustainability-linked bonds:

Guidelines (attached here) for classifying Green Bonds, Social Bonds, Sustainability Bonds, and Sustainability-Linked Bonds are determined by The International Capital Market Association to provide consistency and transparency in the market. The Loan Market Association does the same for Green, Social, and Sustainability-Linked Loans.

Sustainable debt types are growing beyond GSS Bonds as both market awareness and issuers’ needs expand. 2018 saw the issuance of the first Blue Bond, which raises capital specifically for marine projects. Brown Bonds and Transition Bonds have also emerged to transition fossil fuel industries towards clean-energy when projects are too unclean to qualify for Green Bonds. Carbon-neutral Bonds have appeared as well.

Furthermore, bonds are not the only way that Sustainable debt is expanding. Sustainable debt is becoming a growing part of the global fixed income market, thanks to its unique ability to allow companies and governments to provide GSS relief. This is while meeting internal sustainability goals, and appeasing both investors’ and the public’s increased interest in sustainability.

Sustainable debt has grown rapidly in the past few years. Since 2007, around $1 trillion USD in Green Bonds, $316 billion USD in Social Bonds, and $317 billion USD in Sustainability Bonds have been issued. According to Bloomberg, 2020 recorded $732.1 billion USD in bond and loan issuances, up 29% from 2019 and a record for volume of issuances in a year. Further, more than 50 issuances raised $2 billion+ in 2020 compared to 15 in 2019, pointing to the increase in both number and volume of issuances.

In the first quarter of 2021, sustainable investments again outperformed. Matthew Toole, Director of Deals Intelligence at Refinitiv, noted that in the first quarter of the year it accounted for a “record 11 percent of global capital markets activity and [set] all-time quarterly records for equity capital markets and syndicated lending” (Forbes India.) In line with this growth, a poll from Environmental Finance showed two-thirds of respondents expected to see 2021’s global issuances at $600 billion and $700 billion, and the better part of the rest predicting between $700 to $800 billion USD.

In addition to Sustainable Debt’s market growth, the types of GSS Bonds issued are also expanding:

Green Bonds have historically occupied the largest portion of the Sustainable debt market, and account for 1-2 percent of global fixed-income assets (approximately $1 trillion USD.) However, the market has diversified in recent years: In 2018, 85% of GSSS Bond issuances were Green Bonds but in 2020, only about 50% of GSSS Bonds were Green. This left space for an increase in Social, Sustainability, and Sustainability-Linked Bonds.

Social Bonds reached $147.7 billion USD, a 720% increase from 2019. As Social Bonds include projects such as public health initiatives and job-support programs, this jump was likely in reaction to the COVID 19 pandemic. For the same reason, Sustainability Bonds also saw an 81% increase in this time to $68.7 billion USD.

Fannie Mae, a mortgage loan company sponsored by the US government, led 2020 Green Bond issuances with $13.0bn. The agency’s Multifamily Green MBS program finances mortgages for properties that are in line with Green Building Certifications or show water and energy efficiency improvements.

The Federal Republic of Germany ranked second in Green Bond issuances ($12.8bn) after its initial green sovereign bond. Germany has one of the largest domestic green bond markets globally thanks to KfW, a state owned investment and development bank, which ranks fourth.

Société du Grand Paris, which was established by the French government in 2010 to expand its metro and commuter rails and create the “Grand Paris Express,” ranked third with $12.2bn in issuances. The Republic of France’s sovereign program ranked fifth.

These issuers allowed the United States, Germany, and France to lead as the Top 3 Countries in Annual Green Bond Issuances in 2020.

The United States issued the most Green Bonds of any Country in 2020 ($51.1bn), followed by Germany ($40.1bn) and France ($32.1bn). Europe more broadly issued the greatest amount of green debt in 2020, 48% of all green debt, to total $165bn.

The European Union led in Social Bond issuances in 2020. It funded the largest single Social Bond ever, valued at $17bn in October 2020.

In March 2020, the African Development Bank issued the largest Social Bond at the time, $3bn in response to the COVID 19 pandemic. Unedic Asseo issued a $4bn Social Bond in May 2020 and again in June 2020 in response to the pandemic. Social Bonds issued in response to COVID 19 funded job support programs and other public health and social support initiatives.

The Sustainability Bond market, which allows both Social and Green Bonds, saw less growth than Green and Social Bonds this year, but growth nonetheless. The World Bank led in Sustainability Bond issuances with $8bn in Sustainability Bonds issued.

Blue Bonds: Blue Bonds are a bond instrument that raise capital for projects with marine or ocean-based benefits. The first blue bond was issued in 2018.

Climate Bonds: Fixed income bonds for climate change solutions/mitigation.

ESG integration: (ESG) integration is the practice of incorporating ESG information into investment decisions to help enhance risk-adjusted returns, regardless of whether a strategy has a sustainable mandate.

Four Core Components of the GBP and SBP: The Four Core Components of the GBP and SBP outline the necessary qualifications for a Green or Social Bond. They are:

1. Use of Proceeds 2. Process for Project Evaluation and Selection 3. Management of Proceeds 4. Reporting

Green Bonds: Green Bonds are any type of bond instrument that raise capital, partially or fully, for new and/or existing projects with positive environmental benefits. The first Green Bond was issued in 2007.

Green Loans (GLs): Green loans are loans that are allocated to projects with positive environmental benefits.

Green Bond Principles (GBP): Green Bond Principles are voluntary guidelines set by the International Capital Market Association (ICMA) that recommend transparency, disclosure and reporting in the Green Bond Market. They outline the necessary qualifications that must be met for a Green Bond.

Green, Social, and Sustainability Bonds (GSS Bonds): An encompassing phrase to talk about the major bond types consistent with sustainable debt.

International Capital Market Association (IMCA): “The International Capital Market Association is a self-regulatory organization and trade association for participants in the capital markets.” (IMCA)

Social Bonds: Social Bonds are any type of bond instrument that raise capital, partially or fully, for new and/or existing projects with positive social impacts. The first Social Bond was issued in 2010.

Social Bond Principles (SBP): Social Bond Principles are voluntary guidelines set by the International Capital Market Association (ICMA) that recommend transparency, disclosure and reporting in the Social Bond Market. They outline core principles of meeting qualifications for a Social Bond.

Sustainability Bond: Sustainability Bonds are bonds that finance or refinance both Green and Social Projects. They follow the GBP and SBP.

Sustainability Bond Guidelines: Sustainability Bond Guidelines are guidelines set by the International Capital Market Association (ICMA) that recommend transparency, disclosure and reporting in the Sustainability Bond Market. The core principles in meeting qualifications for a Green and Social Bond apply to Sustainable Bonds.

Sustainability-Linked Bonds (SLB): Sustainability-Linked Bonds are bond instruments that raise capital for a company under the acknowledgment that it meets externally monitored sustainability/ESG goals during the bond’s issuance. The main difference between SLB and GSS Bonds are that SLB can be used for general corporate purposes.

Social Loan: Social loans are loans that exclusively finance or refinance, fully or partially, new and/or existing projects with positive social impacts.

Social Loan Principles: Social Loan Principles are a framework set by the Loan Market Association that outline the four core components of a Social Loan:

1. Use of Proceeds

2. Process for Project Evaluation and Selection

3. Management of Proceeds

4. Reporting

Sustainability-linked loan: Sustainability-linked loans are loans allocated to a company under the acknowledgment that it meets externally monitored sustainability/ESG goals. The main difference between SLL and GSS Loans are that SLL can be used for general corporate purposes

Sustainability-linked Loan Principles: Sustainability-linked Loan Principles are a framework set by the Loan Market Association that outline the four core components of a Sustainability-linked Loan:

1. Relationship to Borrower’s Overall Corporate Social Responsibility (CSR) Strategy

2. Target Setting – Measuring the Sustainability of the Borrower

3. Reporting

4. Review

Sustainability-linked Bond Principles: The SLBP have five core components:

1. Selection of Key Performance Indicators (KPIs)

2. Calibration of Sustainability Performance Targets (SPTs)

3. Bond characteristics

4. Reporting

5. Verification

Taxonomy regulation: Taxonomy regulation is EU-wide framework that classifies which economic activities are considered environmentally sustainable using four core requirements:

1. They provide a substantial contribution to at least one of the six environmental objectives.

2. 'No significant harm’ is caused to any of the other environmental objectives.

3. Compliance with robust and science-based technical screening criteria.

4. Compliance with minimum social and governance safeguards