Interviews

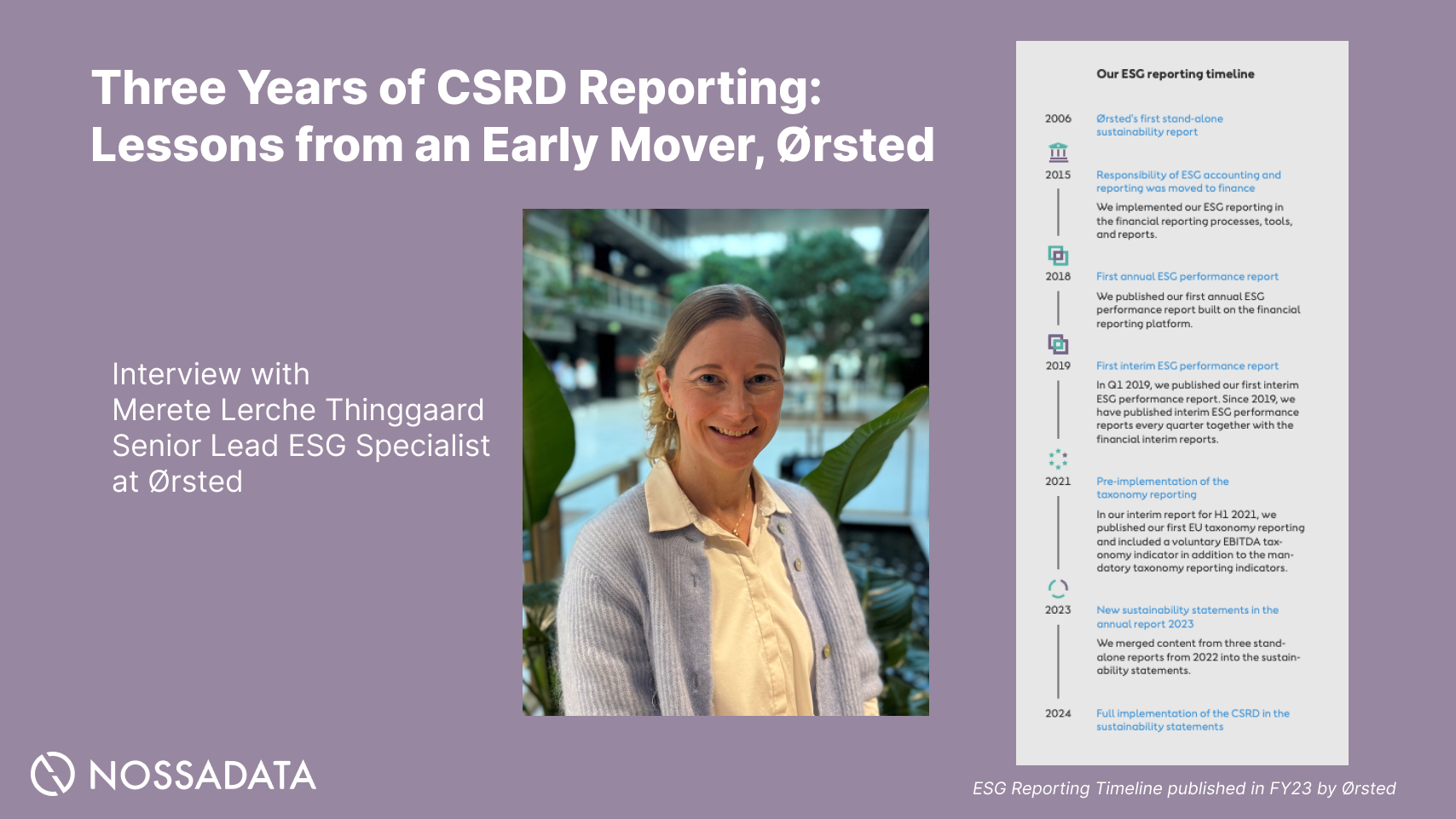

Three Years of CSRD Reporting: Lessons from an Early Mover, Ørsted

An expert interview with Merete Lerche Thinggaard, Senior Lead ESG Specialist at Ørsted, on three CSRD reporting cycles.

An Interview with Dr. Kim Schumacher, a lecturer in Sustainable Finance and ESG at the Tokyo Institute of Technology, the creator of the first graduate-level course on Sustainable Finance in Japan. He is also the founding director of the Japan Sustainable Finance Research Network. His work and research is focusing on ESG, Impact Analysis, Sustainable Finance, Sustainable Energy Transition, Clean Energy Technology Development, Climate Change Law and Policy, and Environmental Regulatory Procedures.

We recently got an opportunity to interview Dr. Schumacher and gather his views on greenwashing, the new EU regulations and the urgent need to involve more natural science professionals into the field of ESG and sustainable finance.

Q: What led you to become involved in sustainable finance and ESG?

Kim: “What got me involved in ESG and sustainable finance is not so straightforward. I am not a trained financial professional. I originally studied law and in 2011, I was able to go to UC Berkeley. I had a scholarship to go there and study environmental law. This was around the time when the entire nuclear power discussion was unfolding in Japan, after the Fukushima nuclear accident and the subsequent shut down of all the nuclear power capacity. I was very intrigued in how Japan managed the transition towards a post-nuclear society. I was also not very interested in pure law anymore. So I finished my degree but felt I wanted to learn more about technology and science. For the next six months I studied non-stop and tried to catch up on my scientific knowledge. I had to do this for an entrance exam as I had enrolled myself in a PhD program in Environmental Science at the University of Tokyo, in Japan. I selected my supervisor specifically because he used to work for TEPCO, the company which managed the nuclear power plants in Japan. I then began studying the environmental impact of the large-scale renewable energy projects during my PhD. I looked at what barriers, including regulatory ones, these types of projects were encountering and examined various types of environmental data - such as bird strikes! This was all very interesting and the interdisciplinary aspects really fascinated me.

After I finished my PhD in 2017, I had the opportunity to go to Oxford and join their sustainable finance program as a postdoc. I had both - the legal background and the scientific background, and they were looking for someone exactly like that. Here I had the chance to do a very diverse set of research around sustainable finance, for example, scenario modelling risks in terms of carbon exposure etc. Soon I was able to get my own funding from the European Investment Bank and from the UK Higher Education Innovation Fund to look into the impacts of green bonds.

Unfortunately, I became a victim of Brexit and was told that the funding coming from the European Investment Bank would no longer be available once the UK leaves. This is when I had the opportunity to return to Japan and create the first sustainable finance course in the country! This was basically the route that I took.”

Q: Over the course of your career, what are some of the major developments that you have seen in ESG?

Kim: “Well, there is a sequence of developments - first, with climate change becoming more tangible and real, people and investors are becoming much more aware of their impact. From raging forest fires to the continued and accelerating melting of glaciers and ice sheets. People are now becoming much more aware, and this includes investors. Forest fires or heat waves that used to occur only maybe once every 10 years are now rapidly increasing and occurring every 1-2 years. All this has led to the rapid growth of green finance, sustainable funds, climate bonds etc. All of these have risen dramatically over the last 5 or so years. Now, we are actually seeing an exponential growth where sustainable finance is outpacing even regular investments, at least in terms of growth rates. Although, in terms of absolute volume it's still far below.

Second, what all this growth has brought with it is the question about how many of these products are actually ‘green’? Greenwashing is really one of the main problems today and it stems from our lack of knowledge. We do not know if these sustainable finance products fulfil the promises that they make. For example, products can say that they will reduce carbon emissions, reduce deforestation or improve biodiversity etc, but often there is no data to test or verify these claims.

Lastly, this is where we see a lead-in to regulatory developments. Today, regulators all over the world have become much more aware that the green finance market was largely unregulated for a long time. There was basically no oversight of preventing greenwashing and no one was holding investors and issuers up to their promises. In reality, sustainable finance was oftentimes actually just a refinancing exercise where existing assets were basically refinanced at a lower rate because green finance products offered better conditions.

So these are the three key developments I see: the scaling of the market, the questioning of greenness, and the regulatory measures to address greenwashing.”

Q: Is there a need to include more natural-science professionals in the ESG space?

Kim: “Yes. 110% Yes. Greenwashing is not limited to financial products. It also applies to teams and individuals. Because of the rapid scaling of the sustainable finance market, there is a trend where a lot of people try to present themselves as sustainability, climate, or environmental experts. This is called “competence greenwashing”. Currently a lot of people who work in sustainable finance have finance, business or accounting backgrounds. However, a lot of the new regulation in sustainable finance goes into very technical and concrete natural science concepts such as climate scenario modelling or biodiversity assessments. It is great that financial professionals are taking short-courses in sustainable finance but these classes do not make them subject matter experts. For instance, if one was to undergo a brain surgery, would they prefer a doctor who has merely read an introductory book, or one that has read the book as well as gathered relevant practical experience? If I were an investor, I would be very worried if my team lacked natural science professionals as it would be difficult to measure or even understand a lot of the complex ESG data. It is also important to note that not all natural sciences professionals are identical - each area requires specialist training. Take, for example, a water-related ESG investment which would require someone with expertise in hydrology. I encourage financial professionals to learn more about ESG and green finance but I do not think that this can compensate for the lack of a team-member with a scientific background. In the future, we should have sustainability teams that are composed roughly of 50% financials and 50% non-financials because there will be a synergetic cross-pollination effect. This way, they can learn from each other and this is the sort of interdisciplinary collaboration that is needed in this industry moving forward.

Additionally, as we saw in the 2008-09 crisis, the control mechanisms in the financial industry often do not work reliably. In contrast, the accountability mechanisms in the scientific community are considered to be much stronger. We need to bring this into the sustainable finance industry. In the scientific community, we have the process of peer review which acts as a safety check to ensure that there are no overtly misleading statements or outrageous over-estimations.”

Q: With designing the first graduate level Sustainable Finance course in Japan, what were some of the key areas you wanted in the curriculum?

Kim: “Not all sustainable finance curricula are the same. I am a lecturer at the Tokyo Institute of Technology, which is a university with a strong focus on natural sciences. So most of my students tend to have more scientific backgrounds such as engineering or chemistry. Hence, my course is trying to teach scientists about finance. This is why I try to teach them in a way that makes them comfortable with core financial concepts. For example, key investment principles, what are the different financial products that are out there, or about bonds etc. I try to make the link between how investing relates to natural science. I focus on things such as how do we integrate environmental data into a format that can be used by the financial sector? In contrast, when I teach in Luxembourg, where my students do not tend to have such natural science-heavy backgrounds, I try to make the course more about the scientific side. I try to teach them about the different types of ESG data and what skills could be useful to them to disseminate the inconsistencies in environmental data. I teach them more about scientific approaches and try to familiarise them with where and how they can find useful ESG resources. My teaching approach adapts according to who I am teaching; this ensures that my students know enough about both - the financial as well as the scientific side. However, it is important to note that because of how vast the area of sustainable finance is, it is impossible for an individual to have complete knowledge in both areas.”

Q: What is the role of governments in shaping a greener future and promoting a circular economy?

Kim: “I think governments play a huge role and are basically the gatekeepers of how we will get to a sustainable and circular economy. Every month or so we read something like “big investors urge governments to take action”, politicians say “business leaders need to do more” - this back and forth goes on while very little actually gets done. In my opinion, a lot of these initiatives, however, are hot air. The same investors who call for action, often are also lobbying to dilute any new concrete measures. This is where the regulators and governments need to come in and take decisive action. However, one thing that I have realised is that governments are basically just an aggregate of societal interests. They are representing the wishes of individuals, businesses, NGO’s etc. So even though people often say they want climate action, once governments introduce such policies, increasing fuel prices for example, people do not support the policy anymore. This was the case in France, with the Yellow Vests. There was a lot of political reaction. People want climate action but they do not want climate action to affect their own lives and lifestyles in any way.

Yet, that being said, government action is sometimes the only solution. Take for example, the initiatives by supermarkets to ban single use plastic bags in Australia. Customers were outraged as they really did not want to pay for plastic bags and hence, many supermarkets reversed course and had to re-introduce them. The government then went ahead and put a ban on plastic bags. Sometimes, there is no other way than regulation. Usually only a handful of companies want to take the “early adopter” reputational benefits, the overwhelming majority will wait and see, and only take action if there is no other way and regulators take action. Self-regulation has shown that we will not get anywhere, at least not in time to avert further ESG-related planetary degradation. Even in Japan, where people are much more aware and considerate of the environment, a considerable amount of plastic still ends up in waterways. Education helps, but only to a certain degree. Therefore, I see no other way around government action as the main way forward. The role of governments is immense in shaping a circular economy, and in promoting sustainable development in general.”

Q: What are your thoughts on the upcoming EU taxonomy and Sustainable Finance Disclosure Regulation (SFDR)?

Kim: “They are necessary and they are a very good start. Basically this goes back to the idea of greenwashing, where the impact is currently often being advertised but not properly recorded or verified. There's no way of making sure that what is promised is actually happening in reality. The EU recognises that greenwashing is a key problem. They want to ensure that not any activity can be labelled as green. So, investors cannot easily say that their product is a green investment when in fact it does not have any positive and measurable impact. For example, fossil fuels cannot be claimed as green investments under the EU Taxonomy. They have classified 6 objectives:

If you contribute to one of the 6 objectives then you become eligible to label your financial product as green. The taxonomy is sort of a catalog to screen for what is actually green and what is not. However, a very important point of the taxonomy as well as the SFDR is that there can be no tradeoff. You cannot do any significant harm to any of the other objectives. So - you need to contribute to one or more of the objectives yet be impact neutral towards the others.

As I said before, sometimes it is not possible to make a judgement about financial products because there is simply no sufficient data about it, both in terms of quality or quantity. The SFDR is trying to solve this. This is a very important step. Under this regulation, you cannot say an activity is green without having proper information and data about the said investments. The SFDR is trying to improve accountability, transparency and accessibility to data. All this information needs to be presented in a certain way and hence it also advances ESG data standardisation across the financial sector.

However, the problem is that a lot of actors or stakeholders in Europe feel that they are not ready yet. The regulation was supposed to enter into force in its entirety by March 2021, but numerous actors have heavily lobbied to postpone certain elements and now the EU is considering a delay ranging from 6 months to 1 year to fully implement all the aspects of these regulations. Investors claim that they do not have the capacity to produce the data required. This brings me back to the need to include more natural science professionals who can better understand, produce and report this sort of complex non-financial data. Investors can no longer just rely on rating agencies as there is a lot of divergence between ESG service providers and rating methodologies are often like a black box. The EU has said that rating data needs to be regulated. Indeed, we need better data and more transparency to fully embrace these new and important regulatory initiatives.”

Q: How does Asia compare to Europe in terms of ESG regulations?

Kim: “The key difference is that the European initiatives are mandatory. This is also what sets Europe apart from most of the world. A lot of other countries are in the process of creating their own taxonomies, yet they are not mandatory. They say that financial professionals should use them, but if they don't, there are no serious ramifications. It mostly just represents a ‘best-practice approach. Overall though, we do see a trend towards trying to create new or update existing financial and corporate governance frameworks. In Japan, they are creating a ‘transition taxonomy’ which is basically saying that while certain activities might not be fully green, they are still much better ESG performance-wise than the current status quo. So we should, for example, promote the transition to cleaner fossil fuel-based power generation using coal or natural gas, as an intermediate step towards a net-zero economy reliant on clean energy.

Globally, I think the investment community is now inching towards ESG and sustainable finance practices because they believe that what Europe is initiating will constitute the future global best practice standards. Basically every investor or asset owner will ask for ESG factor integration and it will be hard to justify not at least looking at sustainability in some way.”

Q: What excites you most about where ESG and sustainable finance is headed?

Kim: “What excites me most would be the prospect of more measures to reduce greenwashing. Europe is pushing very strongly in this direction and that gives me hope. Currently for me, there is strictly speaking no genuine green investing or green financial sector because of the absence of proper impact data. There are a lot of industry stakeholders claiming that their products are making a difference, but no one is systematically measuring, reporting or verifying ex-post ESG impacts. We can assume that it is better than the status quo but we cannot wait 10 years to see if global CO2 emissions went down, or deforestation of critical forest ecosystems halted. We need immediate action to fight greenwashing. If the EU is successful in sustaining this effort, it will serve as a powerful indication to the investor community that proper and transparent ESG products are here to stay. Additionally, if we can integrate more science-based accountability and subject matter expertise into the sector, it will improve overall institutional diversity, potentially yielding great results. We need finance professionals and science experts to be in the same room. I am hopeful that we are moving into the right direction with the strong regulatory actions in the EU as well as beyond. There will be a lot of pushback from many sides but if we can sustain this momentum, that would be ideal. Governments need to take quick, science-based and decisive action. This is what excites me the most.”