Interviews

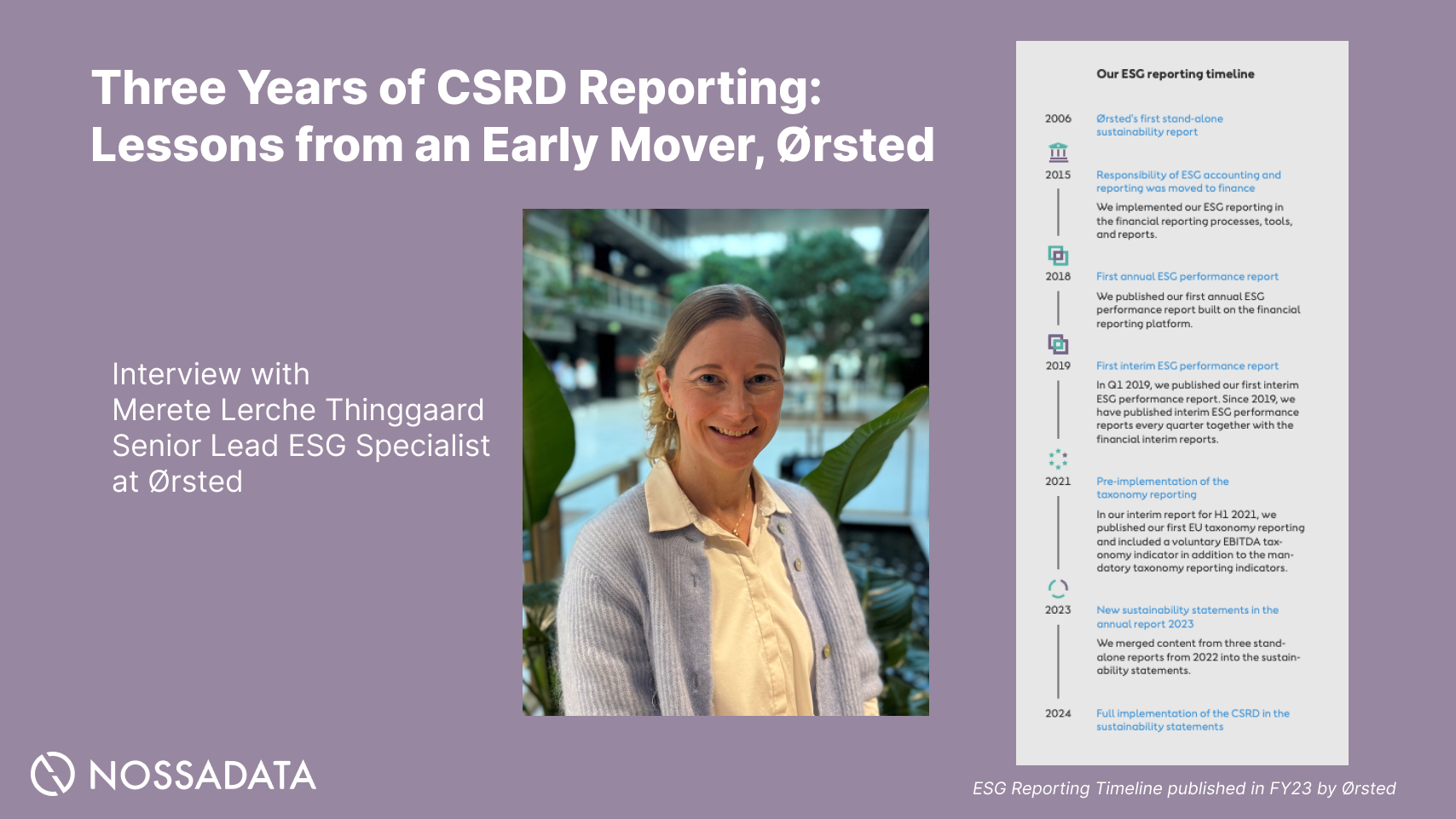

Three Years of CSRD Reporting: Lessons from an Early Mover, Ørsted

An expert interview with Merete Lerche Thinggaard, Senior Lead ESG Specialist at Ørsted, on three CSRD reporting cycles.

We interviewed Tamara, Founder and Managing Director of Close Group Consulting.

I spent over 20 years in the investment and risk management industry. I started out on the sell-side in institutional sales and trading, and then moved to the buy-side at a fixed income asset manager. After that, I went to one of the largest pension funds in Canada, PSP investments, to work in their Public Markets team. It has been about eight years since I was first introduced to ESG. At that time, PSP had a team of one and was very much focused on stewardship and proxy voting. PSP wanted to become a signatory to the UNPRI and it was my responsibility to see if this would make sense from a public markets perspective. This was really when I became introduced to ESG factors, but very quickly I realised how these factors were very material and very relative to the investment management process and the risk management process. It also became clear that there was a huge gap between the investment industry and the sustainable investment/sustainable development industry. I decided to leave PSP 5 years ago to work primarily in ESG and I started my own advisory firm.

“I've been working with asset managers and asset owners to help them integrate ESG into their investment and risk management processes.”

.jpg)

The tool assesses ESG integration for investment firms and investment funds. It's a very detailed assessment of the ESG integration practices for asset managers and general partners and it assesses them against industry best practices. The tool distinguishes between firm practices and fund practices. For example, a firm may have a very sophisticated ESG integration methodology, but that doesn't necessarily make its way down to each of the firm’s individual funds. On the flipside, a very sophisticated fund in terms of its ESG integration, may not run up to the level of the parent firm. This assessment tool allows for both - an assessment at the firm and at the fund level.

Another feature is that it's asset class specific. You have different lenses when you integrate ESG into private markets versus public markets. If you look at something like private debt, you arguably have even fewer levers to pull when it comes to ESG integration. Concentrating your efforts at the screening and pre-investment stage is very important for a private debt manager, whereas public equities or private equities have a different type of perspective when they consider ESG integration.

In terms of the reasoning behind the tool and the market gap, there was (and still is) confusion in the market regarding ESG integration.

“Pretty much all managers these days integrate ESG, but it's still very difficult to identify which ones are doing it at a very sophisticated level and which ones are doing it at a more initiated level.”

ESG integration is not binary. It's not a matter of if “you do it or you don't do it,” there are so many different ways of doing it.

A sophisticated investor will be integrating ESG top-to-bottom within their business model and end-to-end across their investment and risk management processes. If you do an assessment within the tool, the scoring is very granular and built out across different categories and subcategories, so you can see where you're integrating ESG and to the level it's being integrated. A more sophisticated manager can show their clients just how advanced they are when it comes to ESG integration. A less sophisticated or more initiated investor can see what they need to be doing to integrate ESG at a higher level of maturity.

We didn't want the tool to just be a survey where you get asked a lot of questions, you answer them, we go away, and we come back and score you. We wanted to be completely transparent to the user and have a very granular scoring methodology. Every category and subcategory has a score, and these roll up into an aggregated category score and then an aggregated overall score. But there are many different ways you get to that overall score, and you can see that in the breakdown of the scoring.

I think the one that we see most often is that ESG integration is a ‘one and done’ type thing. There's an idea out there that you'll just go and create a policy, maybe bring in some external ESG data, map that to your positions, become a signatory to PRI, and then you're done. But if you really want to integrate ESG, whether you're an asset manager, an asset owner, or a corporate, it's about a strategic shift within the organisation. It’s about creating a different mindset across the entire firm.

So again, top-to-bottom and end-to-end. This includes ESG within investment and risk management processes, but also the firm itself. It includes looking at diversity and inclusion and even procurement processes and how you're integrating ESG or sustainability across those processes.

“As the industry and the market evolves, so will the level of ESG integration. It's really important for investors to understand that this is not a check the box process. Rather, it’s something that will gradually evolve within your firm, so setting up the right infrastructure for that now is really important.”

Generally speaking, I’ve tended to work with firms that have already made that decision to integrate ESG and become a more sustainable firm. How they've come to that decision certainly varies, some will be coming from pressure from their investors, clients or private equity owners.

It’s important for firms to understand it depends on which ESG factors are mission critical for their business model; it really is a business model and business strategy decision for a firm. Therefore, it should sit under the purview of executive management and the board. It should not be relegated or completely delegated to a sustainability officer or the head of responsible investing. It needs to sit at the top of the house.

“I’d say that if a company is more reticent to integrating ESG, then it’s probably because that decision has not yet made it up to the top of the house with the executives and board level decisions.”

Yes, this is an excellent question! I would say that they should approach this like they would for any other strategic shift or initiative. You need to have a strong and solid project management process to back this up. For instance, when we propose certain ESG initiatives to an investor, we build out a target state for them and then create a very detailed and customised implementation plan and roadmap with different ESG initiatives. We also provide an assessment of the various levels of effort required. This way firms can focus on those initiatives that make the most sense for them now and implement the others a bit later.

As I have a background in risk, I'm really happy to see that the risk teams are getting more involved with this now. They have not been as involved with ESG because risk teams are very quantitative teams. They do a lot of quantitative modelling and financial modelling, and come up with risk thresholds, budgets and constraints for Portfolio Managers.

“But one of the issues with ESG is that while it can be quantitative in nature, it is generally qualitative and can be subjective. This makes it difficult for a risk team to model some of these risks and to put a threshold or constraint on an investment or a portfolio.”

But it’s great to see such teams getting more involved. Scenario analysis, for instance, has really progressed so that’s helpful. Definitely everything around climate and carbon has progressed. You can actually put a price on carbon, so we've seen a lot more modelling in terms of carbon risk of investments in portfolios which is great as the world is committing to a net-zero or low carbon economy.

I think that when the risk teams start deep diving into this data, and having reporting solutions for this data from the corporate side, it’s really helpful because it creates a consistent and comparable database for the team to model some of the risk exposures. Once the risk teams can start modelling exposures, it impacts how the managers are managing them. Therefore, it’s helpful for the market going forward.

One of the most interesting things I have found in some research I recently co-authored, is that ESG is a business model and business strategy issue.

“ESG absolutely needs to sit at the board level on the corporate side. Even on the investor side, it needs to sit at the executive and board level.”

ESG is just a better way of calculating risk. And whether it's mitigating risk to a corporation/investment, or leveraging those opportunities, it's understanding the underlying business model of the company which can determine the actual ESG risk/opportunity for an investment. The reporting side is fantastic because it's opening the door to this, but now we want to see how companies are managing these issues and not just reporting on them. As ESG risks are becoming increasingly systemic in nature, it is even more important for investors to find firms that are managing these risks. That's certainly something that people are looking at, and as the companies start realising this, it will increase the quality of their reporting. It's definitely going to move the market forward.

Right now, there’s a huge emphasis on climate. That's at the top of mind for a lot of investors. The regulatory environment too, it's always been strong in Europe, but it's certainly becoming much stronger in North America. I’d say that's pushing a lot of investors to take action now, and we have seen a huge increase in the number of managers looking at integrating climate risk management into their portfolios and investments.