Interviews

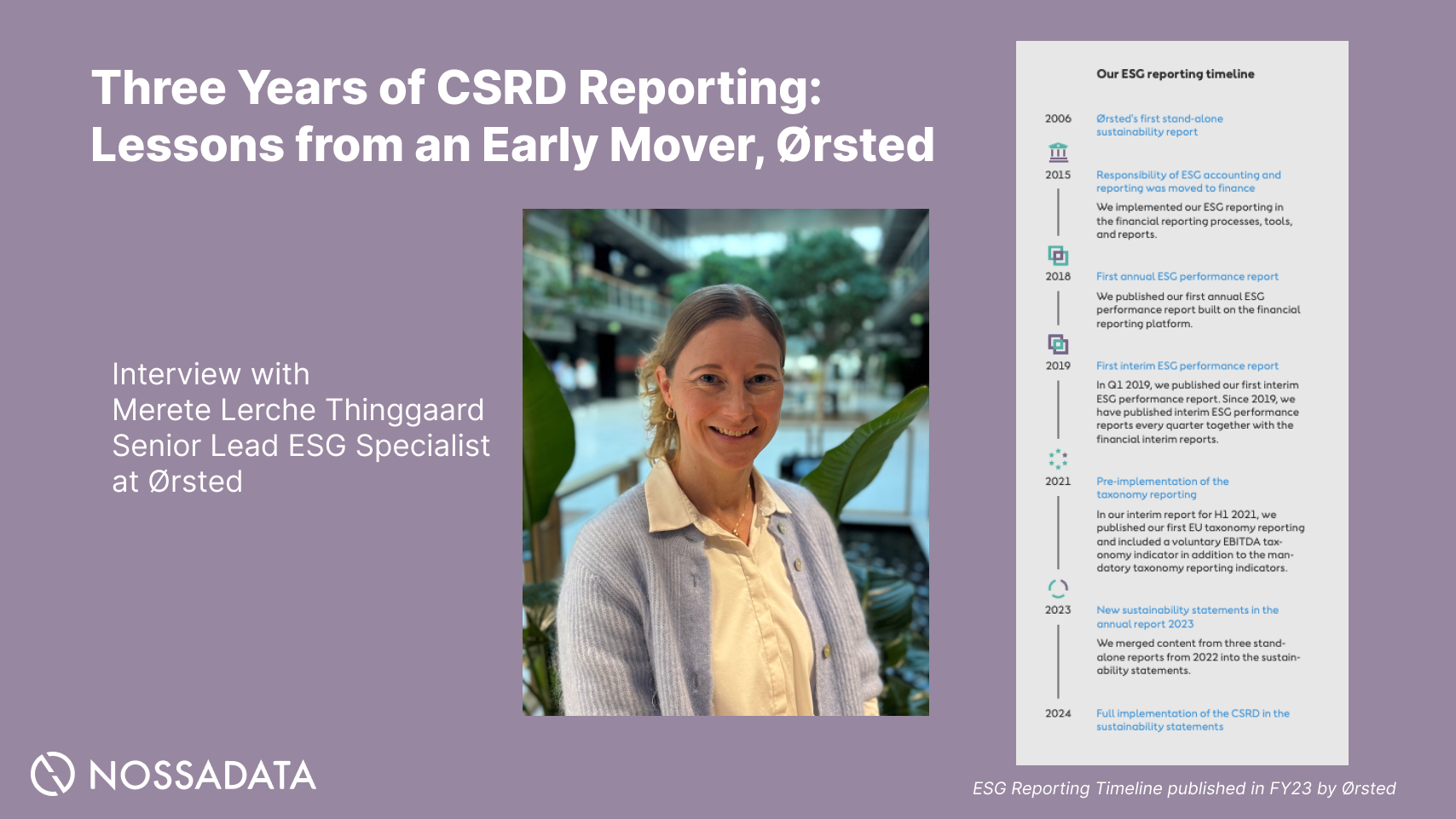

Three Years of CSRD Reporting: Lessons from an Early Mover, Ørsted

An expert interview with Merete Lerche Thinggaard, Senior Lead ESG Specialist at Ørsted, on three CSRD reporting cycles.

As the Corporate Sustainability Reporting Directive (CSRD) enters its second year of implementation for the first wave of in-scope companies, I wanted to focus an analysis specifically on communication about the DMA. The Double Materiality Assessment (DMA) is at the center of CSRD disclosure and I wanted to understand how Year 2 companies were considering this. This article compares the DMA methodologies of five Year 2 CSRD companies sharing about their processes overall and highlighting key parts of their disclosure.

The below x5 companies were assessed:

Ferrari

Country: Italy

Industry: Automotive – Luxury Sports Cars

Market Cap: ~$66.4 B USD (Feb 2026)

Description: Ferrari N.V. designs, engineers, and sells high-performance luxury sports cars and supercars, with a storied heritage in motorsports and Formula 1 racing. It also monetizes its iconic brand through licensing and luxury lifestyle experiences, blending automotive excellence with premium branding.

Ferrari’s Annual Report FY2025.

KPN

Country: Netherlands

Industry: Telecommunications / Telecom Services

Market Cap: ~$20.8 B USD (Feb 2026)

Description: Koninklijke KPN N.V. is a leading Dutch telecom operator providing fixed and mobile telephony, broadband internet, and television services, along with IT and cloud solutions for business customers. The company’s network infrastructure supports consumer, enterprise, and wholesale communications across the Netherlands.

KPN Integrated Annual Report FY2025.

Norsk Hydro

Country: Norway

Industry: Metals / Aluminium Production

Market Cap: ~$18.0 B USD (Feb 2026)

Description: Norsk Hydro ASA is a global aluminium producer headquartered in Oslo, operating across the value chain from raw materials to finished products, with significant renewable energy activities. It serves industries such as automotive, construction, and packaging, and is focused on low-carbon aluminium solutions.

Norsk Hydro Integrated Annual Report FY2025.

E.ON

Country: Germany

Industry: Energy / Utilities – Electric & Gas

Market Cap: ~$57.0 B USD (Feb 2026)

Description: E.ON SE is a major European utility company that generates and distributes electricity and gas, serving millions of customers across Europe. It focuses on energy networks and customer solutions, including renewable and efficient energy services.

Nordea

Country: Finland

Industry: Financial Services / Banking

Market Cap: ~$66.4 B USD (Feb 2026)

Description: Nordea Bank Abp is the largest financial services group in the Nordic region, offering retail, corporate, and institutional banking, asset management, and wealth services. Headquartered in Helsinki, it serves millions of customers across northern Europe and operates through a pan-Nordic business model.

Currently you can review the Simplified EFRAG guidance on DMAs (from late 2025). This is available here. “3. Double materiality as the basis for sustainability reporting”

Under the requirement 3.1.3 Bases for assessing materiality the below is stated:

In EFRAG’s guidance it also explains that double materiality has two dimensions: impact materiality and financial materiality and the undertaking shall consider how they interact. An impact can be financially material from the start or become financially material, when it is reasonably expected to affect the undertaking’s financial performance, financial position, cash flows, its access to finance or the cost of capital over the short, medium or long term. Impacts can be material exclusively from an impact perspective, irrespective of whether they are financially material.

Read the EFRAG guidance for a full overview.

Ferrari:

KPN Process description:

Norsk Hydro Process Description:

The materiality assessment is based on input from Hydro’s subject matter experts in group functions for climate, environment, social responsibility, health and safety, communication and investor relations, compensation and benefits, diversity, inclusion and belonging, compliance, and enterprise risk management, as well as input from risk management and sustainability functions in each business area. Involvement of the risk management functions supports the identification and further evaluation of sustainability related impacts and risks.

The views of Hydro’s stakeholders are integrated in the annual update of the materiality assessment. Hydro’s group functions and business areas summarize input provided to them through their engagement with affected stakeholders and their interaction with external sustainability experts and users of Hydro’s sustainability statement.

EON:

Nordea:

1) understanding the context of the organisation

2) identifying actual and potential impacts, risks and opportunities

3) assessing actual and potential qualitative and quantitative impacts, risks and opportunities

4) determining material impacts, risks and opportunities by applying appropriate thresholds.

Impact materiality is determined based on positive and negative impacts, while financial materiality is determined based on financial risks and opportunities. An ESG matter can be material from an impact materiality perspective, a financial materiality perspective, or both. The outcomes of the impact assessment and the risk and opportunity assessment are consolidated, forming our DMA outcome and determining the sustainability matters that are material for us. As part of the consolidation process, any interdependencies between material impacts, risks and opportunities are formalised.

In 2025 our DMA outcome was validated in consultation with internal representatives of our six main stakeholder groups and through a newly established stakeholder engagement framework. This involved drawing on regular dialogues with affected stakeholders and incorporating their considerations where applicable.

Ferrari:

This year Ferrari included a benchmarking assessment in their double materiality assessment stage:

EON: EON also included a benchmarking and refining piece in their DMA explaining.

“In 2025 we focused in particular on clarifying and condensing our description of material IROs in order to avoid duplication. Feedback from internal stakeholders (such as the CEO, CFO, and Supervisory Board) and external stakeholders (by means of, for example, benchmarking analyses and peer comparisons) was also taken into account.”

KPN: Both impact and financial materiality did not materially change compared with the previous year; the list of material sustainability matters remained unchanged.

Nordea: The 2025 DMA results are largely unchanged from 2024. The few changes reflect the increased robustness of the analyses, which enabled us to further mature the disclosures.

Ferrari: The Double materiality assessment was prepared under the supervision of Ferrari Group’s Chief Financial Officer and the results were approved by the FLT and by the Audit Committee of the Board of Directors.

KPN: The outcomes of both assessments were validated by the ESG Board and approved by the Board of Management, and shared with the Audit Committee and Supervisory Board.

Hydro: The assessment is reviewed by Hydro’s disclosure committee and approved by the Board of Directors.

EON: Our CEO and CFO then reviewed and approved the selection of the threshold, the topic clusters identified as material, and the resulting reporting obligations. In addition, we consulted the Supervisory Board’s Audit and Risk Committee prior to the Management Board’s final approval. There was also an information sharing about the materiality assessment with the Group Works Council and the European Works Council. E.ON’s CEO and CFO gave final approval to the assessment’s findings. In addition, the Supervisory Board’s Audit and Risk Committee and the Group Works Council were informed

Nordea: The methodology and process description are anchored internally, and the outcome is subject to Group Leadership Team and Board of Director approval.

KPN communicates their approach to thresholds: For the impact materiality assessment, impacts are material for reporting purposes if they exceed certain thresholds. We defined an initial threshold of >~7.0 for absolute impact (positive, negative) or relevancy >4.0. However, we subsequently applied qualitative criteria to determine which (sub or sub-sub) topics have a material impact and which not. For the financial materiality assessment, scenarios that could hinder the realization of KPN’s outlook – the 3-3-7 ambition: ~3% increase for service revenues, ~3% for EBITDA after leases (EBITDA AL) and ~7% for free cash flow (FCF) until 2027 – the related risks and opportunities are regarded as material for sustainability reporting purposes.

E.ON also explained their materiality thresholds: E.ON defined a materiality threshold for the purpose of differentiating material IROs from those that are non-material. IROs that exceeded this threshold for one of the two perspectives (impact or financial perspective) were deemed material within the meaning of the ESRS. In consultation with the specialist departments involved, the threshold 3.0 on the assessment scale used was selected for IROs. This threshold was considered appropriate because it is exactly in the middle of the 1-to-5 scale and thus enables an objective differentiation between material and non-material aspects. We conducted workshops with the above-defined stakeholder groups’ in-house proxies for the purpose of validating the Group-wide assessment’s findings centrally and ensuring that the list of material IROs is correct and complete. Each stakeholder group could use a correction factor to adjust the findings. IROs ultimately deemed material during the validation process were assigned to topic clusters and to the relevant ESRS disclosure requirements.

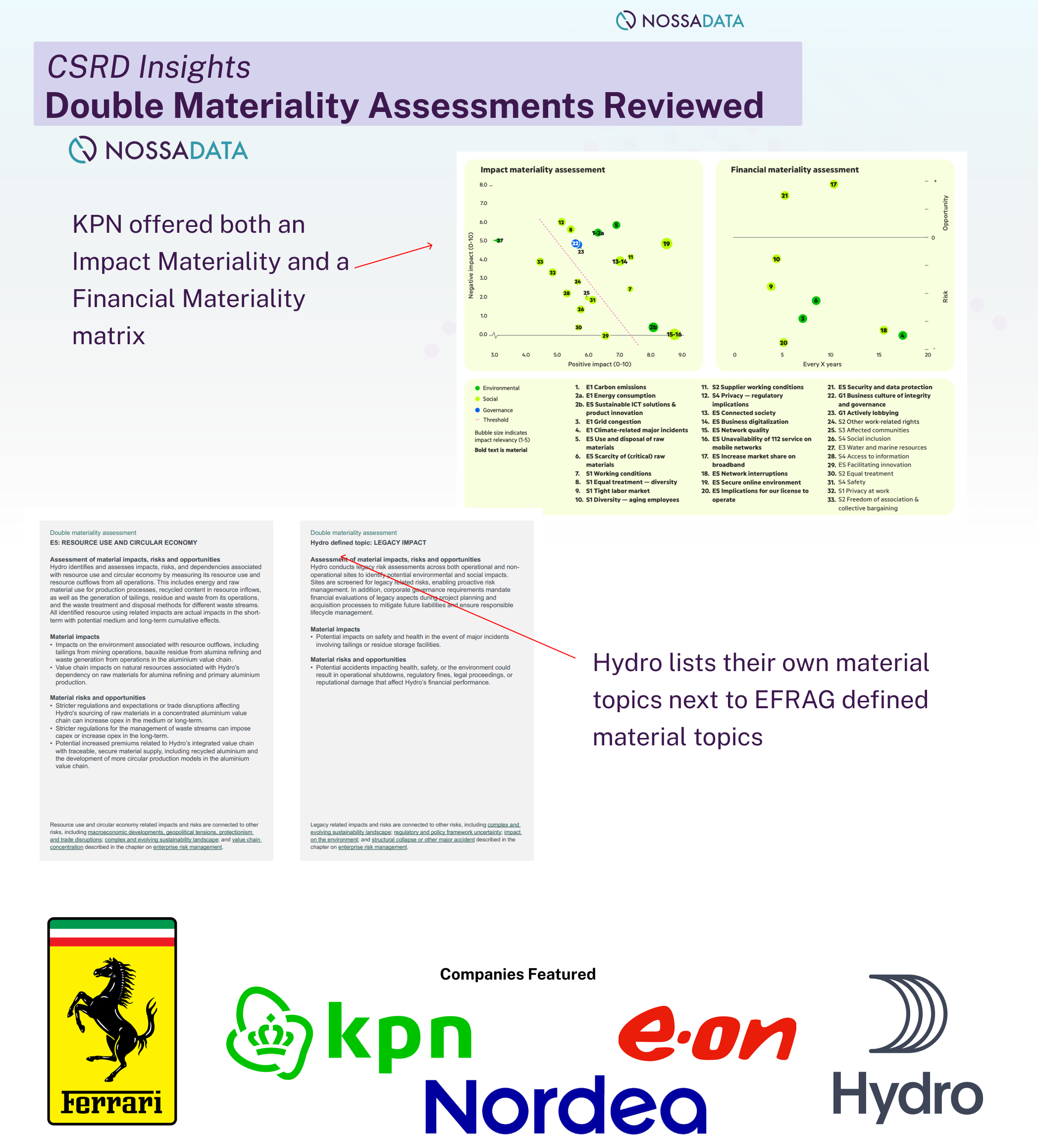

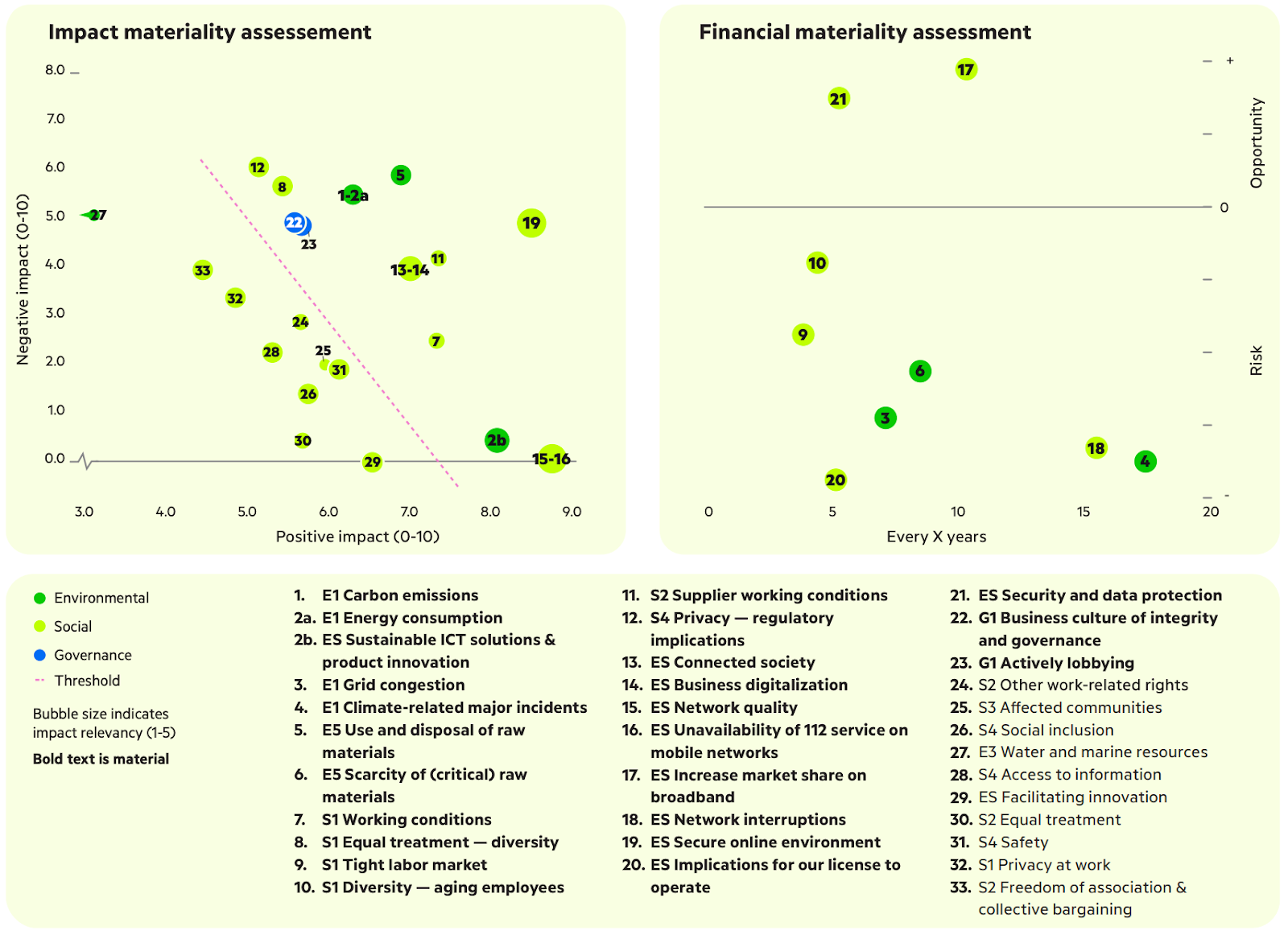

KPN produced side by side tables comparing the results of their impact materiality assessment and their financial materiality assessment.

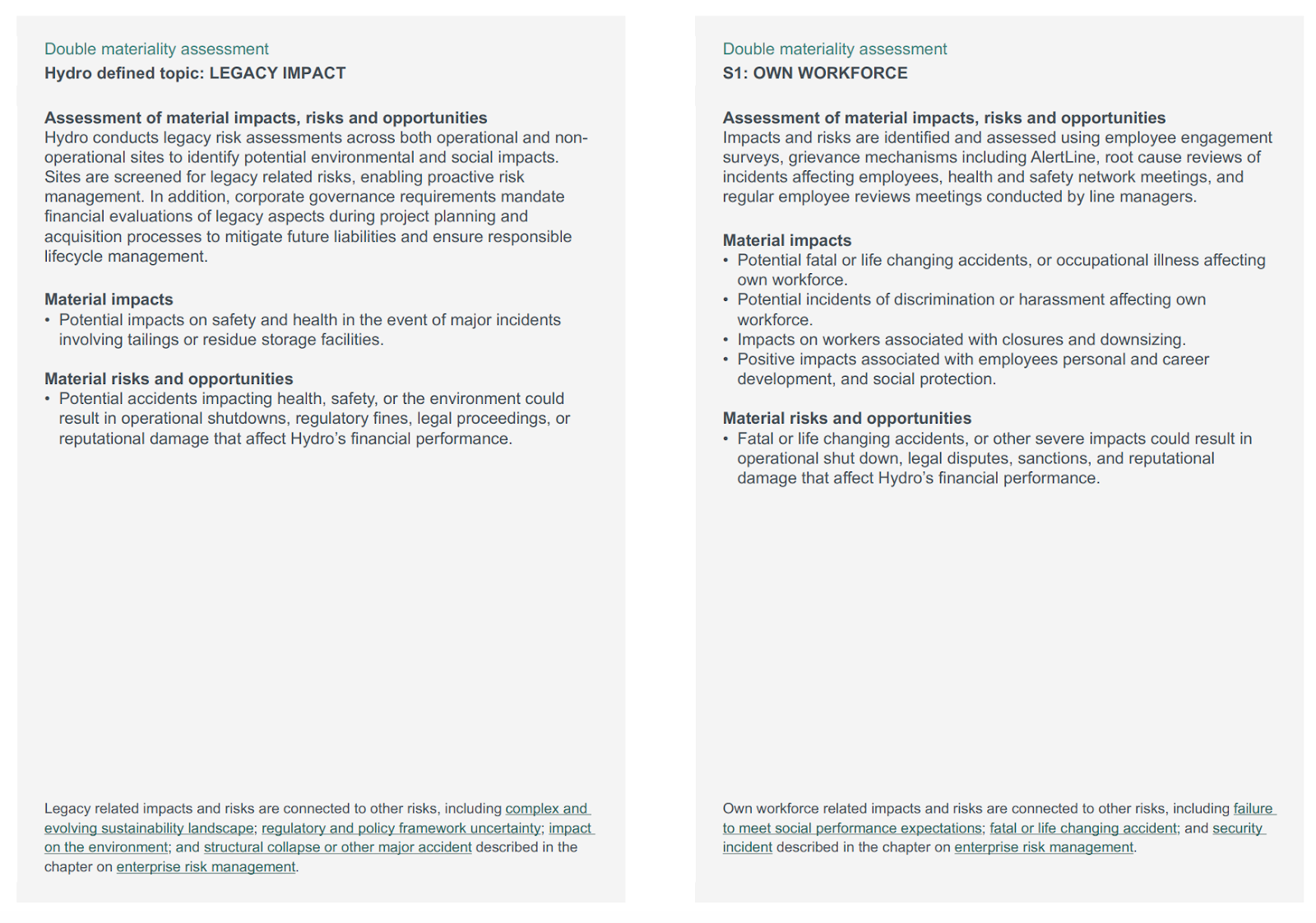

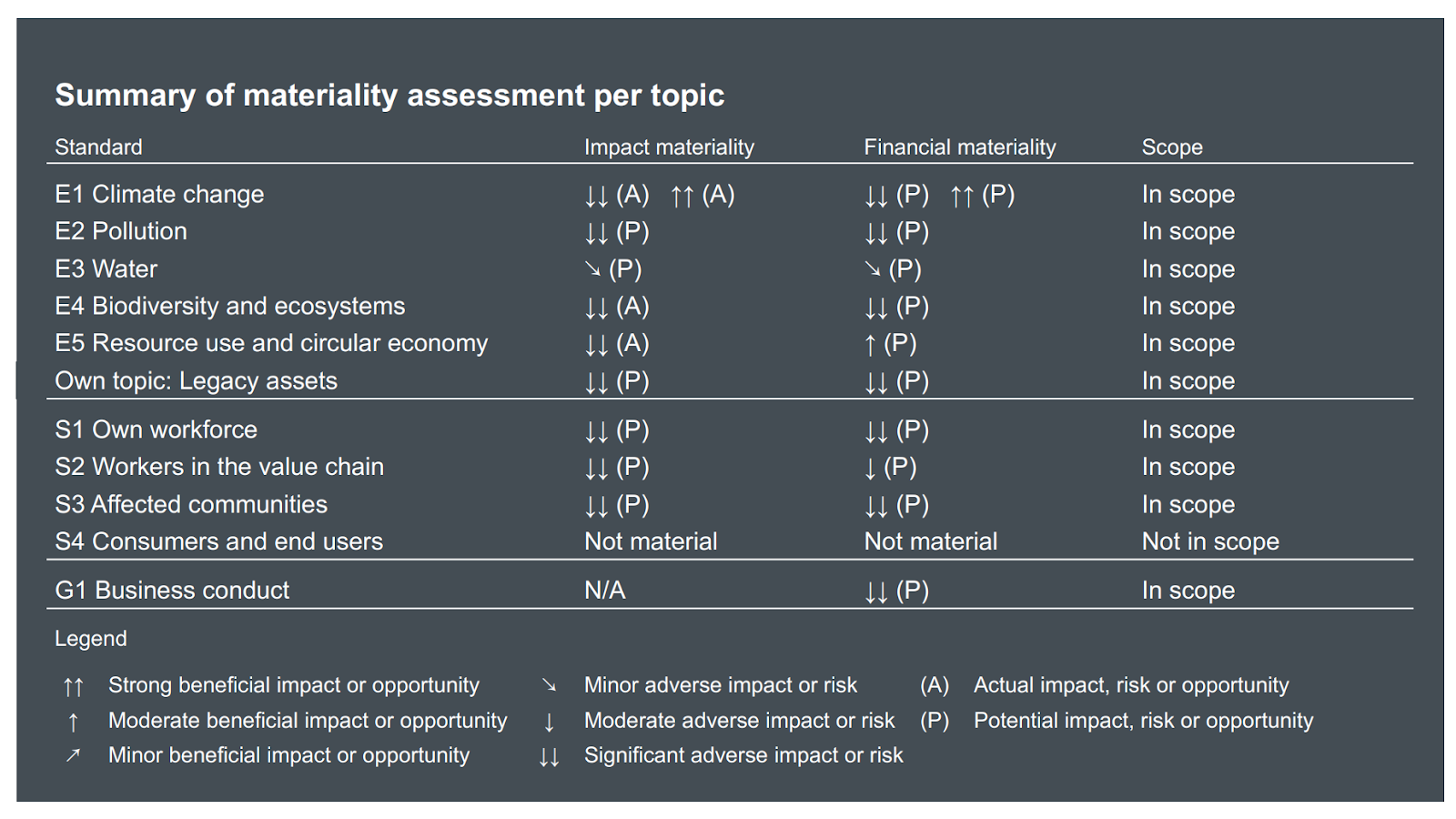

Hydro: Each material risk is presented in a table format describing what the IRO results are, its material impacts and its material risks and opportunities.

Hydro offers a summary table of each of the ESRS topic standards and how they related to Hydro.

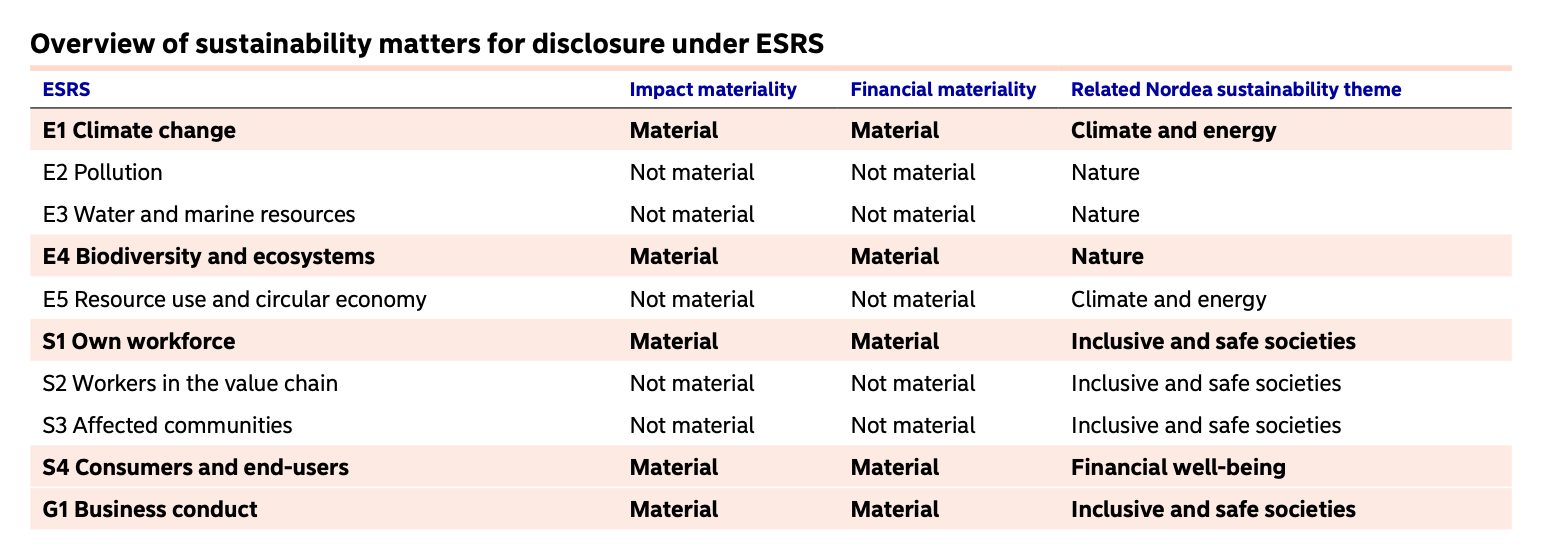

Nordea also offers a summary table versus all ESRS topic standards.

Want to work with Nossa Data on your CSRD Disclosure? We are an ESG Reporting Platform and an advisory tool aimed at streamlining corporate disclosure. Get in touch at solutions@nossadata.com